Alphabet Q3 Earnings: Ad Business is Thriving Amid More AI

Summary

TradingKey - In 2025, Alphabet has been a great turnaround story. The stock price experienced a significant rebound with a year-to-date performance of +45% - the best among all Mag 7 stocks. Within this period, we saw the narrative change from “Google losing market share and getting killed by OpenAI” to “Google becoming the ultimate AI play, and a main threat to OpenAI's ambitions”.

Alphabet's stock price re-rated from 21x PE at the beginning of the year to 27x PE now. We still think this is an attractive valuation considering the current momentum of their operations and the vast opportunities ahead of the company when it comes to AI.

Earnings Overview

Revenue reached above $100 billion for the first time, growing at 16%. The EPS was $2.87, or up 35%. That includes the one-off European Commission (EC) fine of $3.5 billion impacting the operating income. The solid beat made the stock jump over 6-7% in the after-hours.

Google Search Advertising revenue was up 15% driven by an increase in queries from AI Overviews and AI Mode – the AI tools that appear at the top of the search results. Many were concerned that these tools would cannibalize the ad revenue, but in fact, they actually increased the ad inventory.

YouTube advertising revenue also went up 15% mainly due to YouTube Shorts. Revenue from the short-form videos was up 50% and the overall time spent on watching YouTube grew 20% year over year.

Google Network, which represents the ad revenue from 3rd party websites, has been down 2.6%, another quarter of decline, mostly because the new AI Features reduce the traffic to third-party website publishers, moving ad money to Google Search and YouTube.

Google Subscriptions, which is predominantly from YouTube Premium, YouTube TV, Google One and Google Play and the B2C side of Gemini, went up 20% mostly due to strong demand for Google One (AI storage) and YouTube (Premium, TV and Music).

Google Cloud revenue was up 33.5%, another quarter with hyper growth, driven by Gemini VertexAI, a unified, managed platform on Google Cloud for building, deploying, and scaling machine learning and generative AI models. The TPU business also contributed, even though this is still a small portion of the total Cloud revenue.

The operating margin remained strong at above 30%, despite the EC fine.

The balance sheet remained strong with a cash position of $23 billion, marketable securities at $75 billion and long-term debt at $21 billion.

The operating cash flow was $48 billion, while the Capex spent for the quarter was $24 billion, implying free cash flows of approximately $25 billion, $11 billion of which were spent on share buybacks.

Guidance and Future Drivers

In terms of guidance, the management raised their CapEx estimate for 2025 to $91B–$93B (up from prior $85B guidance), with an even greater increase in 2026. Also, revenue growth is expected to remain double-digit.

When it comes to future growth, AI Overviews and AI Mode will drive user traffic. Also, we see various new functionalities on the search engine, such as hiding sponsored results, allowing users to collapse text ads with a single click & view only organic results. This control may help improve user experience and traffic without sacrificing ad revenue.

On the YouTube side, there is also a lot of room for further integration with various functions, such as more automated shop functions on YouTube. Also, a more enhanced recommendation algorithm will help better connect content to the desired audience and also advertise to the desired audience.

Google Cloud is growing at peak rates of 30%+ year-over-year. Even if we see de-ecceleration, the margin at 22% is still not mature. Cloud peers have margins of around 30%, so gradually, Google Cloud will move towards that level. Not to mention that the TPU is a fast-growing segment within the cloud that also has a higher margin.

Source: Company Financials

In terms of margins, there might be a limited upside, as we can see several headwinds - more infrastructure costs, depreciation and hiring-related expenses.

OpenAI: Threat and Moat

The competition with OpenAI is something that will determine the future of Alphabet and the stock price.

Sam Altman’s company remains the biggest risk for Google in the long term. Currently, OpenAI is dominating with ChatGPT having 800 million weekly users, higher than Google’s Gemini of 650 million monthly users.

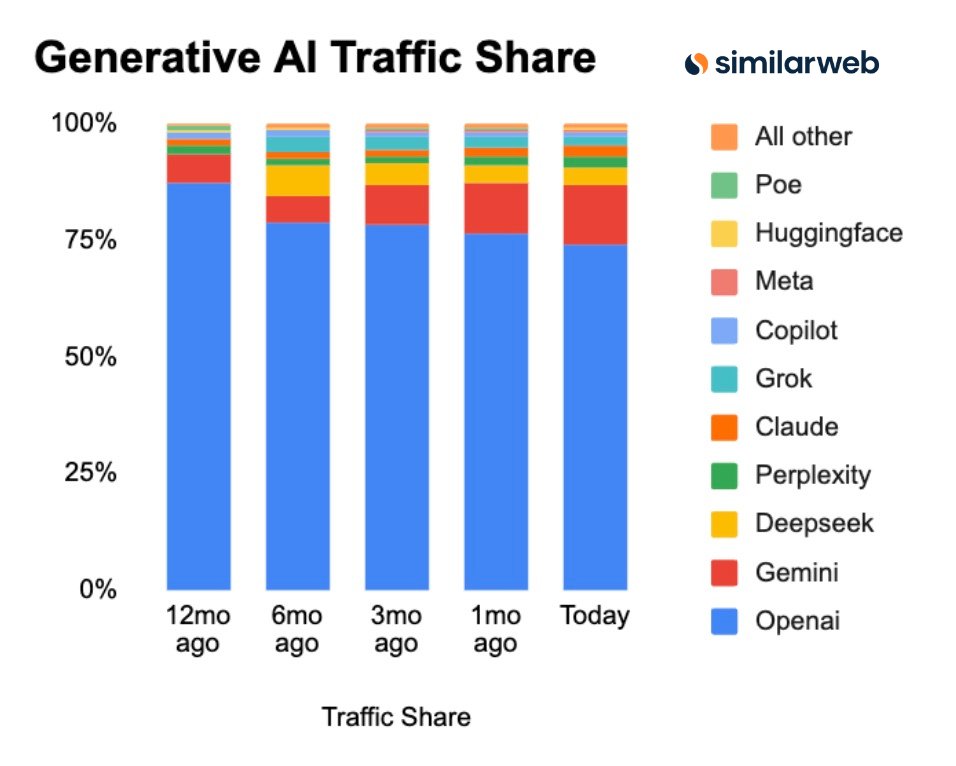

What OpenAI has been doing recently is establishing numerous partnerships with other firms like Shopify, Walmart, Spotify, Etsy, Figma and others. The goal is to create an ecosystem that can solidify OpenAI’s importance in the AI value chain. The stronger the partnership ecosystem OpenAI has, the less need there will be for users to rely on the Google ecosystem. This is all part of the plan for OpenAI to disrupt the whole app industry, and this disruption itself is the main risk for Google.

Source: SimilarWeb

Also, when it comes to Gemini vs ChatGPT, even though OpenAI is not monetising through ads, we expect they may roll out an ad tool in the coming 1-2 years, directly aiming at the advertisers who use the Google ad platform. That’s why Google has to act fast and further scale Gemini to make it an equal competitor to ChatGPT.

However, there are a couple of risk mitigants or advantages that are in favour of Alphabet.

Google Distribution Network

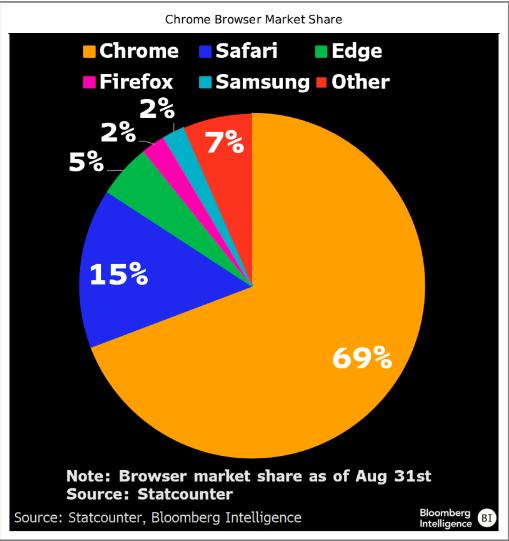

Potential risk mitigant against OpenAI is the solid app ecosystem Google has created, we can see this with the recent launch of OpenAI’s Atlas web browser, which received an underwhelming user reactions because the browser was mostly based on Google Chrome infrastructure, and it is simply much of a smoother user experience utilising Chrome along with Gmail, Drive, YouTube and the other apps from the family.

In fact, the decision of the DOJ not to break Chrome away from Alphabet is a major win for Google because Chrome, with its 70% market share among web browsers, is the main supporting pillar for Google's dominance among the search engines.

Also, Google generously pays 50%of its TAC to Apple, or $20 billion in 2024, to support Google on iPhones. Thus, Google secures both Android (owned by them) and iOS, the two main operating systems, as their distributors.

Source: Bloomberg Intelligence

In the situation of dominating the web browser market and the operating system market, Google just needs to come up with a good-enough AI product, as they don’t have to outperform ChatGPT in terms of functionality. They can just rely on their distribution network to do the job.

Another advantage of Alphabet is its vertical integration - both upstream and downstream. Unlike OpenAI, Google has already established apps (YouTube, Maps, Drive, Mail), and they also have a Cloud business and TPUs. We should also note that even OpenAI still uses Google Cloud, demonstrating the level of penetration of Alphabet in every stage of the AI value chain.

Last but not least, we have the power of Alphabet’s healthy financials. GOOGL has a long track record of profitability and positive cash flows that support one of the healthiest balance sheets out there, and we cannot say the same for OpenAI, where the profitability is not visible for the coming years.

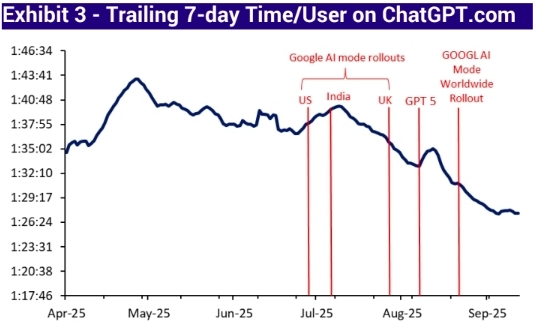

As a result of all the things mentioned above, we can see how Google AI models may actually contribute to the decline of time per user on ChatGPT directly.

Source: SimilarWeb

Other Risks

Macro headwinds (e.g., slowing ad budgets) are still on the table as a potential risk, especially in the context of the mixed macro picture. However, AI will help Google lift up the ad targeting capabilities, therefore keeping the ad revenue growth at high single-digit or above.

Another potential risk is the deal with Apple that expires in 2026. As we saw above, Google pays a generous amount to secure the default status of its search engine on Apple devices. There is always a risk of not being able to renew this agreement or renew it on less favorable terms to Google.

The cloud industry is another intense battlefield for Google. The landscape becomes even more competitive with existing cloud giants like AWS and Azure, joined by emerging players like Oracle, CoreWeave and Alibaba. There is always a risk of Google losing momentum and market share.

Valuation

Currently, GOOGL is trading at 28x PE. Overall, this is around the historical average for the stock; however, as Google becomes more and more AI-native, the stock will deserve a higher multiple, perhaps 33–35x, implying a stock price of around $300 per share, or 15% upside.

Get Started

Recommended Articles