SanDisk Corporation Stock (SNDK) Moved Up by 5.37% on Jun 8: Key Drivers Unveiled

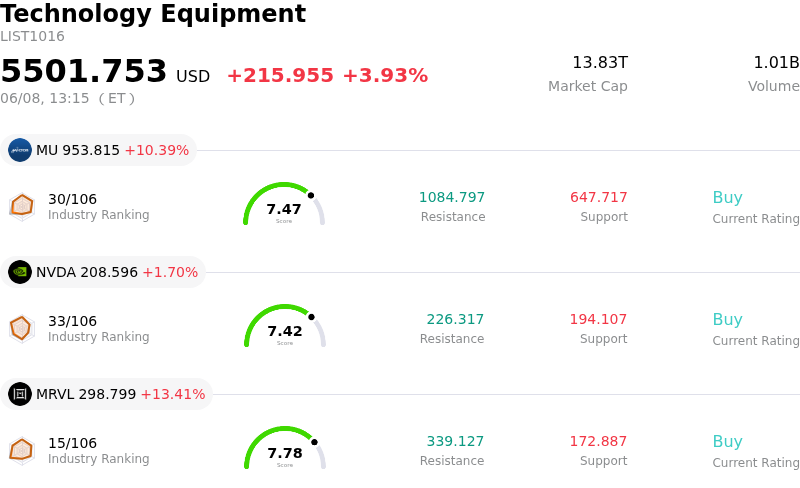

SanDisk Corporation (SNDK) moved up by 5.37%. The Technology Equipment sector is up by 3.93%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 10.29%; NVIDIA Corp (NVDA) up 1.70%; Marvell Technology Inc (MRVL) up 13.35%.

What is driving SanDisk Corporation (SNDK)’s stock price up today?

The intraday price movement for SNDK, which saw an increase, can be attributed primarily to several significant positive developments related to analyst forecasts, strong financial data, and favorable industry dynamics.

A major catalyst for the positive movement was an upgrade in analyst ratings and price targets. Bank of America (BofA) analyst Wamsi Mohan raised the price target for SanDisk (SNDK) to $2,100 from $1,550, maintaining a Buy rating. This substantial increase, representing a considerable percentage boost, signaled strong confidence in the company's future performance. Mizuho also increased its price target for SanDisk to $2,200 from $1,825, retaining an Outperform rating. These upward revisions were driven by expectations of continued robust demand, particularly for NAND flash memory, and constrained supply in the market, with no significant new supply anticipated until 2028 or 2029.

The positive outlook is further bolstered by SanDisk's strong financial position and strategic business models. The company has secured long-term supply agreements with customers, including five deals totaling at least $42 billion in committed revenue and more than $11 billion in guarantees. These agreements include fixed pricing initially, transitioning to variable pricing, which analysts view as a "win-win" for both SanDisk and its customers, ensuring a steady revenue base and future supply. SanDisk's ability to adjust production in response to demand fluctuations, as well as its partnership with Kioxia and growing market share, also contribute to its strong position.

Moreover, the broader semiconductor industry environment is highly favorable for memory chip makers. The demand for NAND memory chips, essential for data centers and artificial intelligence (AI) infrastructure, is experiencing a significant surge. SanDisk, a pure-play NAND flash and enterprise SSD company since its spin-off from Western Digital in February 2025, is a direct beneficiary of this trend. Strong quarterly earnings results, with the company beating expectations on both revenue and EPS, and providing optimistic guidance for the upcoming quarter, underscore the robust demand for its products driven by AI buildouts.

While the stock did experience some volatility and a prior sell-off in the broader semiconductor sector due to macroeconomic jitters and concerns over high valuations, today's positive movement suggests a strong rebound as investors reassess the long-term growth potential fueled by AI demand. The consensus among brokerages remains a "Moderate Buy," reflecting continued optimism despite some insider selling activities and a high P/E ratio compared to historical averages.

Technical Analysis of SanDisk Corporation (SNDK)

Technically, SanDisk Corporation (SNDK) shows a MACD (12,26,9) value of [157.27], indicating a neutral signal. The RSI at 54.89 suggests neutral condition and the Williams %R at -51.69 suggests oversold condition. Please monitor closely.

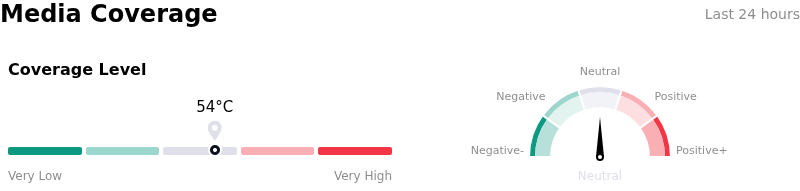

Media Coverage of SanDisk Corporation (SNDK)

In terms of media coverage, SanDisk Corporation (SNDK) shows a coverage score of 54, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of SanDisk Corporation (SNDK)

SanDisk Corporation (SNDK) is in the Technology Equipment industry. Its latest annual revenue is $7.36B, ranking 10 in the industry. The net profit is $-1.64B, ranking 41 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1466.20, a high of $3250.00, and a low of $250.00.

More details about SanDisk Corporation (SNDK)

Company Specific Risks:

- Sandisk's stock experienced a significant intraday decline of 10.38% on June 5, 2026, and an 11.39% decrease over the 24 hours leading up to June 7, 2026, reaching $1,559.32, which is notably below its all-time high of $1,831.50 on June 3, 2026, indicating high short-term volatility and potential for further price corrections.

- The company faces heightened valuation concerns and potential for profit-taking after its stock surged nearly 700% year-to-date in 2026, with analysts like David Sekera questioning if it's a "bubble" and including it in "5 Stocks to Sell in June."

- Insider selling activity, including Chief Legal Officer Bernard Shek's sale of $1,041,600 worth of common stock on June 3, 2026, and other executive sales, may signal caution from management despite the stock's overall positive trajectory.

- Market rumors regarding NVIDIA's Rubin platform potentially reducing memory capacity requirements, which surfaced on June 5, 2026, caused a broad plunge in storage stocks, including an 11.16% fall for SanDisk, suggesting vulnerability to shifts in demand from key AI infrastructure partners.

Recommended Articles