Qualcomm’s AI Renaissance: Why Wall Street May Be Undervaluing the Edge Titan

- Gold Price Forecast: Gold Poised to Break $4,200 as Oil Price Slump Eases Inflation Fears

- Gold declines despite easing concerns over inflation, interest rate hikes

- Fed Decision Eve: 104 Economists Expect No Change; Why Is Citadel Securities Betting on a Surprise Hike?

- Gold Price Forecast: Can Gold Hold $4,020 as Fed Rate Hike Expectations Rise?

- Middle East War updates: US-Iran pause strikes as Trump weighs up diplomatic options

- WTI Oil flirts with the $80 level amid speculation about US-Iran peace talks

Qualcomm (QCOM) is usually considered in the narrow context of mobile modems and royalties, not accounting for its increasing importance in the new AI paradigm. However, its mostrecent Q2 FY2025 earningsindicate that the firm is no longer merely hitching along with the mobile device wave.

However, Qualcomm is fast establishing itself at the intersection of on-device AI, edge computing, and new-gen connectivity. While the market is still bestowing inflated multiples on cloud-based AI chip providers, Qualcomm has been quietly developing a business model in which the AI stack is not merely centralized in the cloud but integrated into billions of endpoints, smartphones, vehicles, PCs, and IoT systems.

This underappreciated advantage, based on decades of system-on-chip integration and signal processing know-how, may be structurally more resilient and lucrative. The market has yet to adequately value the monetization upside from on-device generative AI and edge-native AI solutions, where Qualcomm is ahead with NPUs integrated into Snapdragon platforms. While others pursue hyperscale inference and training workloads in the cloud, Qualcomm is addressing the other 80% of the AI iceberg: edge inference.

This story, AI outside of the cloud, is infrequently valued in existing estimates, yet already drives ASP growth and multi-segment revenue expansion. With stock trading in the neighborhood of 12x forward non-GAAP earnings and non-handset segments advancing by 38% year on year, Qualcomm’s edge-native AI approach may present one of the most asymmetric risk-reward profiles in semiconductors today.

Source: Q2-FY25 Deck

The Power Under the Hood: Qualcomm’s Business Model Redefined

Essentially, Qualcomm's business has two segments at its core: QCT (chipsets) and QTL (licensing). Historically, the company was tied to handsets, but that model is being reconfigured. QCT generated Q2 revenue of $9.47 billion, up 18% from last year, with handsets remaining predominant at $6.93 billion but supported by strong growth in auto and IoT. This is indicative of Qualcomm's ability to place its Snapdragon and modem-RF platforms in markets outside of smartphones, particularly vehicles and industrial edge installations.

Most importantly, Qualcomm's advantage is in integration. The firm doesn't supply standalone chips but vertically integrated platforms that integrate modem-to-antenna solutions, RF front ends, application processors, AI engines, and software. This provides it with a defensible position where power efficiency, size, and performance co-exist in products, which is where the cloud AI players are not strong.

The most impactful evolution is Qualcomm’s AI architecture. Most recent Snapdragon SoCs integrate neural processing units that support running tiny language models on the device. As AI penetrates mainstream mobile and embedded use cases, Qualcomm’s design wins keep spiking. On-device AI is no longer hypothetical—it’s monetized, particularly in new product segments such as foldable phones, wearables, and car infotainment.

In parallel, Qualcomm's software platform, fueled by increasing developer support and optimized AI toolkits, is driving platform stickiness. Developers can deploy quantized AI models on edge devices directly, without the need to constantly rely on cloud connectivity. This virtuous flywheel enhances Qualcomm's relevance above and beyond hardware, bringing the company closer to platform economics.

Source: Q2-FY25 Deck

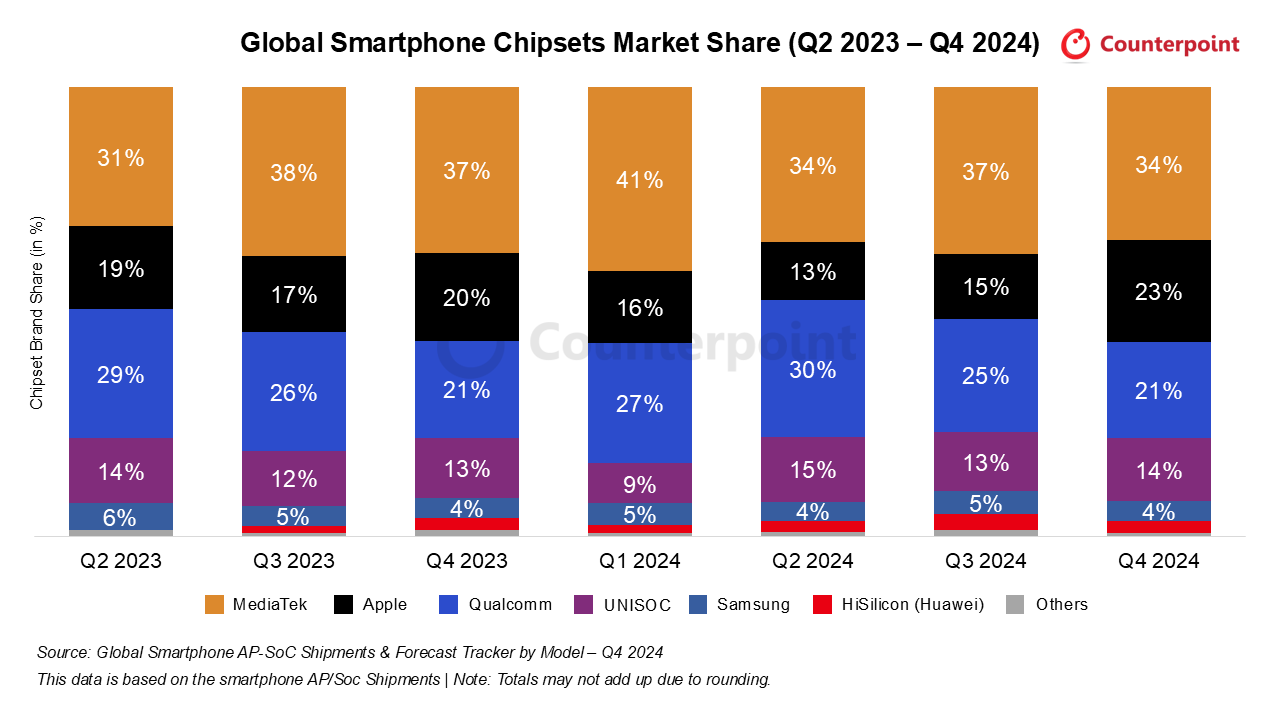

Surviving the Gauntlet: Competitive Pressure and Pricing Dynamics

Qualcomm is in one of the most competitive segments in semiconductors, with average selling prices and gross margins perpetually in decline. Within the premium smartphones segment, the firm has long-standing competition in the form of MediaTek, especially in China, where market share oscillates erratically. That said, Qualcomm still has the lead in premium products across the world due to strategic wins like an increased share of Samsung's flagship shipments.

This level of entrenchment is crucial. Apple is, as of now, replacing Qualcomm modems with in-house silicon while Qualcomm continues to retain high-end OEM stickiness in other areas. Nevertheless, the danger of customer vertical integration is still sharp. Chinese OEMs are increasingly incentivized to create proprietary chipsets under local policy support, and this could undermine Qualcomm's share in subsequent Android cycles.

Mitigating this danger is Qualcomm’s diversification. While competitors with slimmer product lines are vulnerable to exposures from one area, Qualcomm’s expansion into automotive and IoT has created new strategic moats. In auto, Snapdragon Digital Chassis now serves as the foundation of several dozen OEM relationships that allow Qualcomm to embed deeply in electric and connected vehicle architecture. In IoT, Qualcomm’s capacity to deploy full-stack AI at the edge separates it from the competition still tied to cloud-based models of deployment.

Consequently, Qualcomm's price competition is increasingly insulated by the modularity of its products and the layered character of its system. In addition, value capture is not merely by ASPs anymore but by integration, software tools, and system design wins that reap greater margins in the longer term.

Source: Counterpoint Research

In The Microscope: Financial Quality And Scaling Efficiency

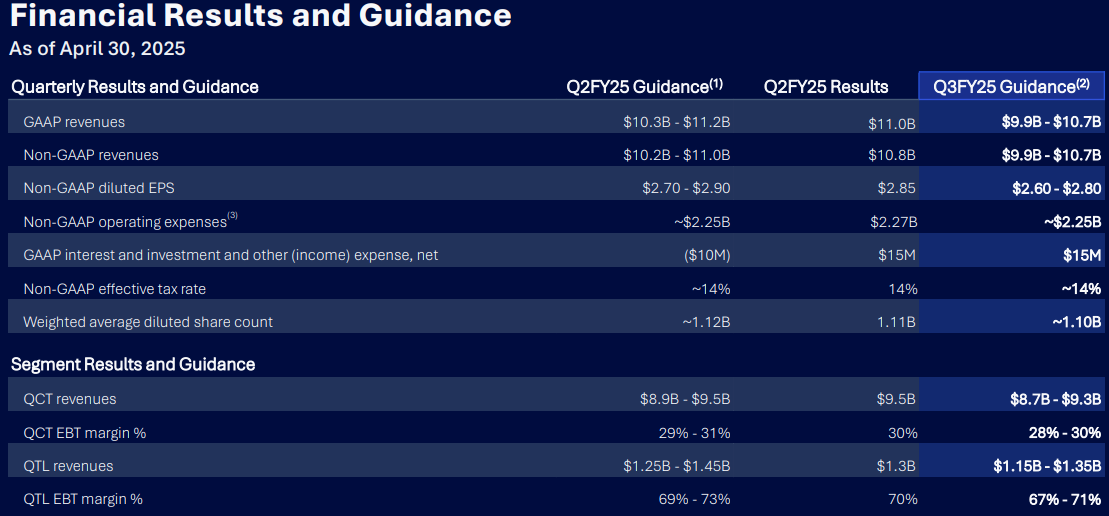

Qualcomm's Q2 FY25 performance was more robust than it seemed. Non-GAAP EPS was up 17% from the previous year to $2.85, and total revenues were up 15% to $10.84 billion. Inside QCT, operating profit exceeded revenue expansion and demonstrated hints of embedded operating leverage. This is all the more appealing considering that fast-growing segments such as auto and IoT are growing quicker than handsets.

The firm is highly capital-efficient. It leverages a fabless model, with low CapEx expenses and heavy investment in scalable programs in areas like on-device AI engines and connectivity. The growing partnership ecosystem behind its edge AI products presages a long-term migration towards higher-margin, software-based business segments, with the possibility of adding layers of recurring revenues on the back of chipset introductions.

Nevertheless, customer concentration is still the primary threat. A significant percentage of the revenue continues to come from several big OEMs, especially in mobile. Qualcomm is beginning to see early success with Snapdragon PCs and auto systems, though these markets are not yet big enough to fully complement a decline from big phone partners. That said, with flagship design wins scaling geographically and across products, the direction is toward less cyclicality.

Operating metrics further support Qualcomm's robust operating profile. The firm's price-to-cash flow ratio is 12x (TTM), compared to the industry median of 17x. Cash flow-based forward valuation (10x) also supports high operating leverage and prudent capital allocation. These metrics, along with better margins in diversified segments, indicate a high-quality earnings stream that is less appreciated during the general AI hype.

Source: Q2-FY25 Deck

The Valuation Gap: Undervaluing the Edge AI Market Leader

Qualcomm's current valuation highlights a structural misalignment between perception and reality. Qualcomm's stock trades at a non-GAAP (TTM) P/E of 12x, almost 40% lower than the sector median of 20x. Its non-GAAP forward P/E is also compressed equally, with a 42% discount. These multiples also are approximately 30–35% below their own 5-year historical average. On GAAP measures, Qualcomm is trading at only 14x trailing and 14x forward, or a ~46% discount to the sector median of 26x.

This is not due to deteriorating growth. Actually, the firm's PEG multiple on GAAP earnings is only 0.5x, substantially less than the sector average of 0.8x, suggesting that it's still not valued enough even considering growth. The only exception is the PEG Non-GAAP value, which is at 1.6x above peer-comparable figures, possibly due to short-run EPS volatility as opposed to a sustained trend.

On EV-based metrics, Qualcomm is still favorably valued. EV/EBITDA (TTM) is only 11x compared with the sector median of 16x, and forward EV/EBITDA is 9x, which signals an even deeper discount. Both these values indicate that Qualcomm's enterprise value highly underestimates its underlying earnings power. The EV/EBIT metric is no different: it’s priced about 41% lower compared with the peer group with a forward value of 10x.

Other metrics portray underlying strength. Qualcomm's dividend yield of 2.5% is significantly greater than the industry median of 1.7% and is underpinned by steady free cash flow. While its book value multiple of 5x is pricey-looking, it is justified by capital-light expansion and the efficiency of R&D. Meanwhile, its forward price/sales multiple of 3x is still in the middle, particularly after accounting for revenue quality and non-handset drivers of growth.

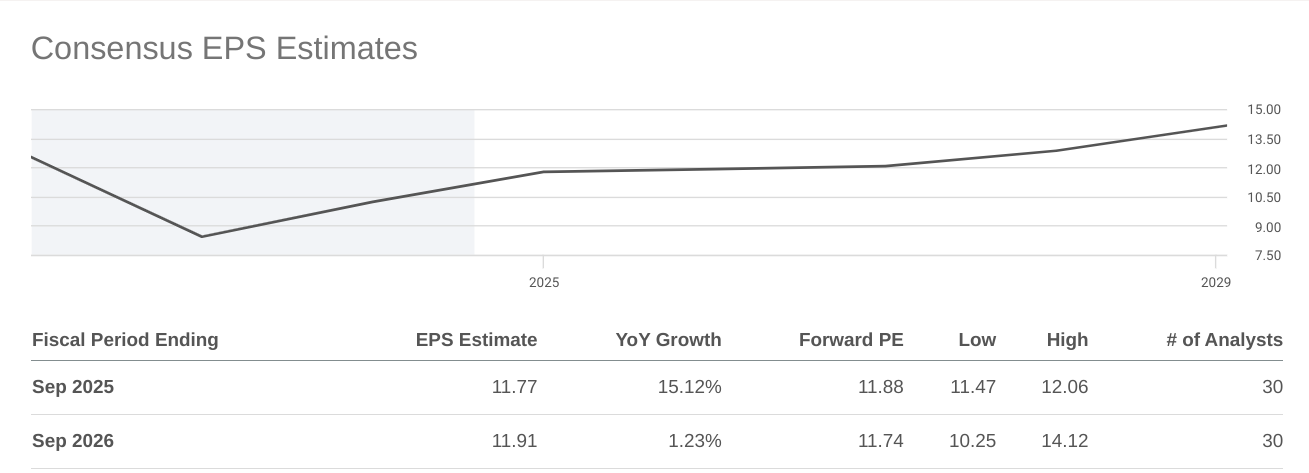

Using the appropriate earnings multiple of 17x–18x forward Non-GAAP EPS and assuming FY25 EPS of $11.20–$11.40, Qualcomm’s fair value is in the range of $190–$205. This represents a 35%–45% upside from its current share price of about $140. This target has not accounted for any premium associated with its AI edge leadership or optionality in software monetization and thereby has further upside on offer.

Source: SeekingAlpha

Blind Spots and Tectonic Risks

Despite its potency, Qualcomm has crucial risks that need to be addressed. Apple’s transitioning to in-house modem chips poses a long-term multi-billion-dollar revenue loss threat. Chinese OEMs, faced with geopolitical and economic pressures, may also move towards local semiconductor solutions more aggressively, thereby endangering Qualcomm’s revenue stream in handsets.

Another structural threat is the risk of scrutiny by regulators. Qualcomm’s licensing model is still in focus in worldwide markets, particularly in those that question its approach to patents. While litigation threats have lessened in the last few years, the underlying exposure remains.

Last but not least, on-device AI is incredibly promising but still is in its early stages in terms of monetization. Were developer adoption, usage-case proliferation, or OEM driving lag, Qualcomm's edge AI thesis may be slower to happen than investors expect, pushing the multiple expansion thesis back.

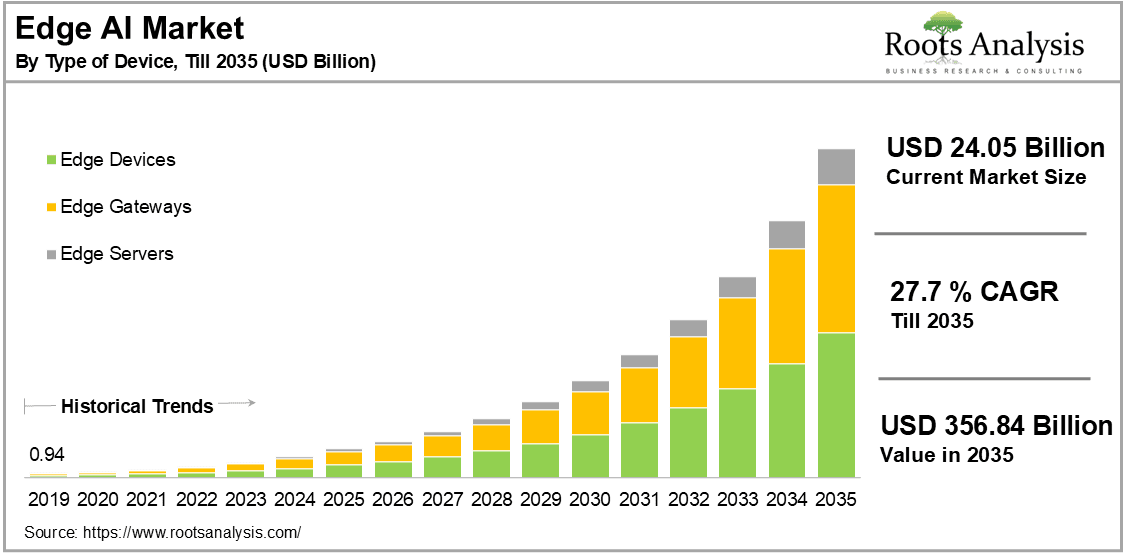

Source:Roots Analysis

Conclusion

Qualcomm is not merely a wireless IP licensor or phone chip vendor anymore. It is an edge AI infrastructure player in plain sight. Those willing to look behind the EPS headline will be able to still discover asymmetric value in a company that is reshaping where and how AI gets applied.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.