US Pre-Market: Memory Chip Stocks Rebound, IBM Plunges 22%, CPI and Warsh Hearing Arrive Together

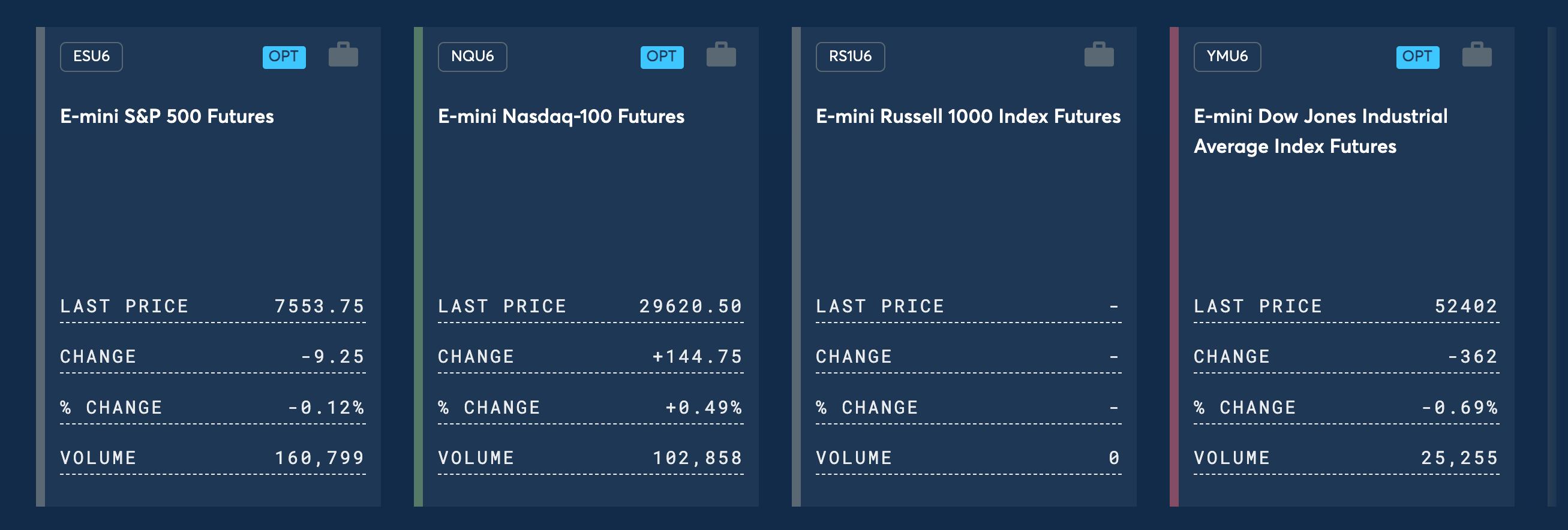

TradingKey - On July 14, Eastern Time, in U.S. premarket trading, the three major stock index futures showed mixed performance. As of press time, Nasdaq 100 Index futures rose 0.49%, S&P 500 Index futures edged down 0.12%, and Dow Jones Industrial Average futures fell 0.69%.

[Source: CME Group]

On the commodities front, international oil prices extended their rally, with WTI crude oil futures rising 1.98% to $79.69 per barrel and Brent crude oil futures advancing 3.3% to $86.11 per barrel. Gold and silver prices edged higher, with spot gold ( XAUUSD) trading around $4,029 per ounce; spot silver ( XAGUSD) trading around $58.02 per ounce.

In the crypto market, as of press time, Bitcoin (BTC) was trading around $62,865, and Ethereum (ETH) was trading around $1,800. The U.S. Dollar Index stood at 101.22.

Market Movers

Memory chip stocks rebounded premarket. As of press time, SK Hynix ( SKHY) rose nearly 7%, SanDisk ( SNDK) rose over 4%, Western Digital ( WDC ), Micron Technology ( MU ), Seagate Technology ( STX) rose over 3%.

Large-cap tech stocks showed mixed performance premarket. Nvidia ( NVDA) rose 1.3%, Tesla ( TSLA) rose 0.42%, SpaceX ( SPCX) rose 0.21%, Microsoft ( MSFT) fell over 3%, Meta ( META) fell 1.23%, Apple ( AAPL) fell 0.87%, Amazon ( AMZN) fell 0.41%, Alphabet Class A ( GOOGL) fell 0.57%.

Market Highlights

Super Inflation Day: CPI Data and Warsh Hearings Arrive Together. At 8:30 AM ET, the US Department of Labor will release June CPI data. The market consensus expects headline CPI for June to decline by 0.1% to 0.2% month-on-month, which, if realized, would mark the first negative monthly growth since 2020; year-on-year, it is expected to ease to 3.8% from 4.2%. Core CPI is projected to rise 0.2% month-on-month, and edge down to 2.8% from 2.9% year-on-year.

Meanwhile, Federal Reserve Chairman Warsh will testify before the House Financial Services Committee for the first time today, before heading to the Senate Banking Committee on Wednesday. Markets expect Warsh to maintain his communication style of declining to provide forward guidance.

IBM plunges over 22% premarket as Q2 revenue falls far short of expectations. IBM ( IBM) released its preliminary second-quarter revenue data today, triggering a sharp market reaction. Revenue was $17.2 billion, up just 1% year-on-year, far below analysts' expectations of $17.86 billion. Software business revenue grew 5%, but infrastructure revenue fell 7%. Diluted EPS was $2.27, down 2% year-on-year; operating EPS was $2.93, up 5% year-on-year.

JPMorgan Chase falls over 2% premarket as Q2 earnings beat expectations across the board. JPMorgan Chase ( JPM) reported Q2 earnings premarket today, with adjusted revenue of $58.02 billion, far exceeding market expectations of $51.39 billion. EPS was $7.70. The investment banking business performed exceptionally well, with equity sales and trading revenue surging 86% to $6.03 billion, far beating expectations of $3.98 billion.

Wells Fargo beats Q2 revenue expectations, falls over 2% premarket. Wells Fargo ( WFC) reported second-quarter 2026 revenue of $22.62 billion, higher than the expected $21.8 billion; net income was $6.4 billion, or $2.00 per share; average total deposits were $1.47 trillion, beating the expected $1.44 trillion.

Rumors of US Listing Resurface; Samsung Electronics Urgently Denies ADR Issuance Review. Market reports today suggested that Samsung Electronics is evaluating the issuance of American Depositary Receipts (ADRs). However, Samsung Electronics quickly issued a statement to deny the claims, stating that "no evaluation of an ADR issuance is being conducted at all," thereby clarifying the market rumors.

Key Events Preview

Eastern Time | Event |

July 14 | Goldman Sachs, Bank of America, and Citigroup Q2 Earnings |

July 14, 8:30 AM | US June CPI Data (Expected +3.8% YoY, Previous +4.2%; -0.1% MoM) |

July 14, 10:00 AM | Fed Chair Warsh Testifies Before House Financial Services Committee |

July 15 | US June PPI Data |

JPMorgan and Wells Fargo both reported better-than-expected earnings, kicking off the bank earnings season on a high note. However, IBM's disastrous earnings led the broader market decline, leaving pre-market sentiment mixed. Tonight's CPI data and Warsh's hearing are the real main events; the key focus is not the improvement in headline CPI, but whether core inflation remains sticky and whether Warsh will use the hearing to deliver clear policy signals. Before both the data and the testimony land, the market is highly likely to remain in a cautious and range-bound pattern.

Recommended Articles