The Week on Wall Street: Fed Holds Steady, Warsh Nomination Roils Markets Amid Shifting Sentiment

Previous Week’s Market Review & Analysis

Macroeconomic Landscape: The U.S. economy demonstrated continued strength, with third-quarter 2025 growth at an annualized 4.4%, primarily driven by consumer spending which rose 3.5%. The Federal Reserve, at its January 28, 2026, meeting, maintained the federal funds rate target range at 3.50-3.75%, following three consecutive rate cuts in late 2025. This decision reflected solid economic activity and an improving balance of risks to the Fed's dual mandate, even as inflation appeared to have peaked at 3% and shown declines in recent months. December's core CPI registered 2.6% year-over-year. The labor market presented signs of stabilization, with job gains remaining low but unemployment rates showing stability. The U.S. dollar weakened against other major currencies, particularly the Japanese yen. Gold prices briefly surged above $5,100 per ounce for the first time on Monday, January 26, though a reversal was seen on Friday.

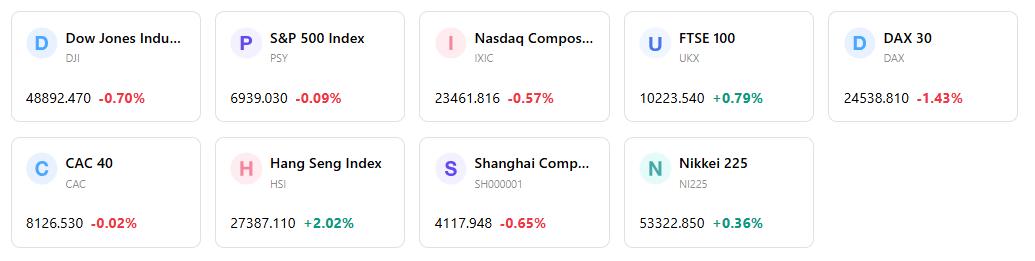

Market Performance Overview: U.S. equities experienced a mixed but generally positive week, concluding with increased volatility. The S&P 500 rose 0.5% on Monday, January 26, reaching a new record high on Tuesday, January 27, and nearing the 7,000 milestone. The Dow Jones Industrial Average added 0.6% and the Nasdaq Composite gained 0.4% on Monday, with the Nasdaq reaching a near three-month high on Tuesday. However, by Friday, January 31, U.S. indices pulled back, with the Dow Jones declining 0.85%, the S&P 500 down 0.52%, and the Nasdaq Composite falling 0.66%. This downturn was marked by sector rotation, as materials, communication services, and technology stocks became drags on the S&P 500, particularly influenced by perceived hawkish Fed sentiment impacting growth-sensitive tech.

Key Events Analysis: A significant event was the Federal Open Market Committee's (FOMC) decision on January 28 to hold interest rates steady. Corporate earnings season continued, with Baker Hughes, Boeing, and General Motors reporting stronger-than-expected fourth-quarter profits. Conversely, the healthcare sector saw sharp declines on January 27, as a Trump administration proposal for modest increases in Medicare insurer payment rates led to significant drops in stocks like UnitedHealth, Humana, and CVS. News on January 30 regarding the nomination of Kevin Warsh as the next Federal Reserve chair introduced uncertainty and contributed to market corrections. January's consumer confidence unexpectedly deteriorated to its lowest level since 2014, although this had limited immediate market impact.

Flows & Sentiment: Equity fund flows showed a mixed picture. For the week ending January 21, estimated inflows into equity funds were $1.58 billion, a notable decrease from the previous week's $31.31 billion. Domestic equity funds experienced outflows of $7.88 billion, while world equity funds saw inflows of $9.46 billion. Bond funds attracted an estimated $18.43 billion in inflows during the same period. Market sentiment grew cautious by week's end, largely due to Federal Reserve leadership uncertainty and mixed earnings reports, contributing to a "risk-off" environment.

Overall Assessment: The market's week was characterized by early strength driven by positive corporate earnings, especially in the technology sector, but ended with increased volatility and a cautious tone. This shift was largely attributable to concerns surrounding Federal Reserve policy and potential changes in leadership, alongside sector-specific headwinds. Economic fundamentals remained broadly supportive, but investor sentiment turned sensitive to policy and earnings surprises.

Next Week’s key market drivers & Investment Outlook

Upcoming Events: The coming week features several key economic data releases. Monday, February 2, will see the release of December 2025 Job Openings and Labor Turnover Survey (JOLTS) data, Q4 2025 Housing Vacancies & Homeownership, and January 2026 Vehicle Sales. On Tuesday, February 3, the ISM Nonmanufacturing Index for January 2026 and Oil Inventories for January 30 are scheduled. The Employment Situation for January 2026 will be a key release on Thursday, February 5. Additionally, more corporate earnings reports are anticipated, alongside U.S. Retail Sales for January.

Market Logic Projection: The market is expected to remain highly attentive to signals regarding the Federal Reserve's future interest rate path, particularly given recent policy and leadership developments. Continued focus will be on incoming inflation and labor market data, which will heavily influence expectations for potential rate cuts.

Strategy & Allocation Recommendations: J.P. Morgan Global Research maintains a positive outlook for global equities in 2026, foreseeing double-digit gains supported by strong earnings growth, lower rates, and the ongoing influence of AI. Investors should evaluate the sustainability of broadening market leadership and consider positioning for a more balanced economic cycle. Fiscal stimulus and tax cuts are expected to continue supporting U.S. consumer and business spending in 2026.

Risk Alerts: Elevated geopolitical tensions remain a significant global risk. The possibility of an "AI Bubble" bursting, should tech companies struggle to monetize AI investments, poses a substantial threat to tech stocks and could potentially trigger a U.S. recession. Risks of an inflation resurgence, whether from AI supply bottlenecks or expansionary fiscal policies like "tariff rebates," warrant close monitoring. Persistent policy uncertainty in fiscal, trade, and immigration domains, alongside sustained high government bond yields, presents downside risks to economic growth.

Markets Weekly

5-Day Index Performance

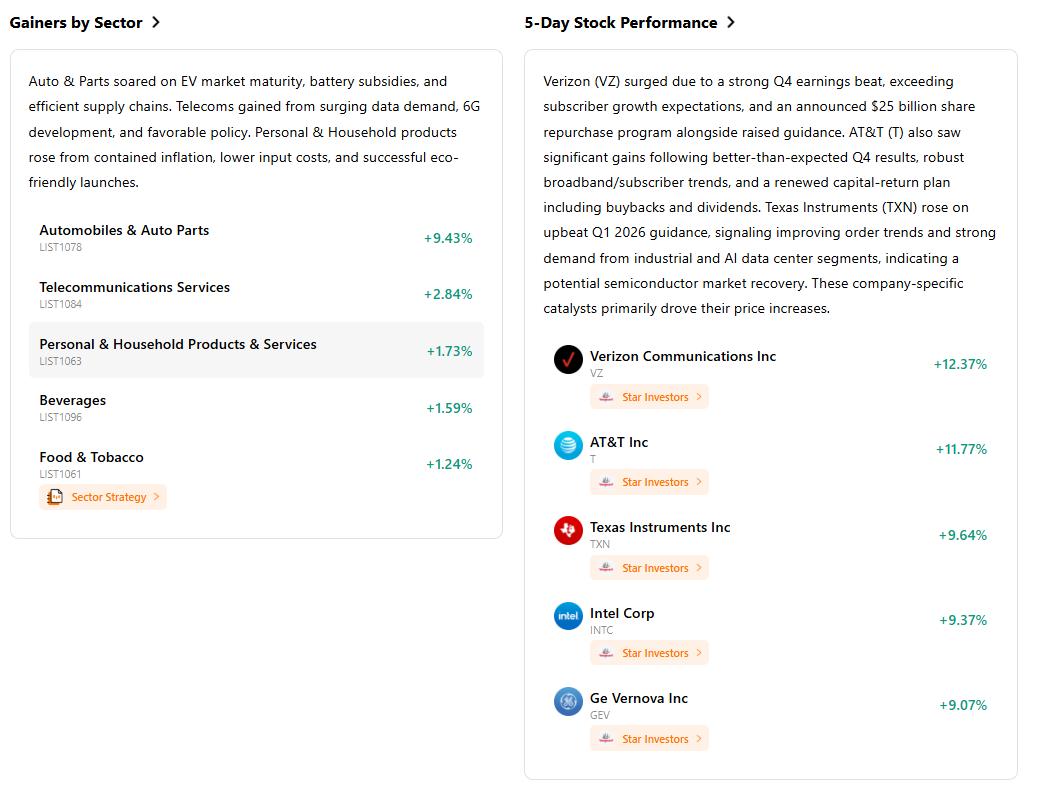

Recommended Articles