Engineering the Future: TSMC’s Strategic Centrality in the AI Era

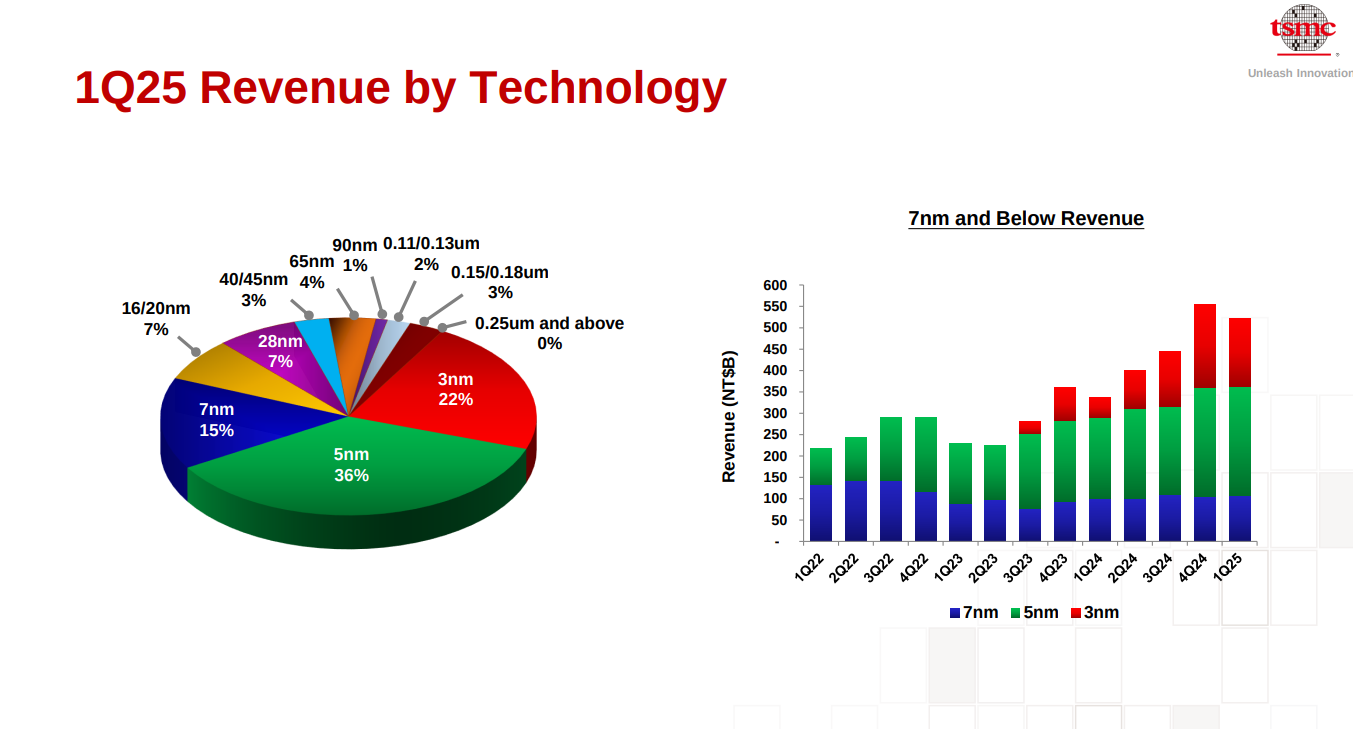

- In Q1 2025, 73% of TSMC’s revenue came from 7nm and below technologies, with 58% of wafer revenue from 3nm and 5nm nodes, driving leadership in AI and HPC sectors.

- Despite a 3.4% QoQ revenue dip due to seasonality, TSMC posted 41.6% YoY revenue growth and 60.3% net income growth, with gross margins stable near 59%.

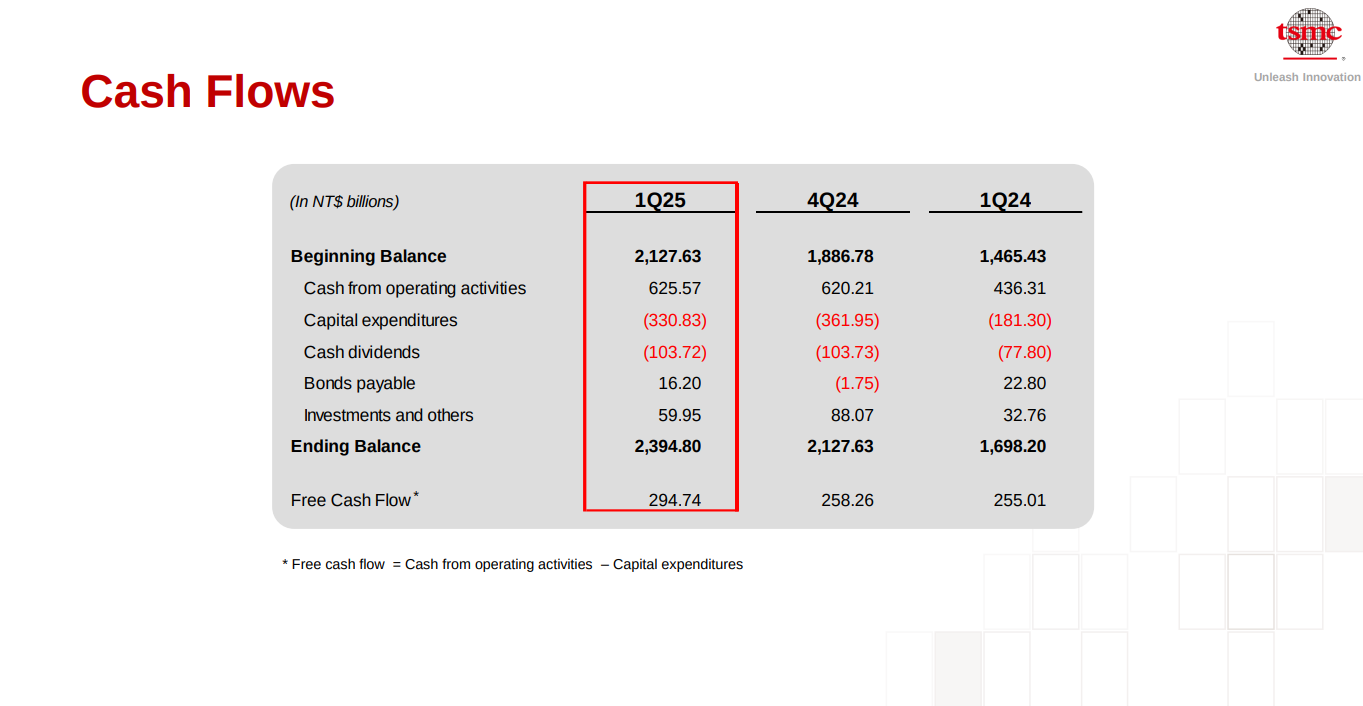

- Q1 2025 free cash flow reached NT$294.7B (~$9B), up 14% sequentially, even with a 5.1% CapEx rise and only 5.1% QoQ increase in net PP&E, highlighting scale leverage.

- Trading at ~27.6x forward P/E, fair value estimates based on 32–35x EPS multiple suggest an ADR target of $290–$317, implying 14–25% upside from current levels.

TradingKey - In a high-multiple AI news-driven market beset by cyclic concerns regarding semiconductors, Taiwan Semiconductor Manufacturing Company (TSMC) is becoming a less volatile but equally mission-critical AI infrastructure pillar. While Nvidia makes headlines, TSMC powers the compute arms race from below through unprecedented process prowess, 3D packaging, and capacity scale. With 73% of Q1 2025 revenue driven by 7nm and below technologies, and 58% of wafer revenue on the 3nm and 5nm nodes, TSMC architectural leadership is now at the center of generative AI, edge inference, and advanced automotive compute.

This asymmetry exists in the market's chronic tendency to price TSMC as a conventional semiconductor cycle stock, not as a platform-level, pure-play foundry cornering sub-5nm volume. Even as Q1 2025 revenue softened sequentially by a mere 3.4% due to smartphone seasonality, YoY revenue accelerated by 41.6%, while net income rose a whopping 60.3%, testimonial to the structural AI transition under way. With stabilizing gross margin at about 59%, and long-term ROE consistently over 25%, TSMC is no longer a pure play manufacturing partner. It is a decoupling world's sovereign supply chain pivot point.

Source: Q1 Deck

Silicon Sovereignty: A Business Model

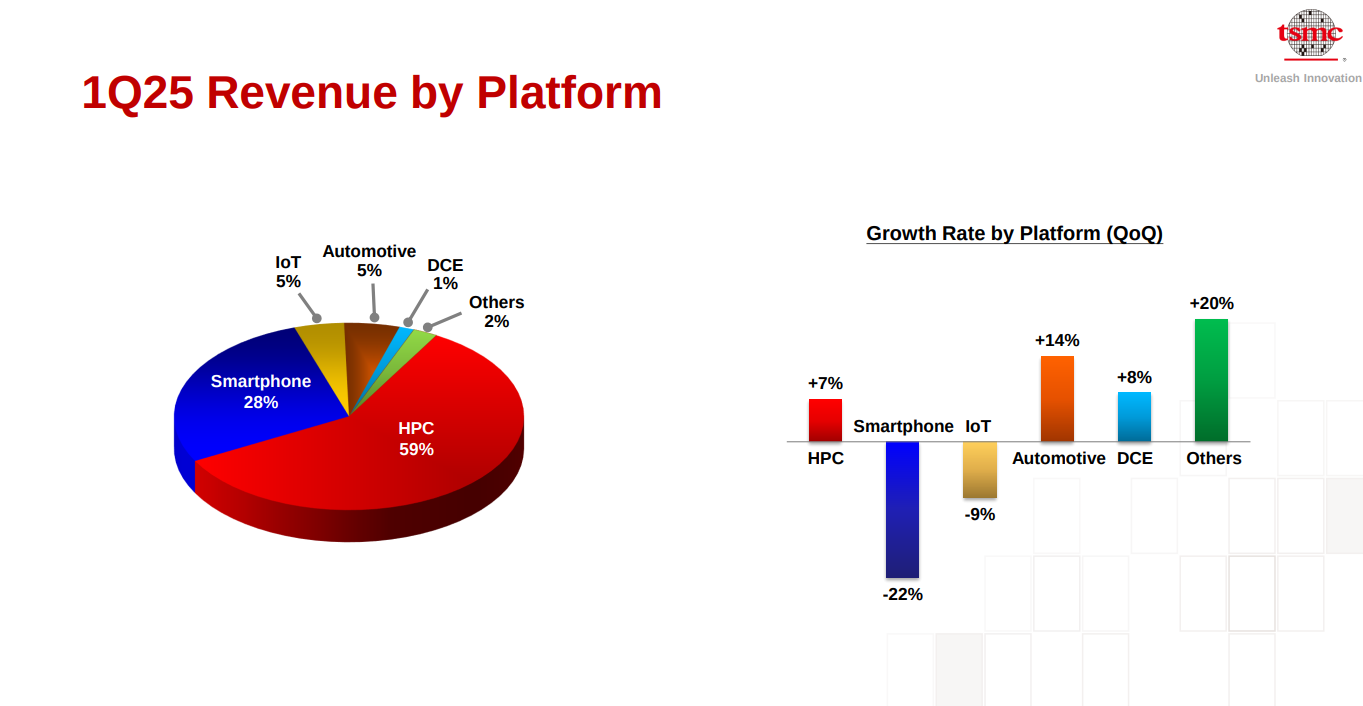

TSMC's business model is strategically designed for deep customer entrenchment and strategic neutrality. In contrast to vertically integrated competitors, TSMC never produces its own chips, precluding channel conflict and solidifying customer trust. In 2024, it manufactured 11,878 variants of chips on 288 process technologies for 522 customers essentially serving as the global compute's outsourced backbone. The revenue breakdown of 59% HPC, 28% smartphone, and the balance across automotive, IoT, and DCE illustrates extensive platform exposure with AI embedded optionality.

What sets TSMC apart, though, is not merely scale but the “3DFabric” strategy: bringing together advanced nodes with high-density silicon interposers, CoWoS, InFO packaging, and SoIC packaging. This allows TSMC to address multi-die and chiplet architectures required by AI accelerators, propelling it beyond a foundry to the world of heterogeneous systems production. The firm's singular capability to deliver logic and packaging within one roof is becoming ever more important, particularly as customers such as Nvidia and AMD require tighter power/performance/area tradeoffs.

TSMC's advanced node leadership in foundries is supplemented by its geographical footprint. Arizona and Kumamoto plants coming online, a freshly started Dresden facility, TSMC is spreading its capacity by aligning with national chip sovereignty plans, becoming a necessity for the U.S., Japan, and Europe alike. Such global alignment are geopolitical moats that protect the company against localization threats, turning industrial policy into business long-term strength.

Source: Q1 Deck

The Foundry Gauntlet: Competition, Integration, and Tariff Risk

In contrast to its position of strength, TSMC is now operating within a highly contested space. Samsung Foundry, technologically aggressive as it is, is behind on yield, as well as on customer satisfaction. Intel Foundry Services (IFS) is spending heavily on becoming relevant, with CHIPS Act subsidies to support it, and is following a U.S.-first capacity strategy to win defense and hyperscaler customers. Nevertheless, there isn't a rival with TSMC's combination of yield maturity, scale, and cost structure at the leading edge.

TSMC's true moat is the yield curve and time-to-volume lead. While Intel is trying out the 2nm gate-all-around (GAA) structures, TSMC's N2 process is already at early customer engagement, with production slated for 2H 2025. Further, with A16, an N2 derivative with backside power delivery tuned to HPC, is targeted for volume ramp in 2026, TSMC's process roadmap is well-tuned to AI system needs.

Civilian tariff threats, on the other hand, are piling up. In Q1 2025, management disclosed that although underlying behavior is stable, policy uncertainty about trade might dent downstream demand. TSMC alone receives 70% of its revenue from North America and 11% from China, so it is exposed to second-order threats from client rebalancing if U.S. limits on Nvidia's H20 and comparable AI chips deepen. While TSMC does not directly make these chips, its reliance on a few hyperscaler customers amplifies end-market sensitivity.

Nonetheless, the strength inherent within TSMC's platform diversification strategy enables partial hedging. Automotive and IoT segments will trail short-term unit growth, yet longer-term silicon content per system continues to increase, especially within electric vehicles and edge AI, and this is cushioning against smartphone cycles, as well as PC weakness.

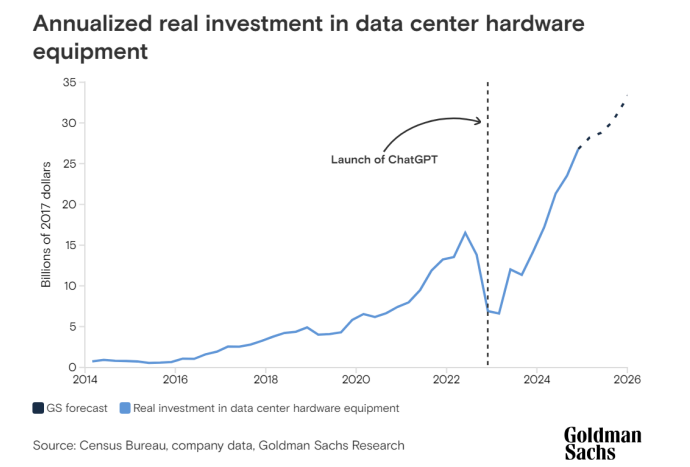

Source: Goldman Sachs

Fabricating financial outperformance: Profits, efficiency, and reinvestment

TSMC Q1 2025 results exhibit a delicate balancing act between margin management and strategic reinvestment. Revenue dropped sequentially by 3.4% to NT$839.3 billion ($25.53B), while maintaining a steady margin of 58.8% due to sustained pricing power at advanced nodes. EPS was at NT$13.94, a rise of 60.4% YoY. Free cash flow at NT$294.7 billion (~$9B) was up by 14% sequentially, notwithstanding earthquake disruptions and a CapEx increase of 5.1%.

The underlying financial driver of these achievements is asset productivity and scale leverage. With net PP&E only increasing by 5.1% QoQ to NT$3.4 trillion, annualized asset productivity is now well above 1.0x. Inventory turnover is healthy at 80 days, while receivable turnover improved at 83 days, testifying to well-disciplined collections against strong capacity utilization.

Crucially, TSMC's margin structure is still superior. Q1 operating margin was at 48.5%, while net margin was at 43.1%, well ahead of foundry competitors. These rates are not the result of underinvestment, TSMC incurred more than US$6 billion on R&D alone in 2024 and continues to devote more than $30 billion a year to CapEx merely to maintain technological edge and packaging lead times. More significantly, long-term ROE is still within the range of 30–35%, even after huge capital intensiveness, which is a sign of exceptional reinvestment effectiveness.

This combination of high margins, careful working capital management, and conservative CapEx makes TSMC's cash flow profile unusually resilient. While Intel incurs burn to catch up and Samsung faces operating volatility, TSMC maintains innovation and shareholder return, distributing NT$14/share worth of dividends in 2024, a YoY increase of 24%.

Source: Q1 Deck

Re-Rating to Come: Valuation Viewpoint and Target Price Scale

TSM occupies a valuation sweet spot between growth and value. Its forward P/E of 17.74 is 11% below its sector median of 19.85, providing relative value in a world where quality names command a premium. PEG ratios paint an even more compelling picture: TSM’s trailing PEG of 0.33 and forward PEG of 0.85 are significantly discounted, 53% and 43% below sector averages, respectively, implying the stock represents better growth for the price. Forward EV/EBITDA of 8.30 and EV/EBIT of 11.73 also signal that investors are paying considerably less for every dollar of earnings versus peers. TSM’s historical premium is deflating, its forward P/E is 21% below its 5-year average, yet this re-rating is a function of macro caution, not a decline in fundamentals.

Nonetheless, there are valuation warning flags that need to be noted. TSM’s forward and trailing sales multiples of 6.15x and 7.36x, respectively, are more than 140% above the sector median, and its 5.03 price-to-book ratio is 65% higher than the sector median, reaffirming that TSM pays a healthy quality premium for its positioning at the cutting edge nodes. Nonetheless, these premiums look warranted by TSM’s size, tech advantage, and sustainable margins.

Overall, Taiwan Semiconductor poses a rare combination of undervalued earnings potential and franchise strength, yet shareholders need to keep an eye on cyclical semiconductor fluctuations and geopolitical risks that may challenge future multiple sustainability.

Additional Risks: Concentration, Trade, and

In spite of its strength, TSMC is exposed to several major risks. Customer concentration is high, Apple, Nvidia, and AMD represent more than 40% of revenue. A slowdown among hyperscaler AI spending or a strategic move to internal chip production (such as Google's TPU or Amazon's Trainium) might pressure volume. Geopolitical threats are ongoing. Although the company is expanding outside of Taiwan, 80%+ of existing capacity is island-focused, thus jeopardised by U.S.-China tensions.

Growing tariffs or export restrictions on high-end chip tooling and IP will also indirectly limit TSMC's innovation rhythm. At last, there is margin saturation risk. Once AI commoditizes and sub-3nm pricing is normalized, TSMC will need to derive incremental value through ecosystem services, packaging, or silicon-vertical integration alliances. The window of opportunity for premium pricing monetization might reduce if differentiated solutions such as A16 or 3DFabric do not get wider traction.

Conclusion:

A Strategic Compounder Hiding in Plain Sight TSMC is underappreciated as the keystone of the global AI stack. While investors pursue AI narrative winners, TSMC possesses a unique mix of technological leadership, geographic leverage, and compounding cash. Its foundry model, packaging integration, and capacity expansion globally place it as the unassuming facilitator of all major AI ecosystems. With a 25% upside potential and limited structural downside, TSMC is worthy of institutional re-rating not as a cyclical tech play, but as a sovereign-scale infrastructure compounder with multi-decade tailwinds.

Recommended Articles