Is the Chip Stock Cycle Here? ASML Price Targets Raised by Morgan Stanley and UBS Ahead of Earnings. Three Key Focuses for Q4 Earnings.

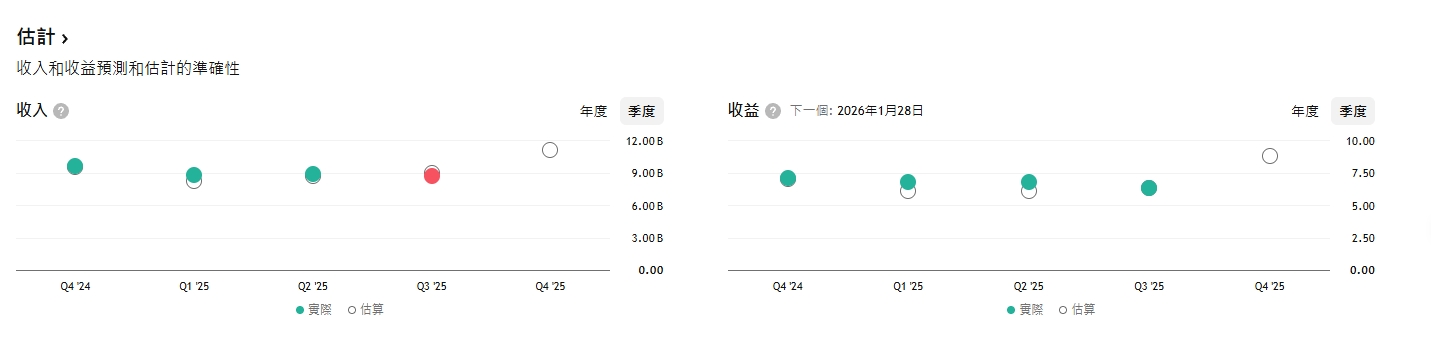

TradingKey - Before the U.S. market opens on Wednesday, January 28, Dutch lithography giant ASML (ASML) will release its Q4 2025 and full-year financial results and provide specific performance guidance for 2026. Previously, the company provided preliminary data: Q4 revenue is expected to be between ‐9.2 billion and ‐9.8 billion, with a gross margin of 51–53%, while stating that 2026 revenue will not be lower than in 2025.

Ahead of the earnings release, Wall Street giant Morgan Stanley has named ASML its top pick among European semiconductor stocks. Both Morgan Stanley and UBS have raised their price targets to ‐1,400, while JPMorgan has set a target of $1,518. UBS further believes that the company's earnings expectations for 2026 and 2027 are approximately 25% higher than the market consensus.

Can Q4 performance support the 30% year-to-date rally?

Prior to the Q4 results, ASML provided a forecast for the current quarter: revenue between ‐9.2 billion and ‐9.8 billion, and a gross margin of 51–53%. Additionally, ASML projected that full-year 2025 revenue will grow by approximately 15% from ‐28.3 billion in 2024 to about ‐32.5 billion, with a full-year gross margin of roughly 52%.

Investment bank forecasts are also quite optimistic. According to a Morgan Stanley research report, ASML's Q4 bookings may exceed market expectations. JPMorgan stated that driven by orders from TSMC and Samsung Electronics, ASML's Q4 bookings are expected to reach ‐7 billion, about 4% above consensus, with most Q4 orders tied to shipments in 2027.

While these figures seem positive at first glance, given that the stock has surged nearly 30% since January (as of the U.S. market close on January 24), there is a need to be cautious about a "sell the news" scenario.

On January 15, TSMC announced its 2026 capital expenditure would increase to $52–$56 billion, sparking a rally in semiconductor stocks. ASML's European shares hit a record high of ‐1,167 intraday, with its market capitalization surpassing $500 billion, making it Europe's most valuable company. Rating agency Morningstar believes this will provide a tangible benefit to ASML, as TSMC’s need for new capacity should translate into new orders for the company.

However, despite these tailwinds, ASML’s outlook remains quite conservative, only projecting that 2026 revenue will not be lower than the previous year, while also signaling a bearish outlook for declining revenue from the Chinese market.

In this earnings report, the focus should not only be on whether ASML's Q4 results reach the guidance range, but also on whether they fall near the upper or lower end . If Q4 revenue and gross margin merely meet the guidance range without further positive catalysts, the stock may face significant upward pressure. Given that the market has already priced in these positives and shares have climbed nearly 30% this month, coupled with ASML's conservative guidance, investors may opt for profit-taking.

Guidance is more important than actual results

Analysts believe the market needs to focus most on the company’s 2026 and 2030 performance guidance. Many investment banks have raised their expectations for the company ahead of the results.

Morgan Stanley analysts stated that due to increased fab and memory capital expenditure in 2027, along with better-than-expected demand in China, they are more confident in higher earnings for ASML in FY2027, expecting bookings in the next 2-3 quarters to reflect this strong momentum.

UBS expects revenue to grow by 23% in 2026 and 14% in 2027, a significant increase from previous forecasts. In the memory sector, UBS anticipates a strong DRAM capital expenditure cycle in 2026, driving ASML’s memory revenue up by 40%. Additionally, given expectations of a 7% increase in 2027 capex for TSMC, a major customer, UBS also raised its revenue projections for ASML's logic segment. Previously, UBS expected 2026 revenue from China to decline, but it has now revised its forecast to be flat year-over-year. These projections support UBS's higher price target for ASML.

With Wall Street expectations set so high, if ASML fails to provide more detailed or better-than-expected guidance—offering only the already-priced-in forecast that 2026 revenue will exceed 2025—the stock's rally will be difficult to sustain.

How ASML responds to market skepticism

Despite the high hopes from investment banks for this quarter and the next two years, the company still needs to address its primary risks: the downward revision of revenue expectations from the China market and tariff risks.

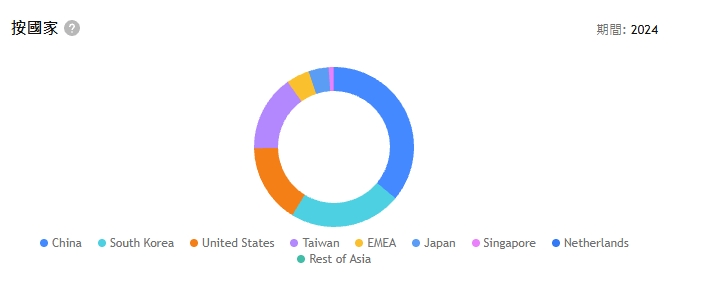

The company stated prior to the results that 2026 revenue from China would decline due to export controls and progress in domestic Chinese lithography technology. The China market contributed significantly to ASML's revenue in 2024–2025: in 2024, revenue from China was ‐10.195 billion, or 36.1% of total revenue; in Q3 2025, it accounted for a staggering 42%. As one of ASML's largest markets, revenue from China will largely determine its total top line.

Additionally, the recent Greenland controversy has highlighted fractures in U.S.-Europe relations, leaving the market deeply concerned about uncertainties surrounding potential tariffs.

ASML's conservative guidance has already tempered the market's high expectations, but these two risks remain unavoidable topics. Will revenue from the China market actually decrease? By how much? If it does, can strong DRAM demand offset the loss? If tariffs continue to rise, who will bear the cost? To what extent will it erode gross margins?

If ASML cannot provide more detailed responses to these questions, the stock will be impacted not only by sentiment from lower-than-expected forecasts but also by pessimistic company fundamentals over the next two years.

Recommended Articles