The Nasdaq Is in Correction Territory. Here Are the 2 Artificial Intelligence (AI) Stocks I'm Buying First.

Key Points

Clarity often arrives after market-beating opportunities become obvious.

Artificial intelligence (AI) infrastructure spending hasn't blinked as the hyperscalers continue to move at full speed.

The Nasdaq correction is a rare entry point for investors to pounce on high-quality compounders at a discount.

- 10 stocks we like better than Micron Technology ›

In late March, the Nasdaq Composite (NASDAQINDEX: ^IXIC) officially crossed into correction territory as the index fell roughly 10% from its prior highs. The Nasdaq's nosedive is thanks to a litany of macro uncertainties driven by renewed tariff anxiety, geopolitical tensions in the Middle East, stubborn inflation, and most importantly, ongoing rotations away from richly valued technology stocks.

While this turbulence is disorienting, long-term investors understand that corrections are not ultimatums -- often, they are invitations. The question is not whether to buy stocks now, but rather which companies to double down on.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

In my eyes, the most durable opportunities still reside in the artificial intelligence (AI) infrastructure buildout. Despite a cloudy macroeconomic environment, the AI revolution has not paused or pivoted. And big tech's $720 billion capex surge underscores that AI demand is showing no signs of doing either.

Right now, two names stand out among a crowded pack of market laggards: Micron Technology (NASDAQ: MU) and Broadcom (NASDAQ: AVGO).

Image source: The Motley Fool.

1. Micron is the memory engine AI models can't live without

Every large language model (LLM) that runs an inference upgrade needs memory. High-bandwidth memory, or HBM, is the specific architecture that Nvidia's Blackwell and Vera Rubin GPUs depend on to transfer data between underlying processing clusters and the memory stack.

When model sizes grow, inference workloads compound -- forming a bottleneck around the HBM content per server rack. Every incremental dollar spent on AI infrastructure by Microsoft, Alphabet, Amazon, Meta Platforms, and Oracle requires a proportional increase in memory bandwidth. Micron's HBM3E and upcoming HBM4 development helps keep the company's solutions competitive at each successive node.

The HBM market is highly fragmented, with Micron being only one of three companies capable of producing this technology at scale -- alongside Samsung and SK Hynix. With HBM inventories already sold out for the year and investments in manufacturing capacity rising, Micron stands out as the company with the most aggressive ramp heading into the inference era.

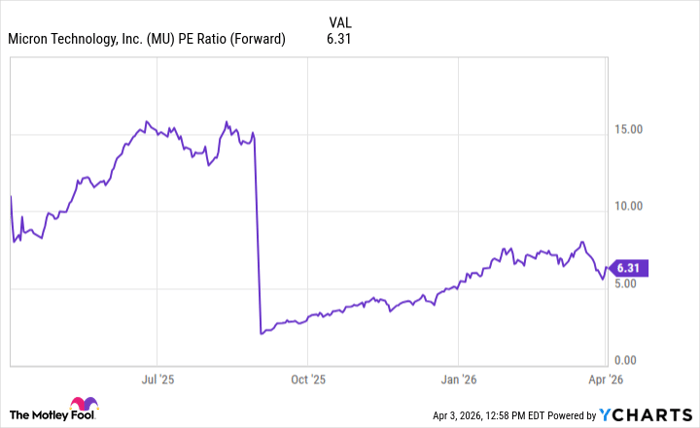

On valuation, Micron trades at roughly 6 times forward earnings -- a figure that looks absurdly cheap when benchmarked against other AI chip stocks that boasted forward P/E multiples between 30 to 50 times prior to the Nasdaq sell-off.

MU PE Ratio (Forward) data by YCharts

Part of the discount reflects lingering skepticism around the durability of the memory supercycle. In addition, the release of TurboQuant -- a new compression algorithm from Google -- has only added fuel to the fire.

These concerns create an opportunity. Rather than relying on a single product cycle, structural demand from the hyperscalers for DRAM and NAND chips creates a floor supporting Micron's trajectory. This is what makes the company's growth sustainable.

Micron remains a core pillar supporting a multi-year, multi-trillion dollar infrastructure buildout. Meanwhile, the company is growing revenue at triple-digit rates and earnings per share are expected to quadruple this year. In my eyes, Micron's plummeting stock price is not a value trap -- it is a rare mispricing.

2. Cashing in on custom silicon

When it comes to AI anatomy, Micron is the memory backbone while Broadcom is the central nervous system. The company designs custom application-specific integrated circuits (ASICs) -- known as XPUs -- for the likes of Alphabet (whose tensor processing units were made in tandem with Broadcom), Meta, and OpenAI.

Rather than competing with Nvidia and Advanced Micro Devices in the general-purpose GPU market, Broadcom discovered a different and arguably more defensible pocket in the chip realm. The company designs bespoke accelerators tailored for specific workloads and then connects these chips with networking equipment. No company specializes in both product sets at scale.

The durability of Broadcom's position in the AI landscape is supported by the depth of its customer relationships and the complexity of what the company builds. Custom silicon engagements are long-term commitments. Once a hyperscaler has co-designed an XPU rooted in Broadcom's DNA, transitioning to a competitor comes with the cost of restarting a multi-year design cycle.

These switching costs create a moat that compounds over time as infrastructure spending accelerates -- allowing Broadcom to generate significant AI-driven growth alongside hyperscaler buildouts.

Another catalyst for Broadcom stems from the recurring cash flow the company commands through its VMware software, which provides stability and cushion to earnings should the core AI business face unforeseen variability in data center spending.

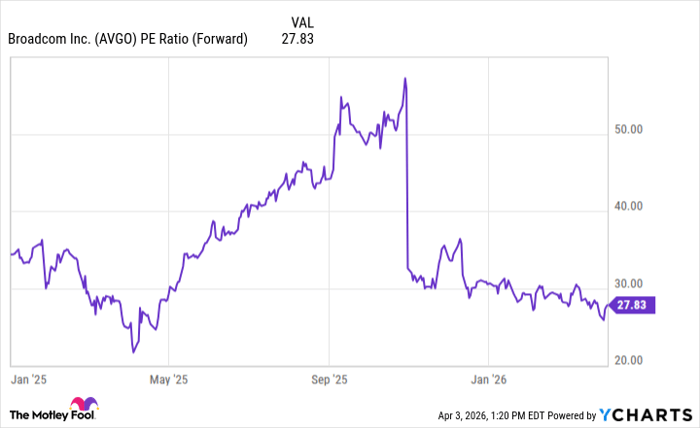

At roughly 28 times forward earnings, Broadcom is trading about 50% off its prior highs witnessed late last year. While this valuation still isn't dirt cheap in an absolute sense, I think it's reasonable for a company with Broadcom's diversification, specialized role in the AI ecosystem, and ability to ride secular tailwinds driven by accelerating investment in infrastructure.

AVGO PE Ratio (Forward) data by YCharts

Looked at differently, if you compare Broadcom to pure-play software names offering commoditized products and burning cash against an uncertain monetization timelines, Broadcom's current setup looks much more appealing for investors with a long-run time horizon.

Should you buy stock in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $532,929!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,091,848!*

Now, it’s worth noting Stock Advisor’s total average return is 928% — a market-crushing outperformance compared to 186% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of April 9, 2026.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Micron Technology, Microsoft, Nvidia, and Oracle. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Recommended Articles