This Week’s CPI Follows Payrolls to Ignite Inflation Fears, Will Fed Rate Hike Option Return?

TradingKey - Following the severe volatility of last Friday's "Black Friday," Wall Street is waiting with bated breath for the release of U.S. May Consumer Price Index (CPI) data this Wednesday. Traders broadly fear the report could show the largest inflationary spike in years, potentially quashing market hopes for a Federal Reserve rate cut this year while significantly bolstering rate hike expectations.

Traders anticipate that the May CPI could rise by approximately 4.3% year-on-year—which would mark its highest level since 2023—largely due to energy prices remaining elevated amid the ongoing stalemate in the Iran conflict.

Last week's robust non-farm payrolls triggered a sell-off.

The U.S. nonfarm payroll data for May, released last Friday, came as a surprise. Data showed that nonfarm employment grew by a net 172,000 during the month, nearly double the market expectation of 85,000, while the unemployment rate stayed at a low of 4.3% for the third consecutive month.

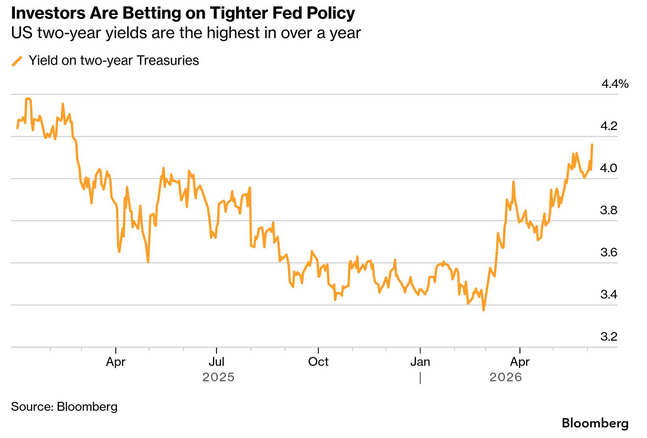

This stronger-than-expected jobs report triggered an immediate and sharp market reaction. The 10-year U.S. Treasury yield, known as the "anchor of global asset pricing," surged to 4.55%, a two-week high. The two-year yield, which is most sensitive to Federal Reserve policy expectations, touched 4.18%, its highest level since February 2025.

Simultaneously, the tech-heavy Nasdaq Composite Index suffered its largest single-day point drop in history, plunging more than 1,121 points, or 4.2%, while also recording its largest single-day percentage decline in over a year.

Fed rate cut expectations shattered

Since late February, global bond markets have undergone a profound shift. At that time, strikes by the U.S. and Israel on Iran triggered a surge in oil prices, completely disrupting market expectations that the Federal Reserve would cut interest rates in 2026.

As the conflict passes the 100-day mark, a lasting ceasefire appears out of reach, exerting further upward pressure on energy prices and intensifying inflation concerns. A resilient U.S. economy has added headwinds to the bond market while complicating the position of new Fed Chair Warsh, who may face political pressure from the White House to lower borrowing costs.

In the face of robust employment data and persistent inflationary pressures, major Wall Street investment banks have withdrawn their forecasts for interest rate cuts in 2026.

Last Friday, economists at BNP Paribas adjusted their forecasts to predict the Fed could hike rates up to three times, most likely starting in December.

Goldman Sachs ( GS) Chief U.S. Economist David Mericle has also completely abandoned expectations for Fed rate cuts this year, pushing back the two previously forecasted cuts significantly to June and December 2027. The Goldman Sachs report noted that the longer the rate pause lasts, the more it reinforces the view that rates are currently at a "reasonable level," while robust investment demand related to AI could provide further arguments for maintaining higher borrowing costs.

Consequently, Goldman Sachs stated that keeping rates unchanged remains a "viable alternative" outside its baseline forecast. Although Goldman believes the likelihood of resuming rate hikes remains limited, it has raised the probability from 10% to 20%. The firm also lowered its U.S. unemployment rate forecast for this year from 4.6% to 4.4%.

Meanwhile, interest rate swap market data showed that as of last Friday, traders had fully priced in one Fed rate hike within 2026, with the probability of an October hike hitting approximately 60% at one point, while a December hike is now considered a certainty.

Another risk indicator that cannot be ignored is the crossover between the unemployment rate and the CPI. There is a "low-probability but high-impact possibility" in May that the U.S. unemployment rate could equal or fall below the inflation rate, which would mark the seventh such occurrence since 1960.

In years when inflation approached or exceeded the unemployment rate (such as 1966, 1973, 2008, and 2021), the Fed typically resorted to rate hikes, and Wall Street's memories of those years are often painful.

Investor Alert

Beyond macroeconomic data, the greatest non-economic event risk in June stems from massive supply in the capital markets. SpaceX's initial public offering (IPO) is set to begin trading next Friday, which, alongside the offerings from Anthropic and OpenAI and the expiration of related lock-up periods, will drain record liquidity from the market.

For investors, the market is currently at a critical turning point. A shift in Federal Reserve policy expectations, persistent inflationary pressures, geopolitical tensions, and the looming liquidity withdrawal have converged to create a perfect storm.

If the inflation data released this week continues to exceed expectations, the Federal Reserve may be forced to adopt a more hawkish monetary policy, which would exert further pressure on risk assets and potentially trigger a new round of global market turmoil.

After years of a low-interest-rate environment, the market is facing the challenge of monetary policy normalization, which will have a profound impact on all asset classes. Investors need to reassess their portfolios to navigate the potential for higher interest rates and increased market volatility.

Recommended Articles