Apple Q4 Earnings Preview: iPhone 17 Challenges a Super Cycle, Services to Lead Profitability

- Gold Price Trend Forecast: Expectations of Easing US-Iran Tensions Boost Gold Prices, $4,070 Becomes Key Level for Bulls and Bears

- Gold Price Trend Forecast: Why Did Gold Prices Fall After US CPI Cooled? Fed Chair Speech and Iran Situation Become Obstacles

- TradingKey Daily Market Brief: Gold Falls Below $4,000, TSMC’s Strong Earnings Fail to Stop AI Trade Cooling, Chip Stocks Sold Off

- Gold Price Forecast: Cooling Inflation Fails to Offset Fed Hawkish Pressure, Gold Price May Fall to $3,500

- Euro declines to near 1.1400 as US launches fresh strikes on Iran

- Tesla Q2 Earnings Preview: Record Deliveries Fail to Hide Profit Pressure, Can Musk Rely on AI and Autonomous Driving to Unlock New Growth Space?

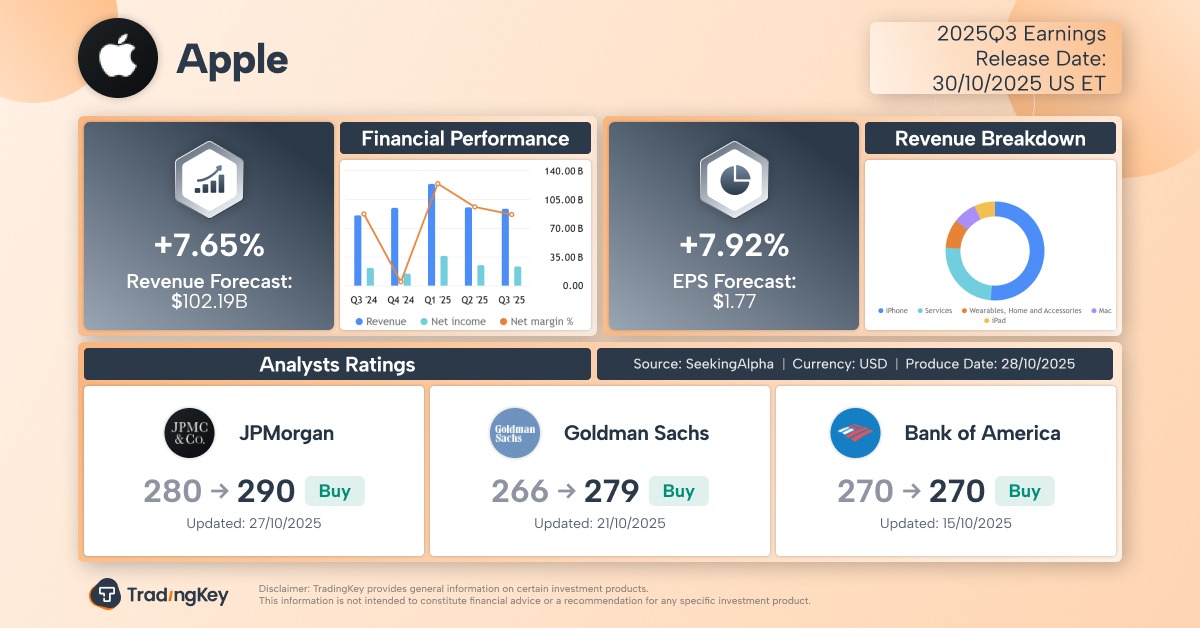

TradingKey - Apple (AAPL), the third company in history to surpass a $4 trillion market cap, will report its Q4 2025 earnings (natural Q3) after market close on Thursday, October 30. For investors in this iPhone design and R&D powerhouse, Q3 may deliver another strong performance — driven by the iPhone 17 launch, services profit overtaking hardware, and easing trade tensions.

According to Seeking Alpha, Wall Street analysts expect:

Revenue: $102.19 billion, up 7.65% YoY from $94.93B

EPS: $1.77, up 7.92% YoY from $1.64

This would mark Apple’s first quarter above $100 billion in revenue since early 2025, fueled by:

A recovery in China

Strong late-quarter sales of the iPhone 17 in key markets

Resilient growth in services

Apple has beaten EPS expectations in 10 of the past 11 quarters — yet its stock has declined the day after earnings in four of the last five reports, highlighting that even strong results don’t guarantee short-term gains.

The iPhone “Super Cycle” Debate

As the smartphone industry rebounds from a downturn, Apple’s iPhone is regaining momentum. In Q2, Apple saw growth in both China and Western markets, with Greater China posting its first positive growth since Q2 2023 — boosted by government subsidies on iPhone purchases.

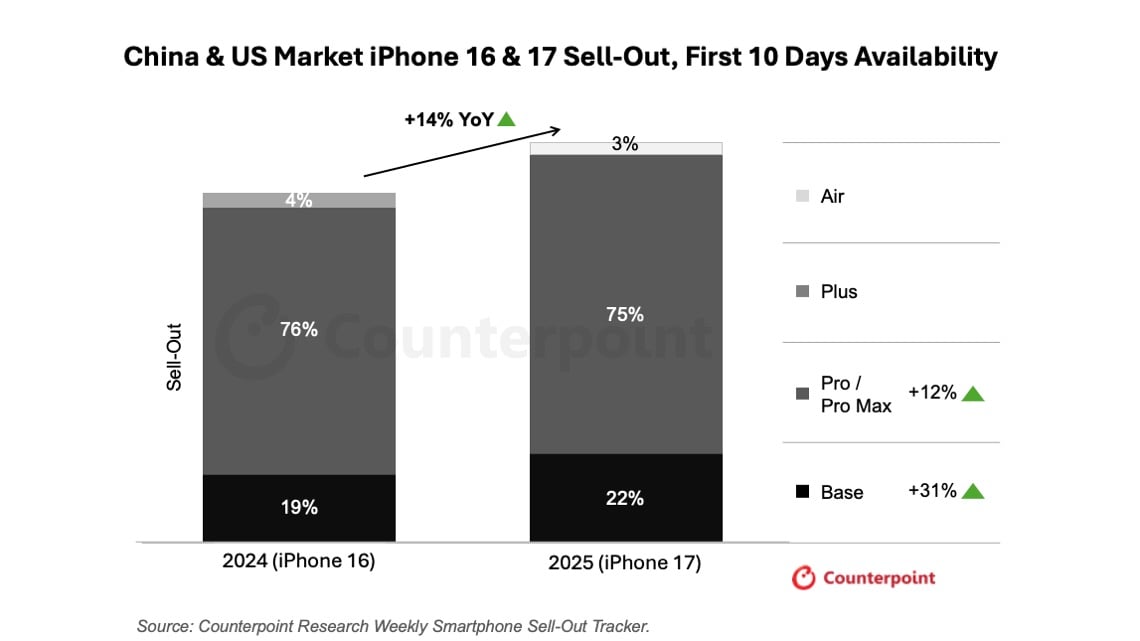

Although the iPhone 17 series, launched in late September, contributed only about 10 days of sales to Q3, its strong debut will influence both results and forward guidance.

Counterpoint Research found that iPhone 17 sales in the first 10 days after launch were 14% higher than the previous-generation iPhone 16 in the U.S. and China.

Source: Counterpoint Research

Omdia noted that global smartphone shipments resumed growth in Q3 after early-year volatility, with iPhone shipments up 4% YoY — marking the strongest Q3 in history. The firm said iPhone 17’s early demand helped Apple capture an 18% share of the global smartphone market.

Analysts project:

iPhone net sales: +7.6% YoY to $49.75 billion

Greater China revenue: +8% YoY to $16.23 billion

Evercore ISI believes the new iPhone could push Q3 results above consensus and provide optimistic guidance for Q4. Given multiple positive indicators, this upgrade cycle may be stronger than usual.

Goldman Sachs cited longer delivery times, higher production targets, and positive carrier feedback as signs that iPhone 17 demand may exceed iPhone 16.

They asked, “Are we entering an iPhone super cycle?” — though the bank remains cautiously optimistic.

Evercore ISI added that the September quarter report will reveal whether strong June quarter performance was a one-off or a sign of a structural shift in iPhone replacement cycles.

Recent reports suggest weakening demand and production cuts for the new iPhone Air model. Well-known Apple supply chain analyst Ming-Chi Kuo said the Air didn’t meet expectations.

But he noted this reflects how well the Pro and standard models already cover high-end user needs, leaving little room for new segments.

Industry experts say the Air’s relative “underperformance” doesn’t undermine the broader upgrade narrative.

Goldman Sachs believes Apple can maintain smartphone appeal through design innovation — such as launching its first foldable iPhone next year and a true edge-to-edge “all-glass” iPhone in 2027.

Services to Become Apple’s Profit Engine

For years, Apple has been synonymous with iPhone, iPad, and Mac — its core hardware revenue drivers. But now, services — including iCloud, Apple Music, and the App Store — are reshaping Apple’s profitability.

Apple’s service bundle now has over 1 billion paid subscribers globally, spanning Apple TV+, Apple News+, Apple Card, and more.

In Q2, services posted a 75.6% gross margin, far exceeding hardware’s 34.5%. Analysts expect services to maintain a 70%+ margin in Q3, while product margins are expected around 36%.

After double-digit growth of 12% (Q1) and 13.3% (Q2), analysts forecast:

Services revenue: +12.3% YoY to $26.96 billion

Goldman Sachs estimate: +13% to $28.2 billion

Bank of America reported two months ago that Apple is undergoing a “deep business transformation,” projecting that services will account for 42% of Apple’s gross profit in FY2025, compared to 41% for iPhone — the first time services will surpass iPhone.

Evercore ISI, expecting continued double-digit service growth, noted that headwinds like the DOJ’s antitrust case against Google and the Apple-Epic litigation have eased in Q3.

Apple’s AI Progress: Important, But Not Critical

Apple’s perceived lag in AI is frequently discussed — but is it really behind?

Apple hasn’t stood still:

Purchased Nvidia GPUs for AI training

Adapted its MLX framework to support CUDA

Integrated OpenAI’s ChatGPT into iOS 18, iPadOS 18, and macOS 18

Unlike the iPhone 16 launch, where AI dominated the presentation, CEO Tim Cook mentioned Apple Intelligence sparingly during the iPhone 17 event — focusing instead on how new devices support AI.

Analyst Mark Gurman noted that internal strategic indecision and departmental friction have kept Apple reactive in AI.

While many argue Apple is falling behind in AI innovation, others say AI isn’t essential to drive iPhone upgrades. A CNET survey found only 11% of U.S. smartphone users would switch phones solely for AI.

As Apple crossed the $4 trillion milestone, Wedbush analyst Dan Ives said that even if Apple missed the AI wave, reaching $4T is a watershed moment — proof of the world’s strongest consumer brand.

Is Apple Stock a Buy?

Driven by improving U.S.-China trade talks and a rebounding iPhone cycle, Apple shares recently hit an all-time high. Year-to-date, AAPL is up 7.70%, with a +4% gain in the past five days.

Per TradingKey, the average analyst target price is $257.46 — below the current $269.70, suggesting some caution.

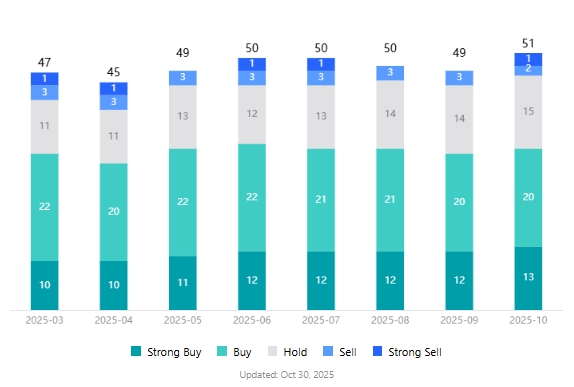

Overall, analysts remain bullish:

Of 51 analysts covering AAPL, only 3 rate “Sell”

65% recommend “Buy”

Analyst Ratings for Apple Stock, Source: TradingKey

Wamsi Mohan, Bank of America analyst, raised his target from $270 to $320 on Wednesday, calling Apple the “ultimate winner in edge AI” with strategic options across new products and markets.

JPMorgan raised its target from $280 to $290 on Monday, noting Apple is entering earnings season with its most positive momentum in a year. Market focus centers on:

iPhone 17 sales performance

Outlook for the upcoming iPhone 18

Risks remain: How sustainable is iPhone demand? And what impact will tariffs and macroeconomic headwinds have on consumer spending?

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.