Starbucks: The Premium Coffee Brand With a Pressured Bottom Line

- Q2 FY25 revenue rose 2% to $8.76 billion, but GAAP operating margin shrank 590 basis points to 6.9%.

- U.S. comparable transactions declined 4%, while $116 million in restructuring costs erased most operating income gains.

- Store-level margins in North America fell from 18% to 11.6%, as labor costs rose 13% to $3.43 billion.

- Channel Development revenue dropped 2%, with segment margin falling to 47.3% and equity income down 12.5% YoY.

- Starbucks trades at 29.11x forward P/E, over 100% above the sector median, despite a 50% YoY EPS decline.

TradingKey - Starbucks’ management is projecting confidence in its "Back to Starbucks" turnaround strategy, but the Q2 FY25 results paint a very different picture to investors. On the surface, management’s optimism is rooted in execution momentum, with net revenues increasing 2% year over year to $8.76 billion and the opening of 213 new stores to take its global total to 40,789.

Source: Starbucks IR

Beneath the surface however, there is structural friction in place. Chief among the issues is operating margin, which shrank 590 basis points to 6.9% on a GAAP basis and 460 basis points to 8.2% on a non-GAAP basis. Diluted EPS dropped 50% YoY to $0.34, with the $0.41 non-GAAP EPS representing a 40% decrease. This margin compression is not a one-off fluke; it represents fundamental cost constraints and misalignment between top-line stabilization and bottom-line execution.

Source: Starbucks IR

The key tension in this case is strategic ambition vs. operating reality. Management cites resilient transaction comps in a difficult macro environment, yet U.S. comparable transactions declined 4%, and the 3% ticket growth was driven more by reduced discounting than upselling.

This optimism is further called into question by $116 million in restructuring expenses that erased most operating income gains and helped corporate losses rise 11.7% quarter over quarter.

In essence, Starbucks is investing to shore up the core business and is incurring huge internal disruption expenses in the process, a situation that by its very nature constrains near-term leverage.

Long-term reinvention is the strategic story, but near-term profits betray execution risk. Shareholders are being asked to believe in a vision that has yet to show it can improve margins. This disconnect between confident messaging and pressured comps is central to assessing whether Starbucks can create sustainable value amid increased labor costs, erratic comp trends, and a structurally weaker cost base.

The Brewing Inefficiency of Transaction Decline and Labour Accumulation

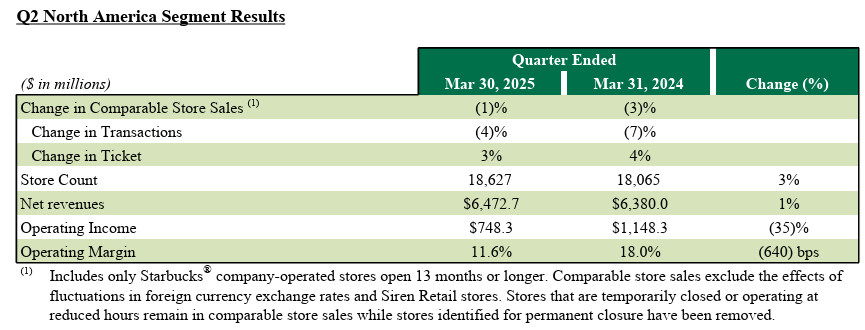

The operating pressure is most acute in North America, which continues to account for almost 75% of Starbucks' operating income. In this region, revenue grew just 1%, held back by a 1% comp sales slowdown and a 4% decline in comparable transactions.

Store operating costs increased 13% YoY to $3.43 billion, causing store-level margins to fall from 18% to 11.6%. Store-level cost intensity rose to 58.5% of company-owned store revenue, up a whopping 540 basis points. This shows a key margin headwind: fixed labor and lease costs are deleveraging just as customer visits decline.

Source: Starbucks IR

Labor cost inflation was largely self-inflicted via the "Back to Starbucks" replatforming, which added higher wage commitments and increased training to improve partner experience. Such investments are necessary to combat unionization pressures and maintain service levels, but they front-load costs without immediate revenue lift. The Q2 restructuring charge, which involves severance from the phase-out of 1,100 support positions, shows the cost alignment has only just begun.

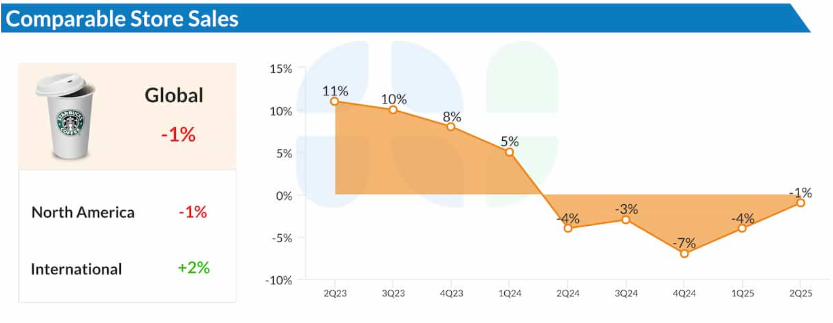

The same is seen in international markets too, where the 2% comp sales growth concealed erosion in margins. While store count expanded 6% YoY and Chinese transactions improved 4%, average ticket declined by 4%, implying demand elasticity is being tested among emerging markets. Even in China, a 5% YoY growth in revenues was driven purely by volume and not by pricing power, which highlights the risk that traffic growth is being bought at the expense of profitability.

Source: Alpha Street

Across the board, Starbucks’ pivot to restoring customer and partner experience is causing a timing mismatch between cost absorption and revenue generation. In the absence of accelerating comps, this inefficiency increases the vulnerability of the investment case to delayed operating leverage.

Channel Development Cracks and the Nestlé Alliance Fatigue

What was once a strategic diversification driver is now showing signs of fatigue. Channel Development revenue fell 2% YoY to $409 million, and operating income fell 11% to $193 million. This deterioration stems not from external shocks but from internal weakness in the Nestlé Global Coffee Alliance and North American Coffee Partnership, implying that Starbucks' consumer packaged goods (CPG) monetization strategy is stagnating.

Source: Alpha Street

The segment’s operating margin fell from 51.7% to 47.3%, indicating growing costs to maintain distribution without volume growth or pricing power. Management is attributing it largely to increased input costs, yet another likely reason is strategic over-reliance on value-alliances that do not offer margin-laden growth anymore. Notably, equity income from Channel Development investments declined 12.5% YoY, further reinforcing the idea that partnership income is deteriorating.

As Nestlé’s royalty amortization (~$5.9 billion remaining) continues to run off as deferred revenue, the absence of visible CPG traction is becoming more concerning. What’s worse is that the high-margin contribution of this segment is disproportionately important for overall profitability, particularly when retail margins are being compressed.

The long-term consequence? Starbucks may need to reconsider its third-party dependency and eventually reintegrate parts of the CPG supply chain to regain margin control. In the meantime, the category’s contribution is structurally diluting.

Discrepancy in Valuation: A Premium Multiple over Slowing Fundamentals

Even with increasing pressure on fundamentals, Starbucks shares trade at valuation multiples that continue to be high based on both its industry and own five-year history. Its forward P/E ratio of 29x is more than twice the sector median of 14x.

Likewise, Its trailing non-GAAP P/E of 27x reflects a 100% premium over the sector median of 13.51. While that is below its own 5Y average of 29.59, the compression is moderate with a 50% YoY detractor in GAAP EPS and declining margin quality. Forward PEG is 3.48 compared to a 1.37 sector median and indicates that growth expectations down the road are overbought compared to expanding earnings.

Other metrics also hint at the same dislocation. Starbucks trades at 3.24x EV/Sales (FWD) and 3.14x EV/Sales (TTM), compared to industry medians of 1.18x and 1.11x. These reflect premiums of 174% and 183% respectively. Historically, valuations were tilted towards the premium side because of network scale and brand strength. Although Starbucks is trading 22–28% below its own five-year average multiples, the market has only partially priced in margin risk.

Its 18.34x EV/EBITDA (FWD) sits uncomfortably alongside 460 basis points of margin compression and is more than twice the sector average of 9.12. Even the improved longer-dated EV/EBIT of 24.55 and forward EV/EBIT of 24.73 suggest peak-level valuations despite deteriorating unit economics.

Price-to-sales ratios remain wide at 2.63x (TTM) and 2.56x (FWD), now trading 228–232% above sector peers while still ~25% below Starbucks’ own historical norms. This puts the stock in a valuation “twilight zone”: too expensive for value investors and too weak on growth to attract momentum capital.

If margins stabilize in FY26 and EPS growth rebounds substantially, these multiples could hold. But if operational inefficiencies continue and comps remain under pressure, the risk on the downside is a re-rating of valuation to a more normalized 18–22x forward P/E and 12–14x EV/EBITDA, implying a 20–30% correction from current levels.

Conclusion: The Brew Remains Strong, But the Froth is Waning

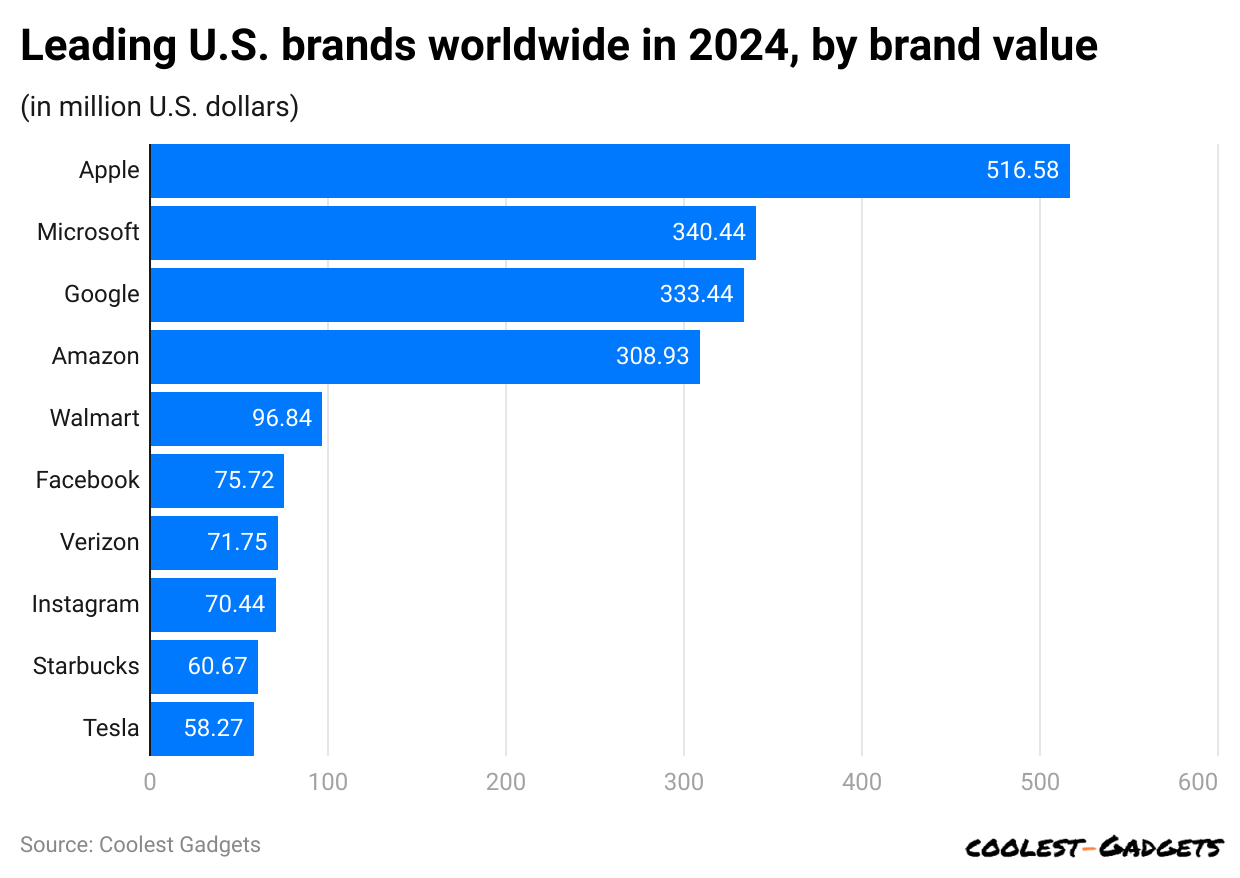

Source: Coolest Gadgets

Conclusion

Starbucks remains a cultural icon with global brand strength and strong economic moats. But Q2 FY25 results revealed a business model under operational stress. While the long-term "Back to Starbucks" strategy may eventually re-energize performance, near-term margin pressure and soft transaction trends suggest the turnaround will be longer, costlier, and riskier than many expect. Investors need to be careful since premium valuation currently assumes a smooth script that financials may not yet support.

Recommended Articles