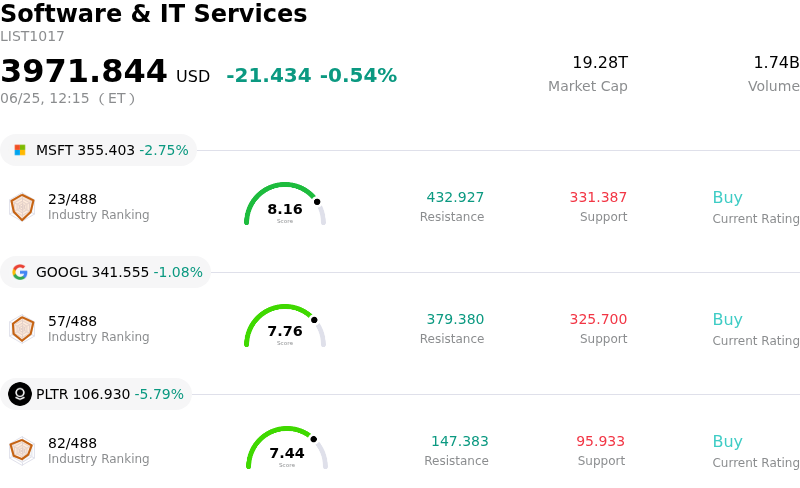

Palantir Technologies Inc Stock (PLTR) Moved Down by 5.79% on Jun 25: Drivers Behind the Movement

Palantir Technologies Inc (PLTR) moved down by 5.79%. The Software & IT Services sector is down by 0.54%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) down 2.60%; Alphabet Inc Class A (GOOGL) down 1.08%; Palantir Technologies Inc (PLTR) down 5.79%.

What is driving Palantir Technologies Inc (PLTR)’s stock price down today?

Palantir Technologies experienced a sharp decline in today's trading session, extending a multi-day slide and reaching its lowest levels in over a year. Despite robust fundamental performance, including exceptional revenue acceleration and strong free cash flow guidance in its most recent earnings reports, the company is facing a perfect storm of aggressive valuation compression, sovereign contract threats in Europe, and shifting competitive dynamics in the artificial intelligence sector.

A primary driver of the downward pressure is a broader re-rating of high-multiple software companies. Investors are rotating capital out of richly valued tech stocks, a trend accelerated by rising interest-rate expectations and recent declines in global semiconductor and hardware markets. With its trailing price-to-earnings ratio sitting comfortably above one hundred times, Palantir has been particularly vulnerable to this rotation. Market participants are increasingly reluctant to support premium valuations when macroeconomic headwinds squeeze growth-oriented assets, leaving the stock highly sensitive to any shift in sentiment.

Compounding these macroeconomic headwinds are significant geopolitical and contract risks in Europe that threaten Palantir's international expansion runway. In France, the domestic intelligence agency announced plans to phase out Palantir's data tools in favor of a domestic sovereign alternative, ChapsVision. Simultaneously, in the United Kingdom, newly renewed political pressure has emerged as parliamentary committees urge the government to exercise a February 2027 break clause to terminate Palantir’s landmark Federated Data Platform contract with the National Health Service. These setbacks have raised structural questions about the long-term viability of Palantir’s public-sector growth outside the United States.

On the domestic front, competitive and operational headwinds are further dampening investor confidence. High-profile short-sellers have intensified scrutiny on the company, pointing to rising competition from frontier AI labs like Anthropic, which is increasingly securing first-time enterprise purchasing decisions. This shifts the enterprise AI procurement model toward flexible, usage-based consumption and away from Palantir’s traditional software deployment structure. Additionally, political gridlock in a polarized election year has raised concerns over US defense pipeline bottlenecks. Investors fear that extended continuing resolutions could freeze federal funding, delaying high-margin programs like Maven and TITAN from pilot phases to scaled production.

Finally, heavy insider liquidations and bearish analyst actions have exacerbated the technical selloff. Significant pre-planned executive stock sales over the last quarter, alongside recent analyst downgrades, have weakened near-term retail and institutional sentiment. Although Palantir continues to generate stellar commercial growth in the US, the market is currently prioritizing immediate valuation risks and geopolitical headwinds over long-term AI-driven operational success.

Technical Analysis of Palantir Technologies Inc (PLTR)

Technically, Palantir Technologies Inc (PLTR) shows a MACD (12,26,9) value of -4.686, indicating a sell signal. The RSI at 30.805 suggests neutral condition and the Williams %R at 96.336 suggests oversold condition. Please monitor closely.

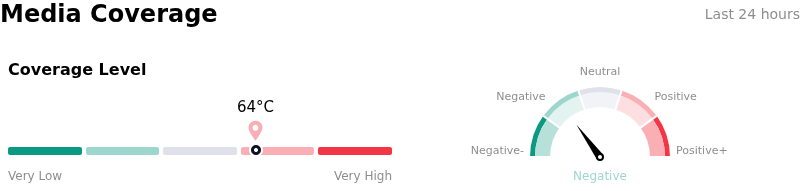

Media Coverage of Palantir Technologies Inc (PLTR)

In terms of media coverage, Palantir Technologies Inc (PLTR) shows a coverage score of 64, indicating a high level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Palantir Technologies Inc (PLTR)

Palantir Technologies Inc (PLTR) is in the Software & IT Services industry. Its latest annual revenue is $4.48B, ranking 72 in the industry. The net profit is $1.63B, ranking 31 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $185.93, a high of $255.00, and a low of $70.00.

More details about Palantir Technologies Inc (PLTR)

Company Specific Risks:

- Loss of Sovereign Government Contracts (France): Reports in the last 48 hours highlight that France's domestic intelligence agency (DGSI) is actively transitioning away from Palantir’s platforms to local competitor ChapsVision. This move to eliminate foreign strategic dependencies poses a direct threat to Palantir’s international government-sector revenue expansion.

- Procurement Obstacles and NHS Contract Scrutiny (UK): London Mayor Sadiq Khan blocked a planned £50 million intelligence automation deal between Palantir and the Metropolitan Police due to a "clear and serious breach" of procurement rules, forcing the project into a competitive 12-month pilot process. Concurrently, UK health officials are facing intense political pressure to execute a February 2027 break clause to terminate Palantir's £330 million NHS contract due to slow platform adoption.

- SaaS Multiple Contraction & AI Subscription Risks: Trading at an extreme valuation of over 128x trailing earnings, Palantir has been caught in a broader software sector sell-off (dubbed the "SaaSpocalypse"). Institutional analysts are growing increasingly concerned that emerging AI agents and large language model (LLM) workflows will commoditize traditional software pricing and erode enterprise SaaS subscription models.

- Technical Support Breakdowns and Short Pressure: On June 25, 2026, Palantir fell to a fresh 52-week low of $108, marking its longest consecutive daily losing streak since March 2023. The stock has broken through key long-term support levels, such as its 100-week moving average, fueled by high-profile short positions and intensifying bearish momentum.

Recommended Articles