Is Monday.com Ltd a Buy After Its Latest Earnings Report?

Key Points

The company's first-quarter results blew past expectations.

AI revenue is accelerating, thanks to enterprise customers who are sticky, growing, and using multiple products.

The business is excellent, but the valuation suggests the easy gains are likely behind us.

- 10 stocks we like better than Monday.com ›

There's a certain type of stock investors love to discover early: fast-growing, profitable, founder-led, and riding a massive technological shift. Monday.com checks every one of those boxes.

The company just delivered another impressive quarterly earnings report yesterday, posting 24% revenue growth in the first quarter of 2026, record operating profit, expanding enterprise adoption, and an increasingly compelling artificial intelligence (AI) strategy. On the surface, it looks exactly like the kind of stock that could become a long-term compounder.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

But here's the more important question for investors today: Can a great business still be a great stock to buy right now?

That distinction matters -- especially in high-growth software investing, where even excellent businesses can underperform if expectations get too high. And after Monday.com's latest set of results yesterday, that debate has become much more interesting.

Image source: The Motley Fool.

The quarter was undeniably strong

Monday.com's latest quarterly results easily cleared Wall Street expectations.

Revenue reached $351 million, up 24% year over year and ahead of consensus estimates. Adjusted earnings per share came in at $1.15, crushing analyst forecasts of $0.93 by a massive 23%.

Profitability also remained impressive:

- Gross profit climbed 23% from last year's first quarter to $313 million.

- Operating income (on a GAAP basis) hit a record $20 million.

- Adjusted free cash flow margin expanded to 29%.

What makes these numbers stand out is that Monday.com isn't growing at the expense of profitability. Many software companies chasing AI growth are burning cash to do it.

Monday.com is doing the opposite. The cloud-based SaaS (Software as a Service) business continues to invest aggressively in artificial intelligence while still generating meaningful operating leverage and free cash flow.

AI is no longer just a feature

My biggest takeaway from the earnings call wasn't the revenue beat. It was management's clear message that the company is evolving from a workplace collaboration tool into a full-scale AI work platform.

Management repeatedly emphasized that the company wants AI agents, including third-party agents, to perform work inside organizations, and not simply help employees organize it.

Importantly, the monetization has already begun. Management disclosed during the earnings call that approximately 10% of net new annual recurring revenue in the quarter came directly from AI-related products. Even more notably, that figure excludes the company's newly launched AI agents, which were only introduced recently.

The company also introduced a new pricing structure combining traditional software seats with AI consumption credits. That move could eventually unlock a much larger revenue opportunity because AI usage scales differently than employee headcount.

Enterprise adoption keeps accelerating

Another major reason investors are excited about monday.com is its continued success moving upmarket.

The company said 42% of annual recurring revenue (ARR) now comes from customers spending more than $50,000 annually. It also reported a record number of customers generating over $500,000 in annual recurring revenue.

This metric matters because enterprise customers tend to be stickier, expand spending over time, and possibly adopt multiple products. As a result, they help generate more predictable cash flow.

Monday.com's cross-selling strategy also appears to be working. More than one-third of large customers now use multiple products across the company's ecosystem, including CRM and service-management offerings.

Its customer relationship management (CRM) business alone has already surpassed a $100 million revenue run rate.

That diversification is important because it reduces reliance on a single product category while increasing the platform's long-term strategic value.

But here's the catch investors shouldn't ignore

This is where the story gets more nuanced.

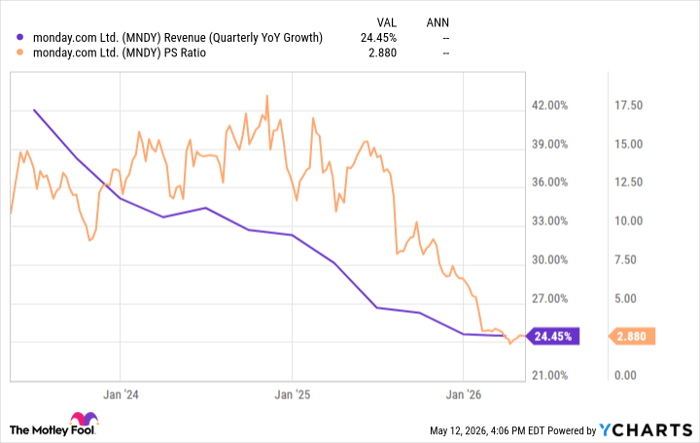

Despite all the positives, management still acknowledged that top-of-funnel demand remains "soft." Management expects net dollar retention to decline slightly throughout the year, as last year’s price increases already helped boost results. And that's evident from the slowing revenue growth seen below.

MNDY Revenue (Quarterly YoY Growth) data by YCharts.

AI competition is intensifying -- nearly every major software company is now racing to build agents and automate workflows. In other words, execution alone won't guarantee outperformance when expectations are already high.

That's often where great companies stop being the best investments.

Monday.com's quality is well understood by the market. The harder question is whether meaningful upside remains. Its price-to-sales ratio has collapsed from nearly 19 to just 2.9 in under 18 months, suggesting fading investor enthusiasm.

The stock surged 18% after yesterday's earnings release -- only to give it all back. Two trading sessions later, the stock sits 16% lower, a sign that Wall Street's initial excitement faded fast once the dust settled. Oftentimes, a great company isn't enough. You need room for upside surprises too.

Savvy investors look at Monday.com's trajectory as a blueprint. They understand that the best investment opportunities aren't the most obvious winners that everyone is already talking about. Rather, they look for businesses quietly entering similar growth curves before Wall Street fully catches on.

Should you buy stock in Monday.com right now?

Before you buy stock in Monday.com, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Monday.com wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $460,826!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,345,285!*

Now, it’s worth noting Stock Advisor’s total average return is 983% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 12, 2026.

Isac Simon has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Monday.com. The Motley Fool has a disclosure policy.

Recommended Articles