Economic Analysis and Outlook for Europe in 2026

Executive Summary

TradingKey - In 2025, the euro area economy exhibited the characteristics of a moderate recovery, yet its endogenous growth momentum remained insufficient. Based on a comprehensive assessment of the annual operation of the EU economy last year, the euro area economy is highly likely to maintain the tone of weak recovery in 2026. The core driving factors for European economic growth this year can be divided into two dimensions: endogenous and exogenous. On the endogenous front, the further intensification of fiscal expansion in Germany is expected to become the core engine driving the growth of the euro area economy. On the exogenous front, the implementation and entry into force of the US-EU trade agreement will effectively mitigate uncertainties in bilateral trade. It is projected that the export trade of the euro area will enter a trajectory of moderate recovery in 2026. The marginal easing of the impact of the Russia-Ukraine conflict is expected to prompt European countries to shift their sustained fiscal expenditures originally allocated to the battlefield in Ukraine to domestic sectors such as people's livelihood security, infrastructure investment and national defense construction, which also constitutes a realistic path for Europe to break the current economic predicament. Based on the above analysis, we judge that the euro area economy will sustain the moderate recovery trend in 2026, with its GDP growth rate likely to fall within the range of 1.2%-1.3%.

In terms of monetary policy, inflation in the euro area had gradually moved closer to the policy target last year, and it is projected to maintain a moderate downward trend in 2026. Supported by the fundamental backdrop of a mild economic recovery, the current policy rate corridor is expected to achieve the neutral regulatory objective of “neither constraining economic growth nor fuelling inflationary pressures”. Furthermore, the European Central Bank (ECB) has clearly stated that it will cease reinvesting the principal payments from maturing securities under the Asset Purchase Programme (APP) and the Pandemic Emergency Purchase Programme (PEPP). This measure marks a further transition of the ECB’s monetary policy framework from the quantitative easing phase to a regular liquidity management model.

The accommodative liquidity environment will provide solid support for European equity markets. Coupled with the fundamental impetus from the economic recovery of the euro area in 2026, we maintain an optimistic stance on the overall performance of European equity markets this year. It is important to emphasize that given the fact that this round of economic recovery in the euro area is a moderate recovery rather than a strong rebound, the gains of European equity markets are expected to underperform those of U.S. equity markets over the next 12 months.

Macroeconomy

The euro area economy staged a moderate recovery in 2025, yet its endogenous growth momentum remained somewhat inadequate. In the first three quarters of 2025, the euro area’s economic growth rate exceeded market expectations on a phased basis; however, upon entering November, the Manufacturing Purchasing Managers' Index (PMI) fell below the threshold. Although the Services PMI still stayed in the expansionary territory, it had declined for consecutive months to 52.6, reflecting the lingering weakness in sectoral prosperity. On the other hand, in terms of confidence indicators, the euro area Economic Sentiment Indicator, Services Confidence Indicator, Construction Confidence Indicator and Consumer Confidence Indicator all rebounded to varying degrees in November, with only the Industrial Confidence Indicator edging down slightly. Meanwhile, the OECD Leading Indicators for both Germany and France also showed signs of recovery. Based on a comprehensive assessment of the overall operational characteristics of the EU economy in 2025, the euro area economy is highly likely to sustain the pattern of weak recovery in 2026.

The core driving variables for European economic growth in 2026 will focus on two dimensions: first, the intensity of fiscal expenditure expansion by governments within the region; second, the actual transmission effect following the implementation of tariff policies, as well as the improvement of exogenous conditions brought about by the evolution of the geopolitical landscape. On the fiscal policy front, the intensified fiscal expansion in Germany is expected to serve as a key engine driving the economic growth of the euro area. According to the estimates released by the European Commission, the overall budget deficit ratio of the euro area is projected to rise to 3.3% of GDP in 2026, an increase of 0.1 percentage points from the previous year. It is noteworthy that the scale of fiscal expansion in Germany is sufficient to offset the drag caused by the fiscal consolidation measures implemented by other major member states. Looking back at the policy process, the German Federal Ministry of Finance announced on July 30 of the previous year that the Federal Cabinet had officially approved the fiscal budget for 2026. The total expenditure under this budget exceeded €500 billion, representing a year-on-year increase of 3.5%. Among this figure, public investment reached a new historical high for the second consecutive year since 2025, with funds to be prioritized for core areas including transportation infrastructure construction, affordable housing supply, digital economy upgrading and national defense security. In terms of national defense-related spending, the combined total of defense budgets and special funds of major countries registered a year-on-year increase of approximately 30%, reaching €108 billion, of which €11.5 billion will be earmarked for aid projects in Ukraine. However, apart from Germany, other major euro area economies such as France will continue to adhere to the policy tone of fiscal consolidation.

The implementation and entry into force of the U.S.-EU trade agreement will effectively mitigate uncertainties in bilateral trade. In the area of reciprocal tariffs, the U.S. imposes a 15% reciprocal tariff on EU goods imported into the country, while granting the EU tariff exemption privileges under the most-favored-nation (MFN) rate for certain goods. Under the framework of allied cooperation, the tariff rates applicable to EU goods exported to the U.S. are generally more favorable than those imposed on goods from other economies. Provided that the subsequent policy environment remains stable, the export trade of the euro area is expected to show a trend of moderate recovery in 2026.

Facilitated and promoted by U.S. President Trump, multiple rounds of consultations have been launched among the U.S., Russia, Ukraine and the EU. Despite lingering divergences over core interests including territorial delimitation and Ukraine’s security guarantees, looking ahead to 2026, the peace process of the Russia-Ukraine issue is expected to keep advancing and moving toward a resolution as all parties further promote negotiations. Looking back on previous progress, it was reported that the key drafting work of the initial version of the 20-point Peace Plan had been completed following the meeting between Ukraine and the United States held in Miami in late December last year. For Europe, the easing of geopolitical disruptions, coupled with the consequent relaxation of Germany’s fiscal constraints and the resolution of energy supply issues, will emerge as a core positive catalyst for the region’s economic recovery in 2026. From the perspective of policy adjustment orientation, redirecting the sustained fiscal expenditures originally earmarked for the battlefield in Ukraine to domestic outlays on people's livelihood security, infrastructure investment and national defense development constitutes a realistic path for Europe to shake off its current economic predicament.

In light of the aforementioned three positive factors, major international institutions have recently revised up their outlook for the euro area economy moderately, following their relatively pessimistic projections released in the middle of last year. Specifically, the International Monetary Fund (IMF) forecasts that the euro area economy will grow by 1.2% in 2026, while both the Organisation for Economic Co-operation and Development (OECD) and the European Commission have set their projections at 1.3%. Overall, the fiscal expansion measures spearheaded by Germany will inject critical impetus into economic growth. Household consumption and corporate investment expectations are showing marginal improvement, tariff-related uncertainties in the trade sector are likely to be further mitigated, and there remains room for easing in core geopolitical pressures. Based on this, we judge that the euro area economy will sustain its ongoing moderate recovery trajectory in 2026, with its GDP growth rate highly likely to fall within the range of 1.2%–1.3%. It should be supplemented that if the actual boosting effects of the aforementioned positive factors exceed current market expectations, there exists the possibility that the GDP growth rate could edge up to 1.5%.

Monetary Policy of the European Central Bank

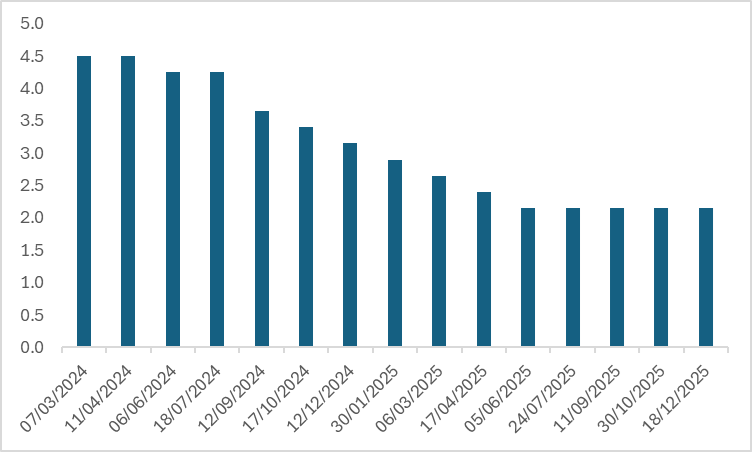

After the European Central Bank (ECB) implemented a 25-basis-point interest rate cut in June 2025, it kept the existing policy rate unchanged and refrained from further adjustments in the three subsequent monetary policy meetings. According to the information disclosed in the ECB’s latest monetary policy meeting minutes, the Governing Council members generally maintained a policy stance of “not rushing to launch a new round of interest rate cuts”, believing that the current policy rate of 2.15% is within a reasonable range that balances the goals of economic growth and inflation control. A number of officials have clearly stated that it is still too early to resume interest rate cuts at this stage, and it is necessary to continuously monitor the evolution of economic data and inflation trends.

Figure: ECB Policy Rate (%)

Source: Refinitiv, TradingKey

Specifically, inflation in the euro area has gradually moved closer to the policy target range, and is projected to continue on a moderate downward trajectory in 2026. Meanwhile, the spillover effects of U.S. tariff policies on the euro area are gradually abating, laying a foundation for the region’s modest economic expansion in 2026. At present, the transmission effect of the wage-inflation spiral has weakened markedly, and the current policy rate corridor is able to achieve a neutral regulatory effect of “neither restraining economic growth nor fuelling inflationary pressures”. Nevertheless, the trajectory of monetary policy is still subject to two-way uncertainties. On the one hand, if economic growth experiences an unexpected slowdown and core inflation remains persistently below the 2% policy target, the European Central Bank (ECB) may seize the opportunity to restart an interest rate cut cycle, with an expected 25-basis-point adjustment per move. On the other hand, if energy prices rebound due to disruptions from geopolitical conflicts or if core inflation is pushed up by stickier-than-expected services inflation, the ECB will not rule out the possibility of reopening the interest rate hike channel, though the probability of such scenarios occurring is relatively low.

The European Central Bank (ECB) has made a clear statement that it will no longer reinvest the principal payments from maturing securities under the Asset Purchase Programme (APP) and the Pandemic Emergency Purchase Programme (PEPP). The two bond-buying portfolios will be reduced steadily at a measurable and predictable pace. This measure marks a further transition of the ECB from the quantitative easing (QE) policy framework to a regular liquidity management model. In advancing the scaling-back process, the ECB will adhere to the core principle of “avoiding disorderly market fluctuations”, and actively guide market expectations through a “transparent reduction pace”. Meanwhile, the ECB will retain the authority to activate the Transmission Protection Instrument (TPI), so as to safeguard the consistency of monetary policy transmission across euro area countries and prevent the emergence and spread of financial fragmentation risks within the region.

Outlook for European Equity Markets

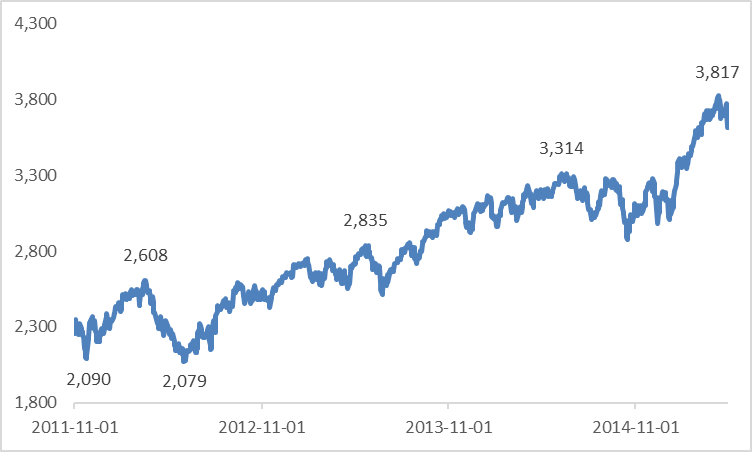

The monetary policy of the European Central Bank (ECB) exerts a decisive impact on the performance of European equity markets. Based on historical experience, the previous low-interest-rate cycle commenced in November 2011 (the early stage of the euro area debt crisis), after which European equity markets maintained a strong upward trend for several years. The core driving factor behind this trend was that the environment of low financing costs significantly boosted the equity allocation demand of the private sector and attracted sustained inflows of overseas capital. Although the market expects the ECB to keep the current interest rate unchanged for a relatively long period, the policy rate of 2.15% still stays at a historically low level. The accommodative liquidity environment will provide robust support for European equity markets, and coupled with the fundamental backing from the euro area's economic recovery in 2026, we maintain an optimistic view on the overall performance of European equity markets this year. It should be noted that given that this round of economic recovery in the euro area is a moderate recovery rather than a strong rebound, the gains of European equity markets are expected to underperform those of U.S. equity markets over the next 12 months.

Figure: Performance of the Euro Stoxx 50 Index in a Low-Interest-Rate Environment Since Late 2011

Source: Refinitiv, TradingKey

At the sector level, from a European domestic market perspective, we remain upbeat about the upward trajectory of European defense spending. Nevertheless, the European aerospace and defense sector posted substantial gains in 2025; in the short term, it is necessary to wait for the release of corporate earnings to verify the rationality of current valuations. Benefiting from solid financial fundamentals and the dividends of a credit expansion cycle driven by economic recovery, the banking sector has established a favorable position with compelling allocation value. From the perspective of external catalysts, the technology sector is expected to form a positive linkage with the upward trend of U.S. tech stocks. The raw materials and industrials sectors will be significant beneficiaries of the enormous demand unleashed by Ukraine’s reconstruction process following the conclusion of the Russia-Ukraine agreement. The consumer sector has relatively lagged in overall performance, yet the market has already fully priced in this trend. Going forward, the recovery in sales in the Chinese market and the easing of U.S. tariff policies will serve as potential tailwinds driving the sector’s rebound. Notably, the latest data indicate that signs of recovery have emerged in the luxury goods sub-sector.

Conclusion

Against the dual backdrop of the euro area’s moderate economic recovery and the European Central Bank’s maintenance of its low-interest-rate policy, we hold a positive outlook on the overall performance of European equity markets in 2026. At the sector level, we recommend that investors focus on five core segments: aerospace and defense, banking, technology, raw materials and industrials, and consumer goods.

Recommended Articles