Who Smokes Whom? Altria and Philip Morris International for Tobacco Supremacy

Investment Thesis

TradingKey - As a U.S. tobacco giant, Altria dominates the cigarette market through subsidiaries like Philip Morris USA but faces severe challenges from declining sales and competition from illicit e-cigarettes. Its revenue structure heavily relies on combustible tobacco, and while pricing power sustains profitability, its smokeless transition is hindered by patent litigation and regulatory pressures. Historical investment missteps have further widened the stock price gap with Philip Morris International. Although EPS is expected to grow in the low single digits over the next three years, and a 6.18% dividend yield attracts income-focused investors, the high 78% payout ratio and transition execution risks may threaten sustainability. The valuation range is estimated at $59–$71, but long-term growth depends on smokeless product breakthroughs; otherwise, valuation compression and dividend adjustment pressures may arise.

.jpg)

Source: TradingView

Source: Altria Group, TradingKey

Company Overview

Altria Group Inc. is a holding company responsible for managing and coordinating its subsidiaries’ operations in producing and marketing various tobacco products for U.S. consumers aged 21 and older. Altria itself does not directly engage in production or sales but operates through its subsidiaries, including Philip Morris USA, U.S. Smokeless Tobacco Company, and NJOY, each focusing on different tobacco product categories:

- Smokeable Products: Philip Morris USA produces combustible cigarettes, while Middleton manufactures large cigars and pipe tobacco.

- Oral Tobacco Products: U.S. Smokeless Tobacco Company produces moist smokeless tobacco (MST) and snuff products, while Helix Innovations produces oral nicotine pouches (e.g., the On! brand).

- E-Vapor Products: NJOY produces and markets e-cigarette products.

As the parent company, Altria is responsible for strategic planning, resource allocation, and overall management, ensuring its products are distributed to the market through wholesalers. It’s worth emphasizing that before 2008, Philip Morris International (PM) and Philip Morris USA were both part of Altria (then called Philip Morris Companies Inc.). To separate U.S. and international tobacco operations, Altria spun off PMI as an independent public company (ticker: PM) in 2008, focusing on international markets, while Philip Morris USA, a wholly-owned subsidiary of Altria, focuses on the U.S. market. The two operate independently, with brands like Marlboro licensed under the spinoff agreement: PM holds international market rights, and Philip Morris USA holds U.S. market rights, with no equity or direct operational control between them.

U.S. Tobacco Industry Competitive Analysis

Industry Overview

The U.S., a major global tobacco producer, is dominated by a few large companies, with Altria as the industry leader. Cigarettes account for nearly 70% of the market, cigars/small cigars about 14%, smokeless tobacco around 7%, oral nicotine products 5%, and e-cigarettes approximately 4% (data source: Tobacco Prevention and Cessation).

Declining cigarette sales have become a long-term trend. According to Altria’s data, U.S. cigarette shipments fell by about 8.5% in the first half of 2025, adjusted. While the North American e-cigarette market is expected to grow from $1.08 billion in 2025 to a higher level by 2030 (CAGR of 5.54%, per Statista), illicit products (accounting for 86% of market share) severely erode the growth potential of legal companies, causing pricing pressure for Altria’s NJOY and making substantial R&D and regulatory compliance investments difficult to yield expected returns. In contrast, the smokeless tobacco market is steadily growing, projected to rise from $1.335 billion in 2024 to $1.773 billion by 2033 (CAGR of 3.20%), with a North American CAGR of about 4.3% from 2025–2035. Oral nicotine products surpassed e-cigarettes in 2022 to become the fourth-largest category, reflecting consumer preference for discreet, convenient, and lower-risk nicotine alternatives.

.jpg)

Source: ResearchAndMarkets

Competitive Landscape

Altria faces intense competition from players like Philip Morris International (PMI), British American Tobacco (BAT), Imperial Brands, Reynolds American Inc., Japan Tobacco, and Turning Point Brands. The industry is broadly impacted by declining cigarette sales, rising health awareness, regulatory pressures (e.g., product bans), and illicit markets, but Altria maintains competitiveness through pricing strategies and a transition to smokeless products.

Altria and PMI split in 2008, with the former focusing on the U.S. and the latter on international markets. However, the rise of reduced-risk products (RRPs) has led to direct competition in emerging areas: PM’s Zyn and IQOS (previously licensed to Altria) compete with Altria’s NJOY and On!. This shift disrupts the geographic separation, with PM’s global RRP experience and brand success (e.g., IQOS’s global achievements) posing a greater threat in the U.S. market. This requires Altria to address both traditional cigarette declines and competition from well-funded global rivals in growth areas.

Revenue Structure

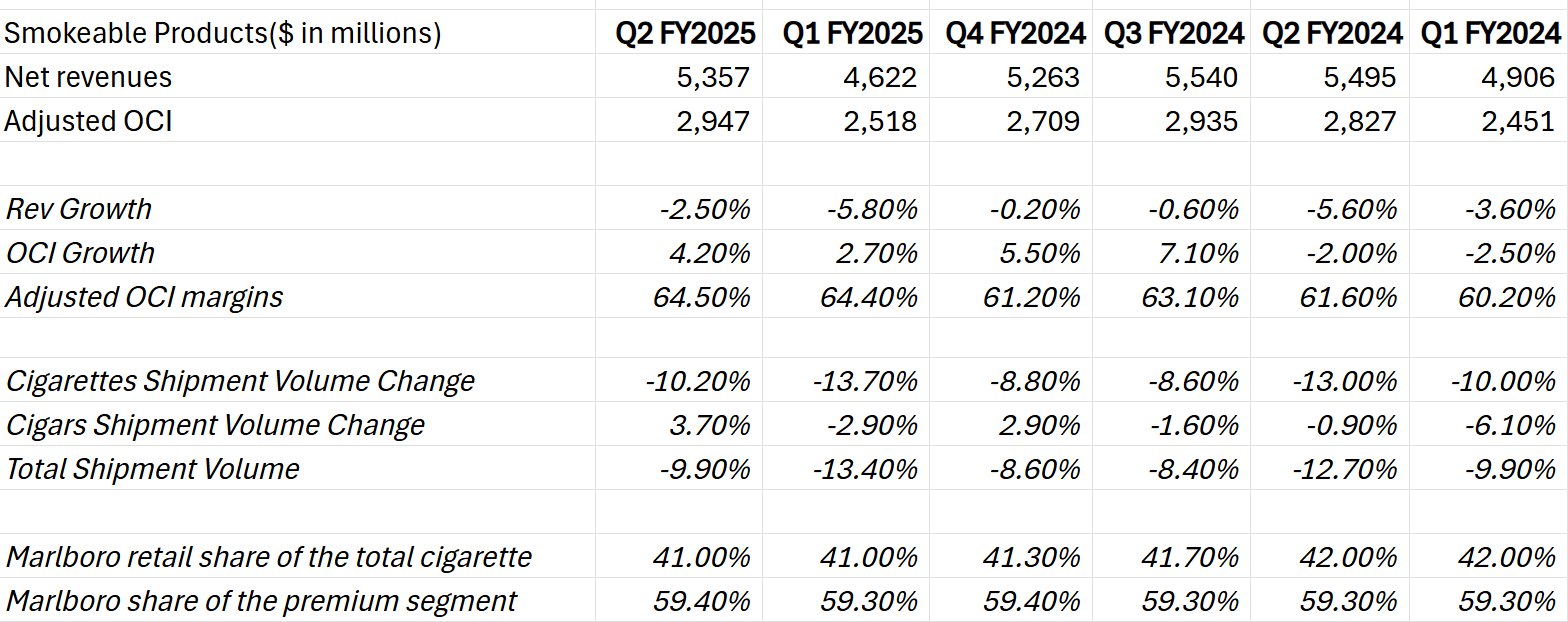

Smokeable Products

Smokeable tobacco products are Altria’s core revenue source, accounting for 88% of total revenue in Q2 2025, with cigarette shipments comprising 97% of this category and Altria holding a 45.2% retail cigarette share. However, this segment faces significant volume decline pressure, with net revenue growth slowing since Q1 2024 due to a near double-digit drop in cigarette shipments. Contributing factors include the rapid growth of flavored disposable e-cigarettes (often evading regulation), disposable income pressures for adult tobacco consumers (ATC), and a shift toward alternative products. Nonetheless, adjusted operating companies’ income (OCI) grew, with margins rising to 64.5%, driven by strong brand pricing power, strict cost controls, and relatively low consumer price sensitivity. However, relying on price increases and efficiency gains to sustain profitability has limits; if volumes continue to decline or consumer price sensitivity reaches a threshold, margin resilience may falter.

Marlboro, Altria’s flagship brand, holds a 41.0% retail share of the U.S. cigarette market, down 1% from 2024, but maintains a stable 59.4% share in the premium segment. As a “cash cow,” Marlboro’s high loyalty makes any market share fluctuations significant, reflecting a structural shift from traditional cigarettes to alternative products (including Altria’s RRPs and competitors’ offerings). This underscores the urgency and necessity of Altria’s “Moving Beyond Smoking” strategy.

Source: Company Reports, TradingKey

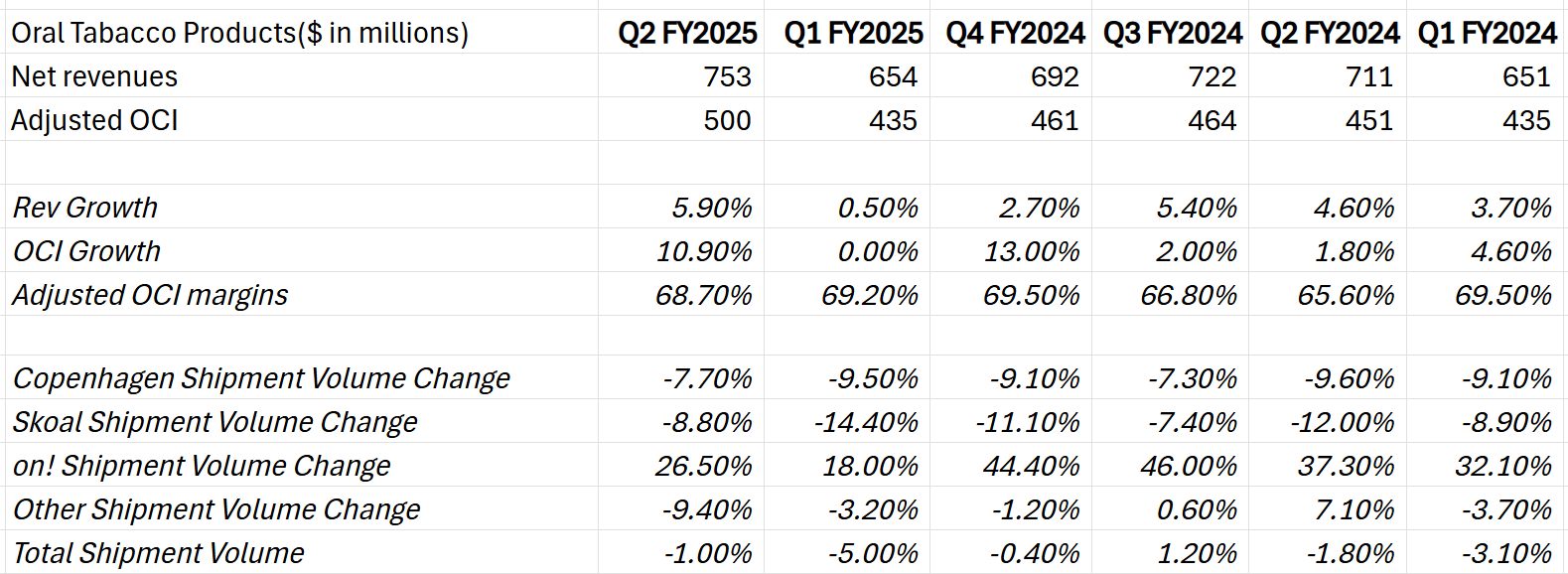

Oral Tobacco Products

Oral tobacco products are a healthy growth area for Altria, with Q2 2025 adjusted OCI growing nearly 11% year-over-year, achieving a 69% margin, surpassing combustible tobacco. However, performance within the category varies: traditional moist smokeless tobacco (MST, e.g., Copenhagen and Skoal) retail share declined due to lower shipments, while smokeless nicotine pouches like On! saw steady retail share and shipment growth, indicating internal “cannibalization.” On!, with its clean taste, discreet use, and lower health risks, attracts modern, younger users, while Copenhagen and Skoal, with tobacco content, bold flavors, and higher health risks, target traditional users. Despite overall revenue growth in oral tobacco, growth stems partly from consumers shifting from higher-margin MST to On!, potentially weakening traditional product profitability. On!’s rising share in the oral tobacco category highlights Altria’s success in transitioning to RRPs. If this model can be replicated in e-cigarettes or other RRPs, it could significantly boost investor confidence in Altria’s future growth potential.

Source: Company Reports, TradingKey

Analysis of Stock Price Disparities

Since the pandemic period in 2020, the stock price gap between Altria Group (MO) and Philip Morris International (PM) has widened. This divergence is not accidental but driven by fundamental differences in market geography, RRP strategies and execution, historical investment impacts, and regulatory environments.

Market Geography Differences

Altria is constrained by the shrinking U.S. market and high illicit e-cigarette penetration, facing dual pressures of declining cigarette volumes and illicit competition in e-cigarettes, limiting both traditional and emerging businesses. In contrast, PMI focuses on international markets, benefiting from global market diversity and regulatory variations, with slower traditional cigarette declines and higher RRP acceptance.

Reduced-Risk Product Strategy

PMI excels in smokeless products, investing over $12.5 billion since 2008, with core brands IQOS and ZYN sold in 84 global markets, over 20 million adults switching to IQOS and quitting smoking, and ZYN diversifying its portfolio to reduce single-product reliance. Altria, however, suffered from failed non-cigarette investments (notably Juul), losing billions. Although it acquired NJOY, its transition lags, with market share trailing PMI’s smokeless business.

Historical Investments and Asset Impairment Impacts

Altria’s Juul investment significantly dragged its stock performance. In 2018, Altria acquired a 35% stake in Juul for $12.8 billion, followed by a $4.5 billion write-down in 2019, with the investment value dropping to 5% by 2022, incurring $8.6 billion in impairment charges. In March 2023, Altria swapped its Juul stake for heated tobacco intellectual property. This failure cost billions, damaging its balance sheet, profitability, and investor confidence. In contrast, PMI’s RRP investments yielded positive returns, driving performance and demonstrating superior strategic execution and capital allocation efficiency.

Regulatory Environment and Legal Risks

PMI’s global operations allow it to navigate diverse regulatory environments, diversifying single-market risks and advancing RRP expansion. Altria, concentrated in the U.S., faces stringent regulations and high litigation risks, making it more vulnerable to legal risks, increasing financial burdens, and reducing valuation and investment appeal compared to PMI.

Growth Potential

Reduced-Risk Product Strategy: Altria’s “Moving Beyond Smoking” vision aims to lead adult smokers toward a smokeless future by 2030, with 2025 goals to accelerate innovation in e-cigarettes, oral nicotine pouches, and heated tobacco. The target is to double U.S. smokeless product net revenue from $2.6 billion to $5 billion by 2028 (with innovative products contributing $2 billion). However, achieving this is challenging, requiring accelerated market penetration and innovation. Failure to meet these targets could dent investor confidence and long-term valuation. FDA authorizations are critical, providing competitive barriers, curbing illicit markets, and boosting consumer trust and market stability.

Key Investments and Innovation: Altria has adjusted its RRP investment strategy. In March 2023, it acquired NJOY for $2.75 billion, securing FDA-authorized NJOY ACE e-cigarettes, reflecting lessons learned from the Juul failure by investing in regulator-approved mature products to reduce risk and ensure stable growth. If patent disputes are resolved, NJOY ACE could return to the market, potentially contributing 15–20% of Altria’s smokeless revenue, driving EPS growth above 5%, given the e-cigarette market’s 8–12% CAGR. Altria also invested in cannabis company Cronos and clean energy drink Proper Wild, exploring non-nicotine areas to address tobacco industry decline and strict regulations, seeking diversified revenue streams. The success of these early investments will determine Altria’s long-term sustainable growth.

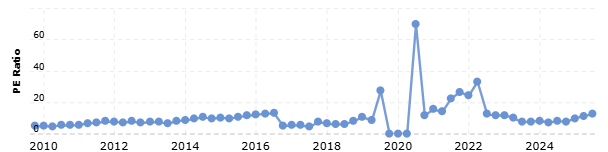

Valuation

The market expects Altria’s revenue to remain flat over the next three years, dragged down by declining traditional tobacco sales, but flexible pricing strategies and smokeless product revenue growth should maintain revenue stability. EPS is projected to grow in the low single digits, driven by effective cost controls, stock buybacks, and dividend reinvestment. Based on a reasonable valuation range of 11–13 times, Altria’s target stock price is estimated at $59–$71.

Source: macrotrends

Investment Recommendation

Philip Morris International (PM) excels in transitioning to smoke-free products like IQOS and ZYN, driving 40% of revenue from reduced-risk items with double-digit growth potential and high-teen EPS expansion, justifying its 36x PE premium. Altria (MO), focused on the U.S., relies on combustible tobacco (88% revenue) amid declining sales, but offers a 6.18% dividend yield with low-single-digit EPS growth.Income-focused investors suit Altria for stable dividends, tolerating high 78% payout ratios and transition risks. Growth-oriented investors fit PM for superior RRP momentum and global diversification.

For PM research report, see: Philip Morris International (PM): Successfully Moving Away from Traditional Products.

Risk

- Dividend Sustainability: Altria’s 6.18% dividend yield, with a 78% payout ratio and insufficient operating cash flow ($2.9 billion vs. $3.5 billion in dividends over the past six months), signals pressure on dividend sustainability. Declining core tobacco profits limit earnings, and a high payout ratio restricts reinvestment. If traditional business profits continue to shrink and new businesses fail to fill the gap, Altria may need to borrow or sell assets (e.g., IQOS commercialization rights) to maintain dividends, which is unsustainable long-term.

- Regulatory and Legal Pressures: Stringent FDA regulations and NJOY patent litigation may lead to product bans and impairment losses.

- Transition Failure Risk: If smokeless products fail, EPS growth could face pressure.

Get Started!

Recommended Articles