What You Need to Know About Memory Leader SK Hynix’s Violent Stock Price Fluctuations

TradingKey - On July 10, Eastern Time, SK Hynix ( SKHY) ADRs listed on Nasdaq, raising $26.5 billion and setting a new record for a foreign company IPO in the US, with the ADRs closing up 12.76% on their first day.

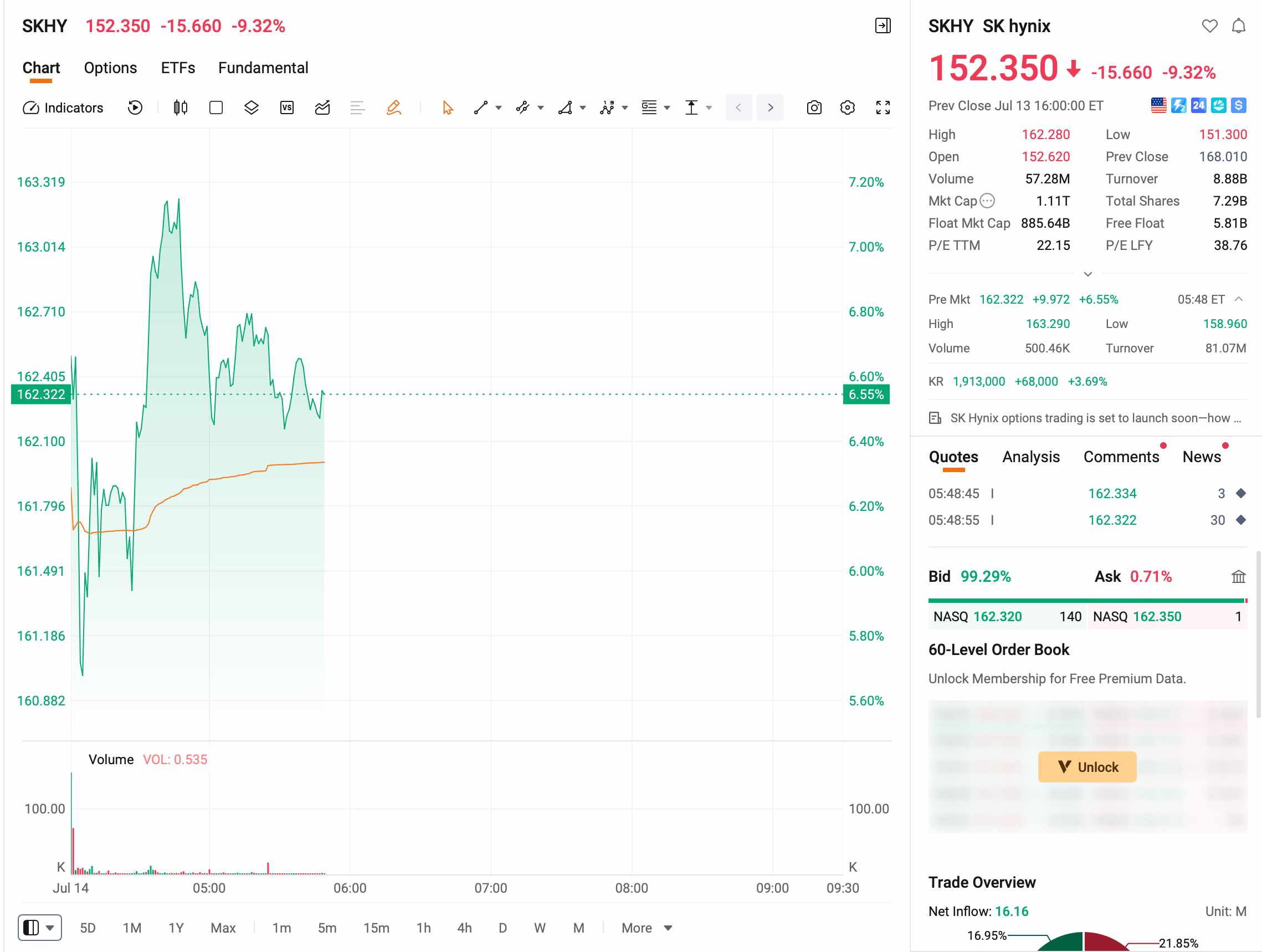

On July 13, the underlying South Korean shares plummeted 15.37%, marking their largest single-day drop since listing and retracing 35% from their June peak. The ADRs plunged nearly 9% in a single day, giving back almost all of their gains. The following day, South Korean shares staged a V-shaped rebound. As of press time, the ADRs were up over 6% in pre-market trading, and the long-short battle over these two days has been brutally fierce.

[Source: Futu]

Why SK Hynix Slumped?

A "below-expectations" report sparked panic

The direct trigger for the plunge points to the earnings preview report released by Korea Investment & Securities (KIS) on that day. KIS forecast SK Hynix's second-quarter operating profit at 60.4 trillion won, a 556% year-on-year increase, but still about 8% below the market consensus of 65 trillion won.

The report explained that because HBM is mostly priced under three- to five-year long-term agreements, a high proportion of shipments actually dragged down the overall average selling price growth. Against the backdrop of SK Hynix's cumulative gains exceeding 200% in this cycle, a single phrase like "below expectations" was enough to trigger panic selling.

The liquidation spiral of leveraged ETFs is the real driver

Goldman Sachs ( GS) report pointed out that the forced liquidation of leveraged ETFs was the core driver behind Monday's plunge. Following sharp declines in these products, issuers were forced to conduct aggressive risk rebalancing, with this selling accounting for 62% of net selling by local institutions.

More than 10 leveraged ETFs tracking Samsung Electronics and SK Hynix that were listed in late May have seen their prices nearly halved. Among them, the KODEX SK Hynix Single Stock Leveraged ETF, the largest in size, has fallen by a cumulative 45% since its listing, down over 60% from its June peak.

Even more staggering is the cost to retail investors. As of Monday, more than 1.2 million leveraged retail investor accounts across the entire South Korean market had hit margin call thresholds, with approximately 320,000 to 360,000 accounts already fully liquidated, wiping out their principal. Some accounts even owe outstanding debts to brokerages.

Next-Day V-Shaped Recovery: SemiAnalysis Bullish, Regulators Step In

On July 14, South Korean stocks extended their panic in early trading, with SK Hynix plunging nearly 9% at one point. The market staged a dramatic reversal in the afternoon, and SK Hynix closed up 3.68%, erasing all of its intraday losses.

The immediate catalyst came from SemiAnalysis, an independent research firm. The firm released a report on that day titled 'Be Greedy When Others Are Fearful,' taking an unequivocally bullish stance. The report expects SK Hynix's second-quarter blended DRAM average selling price to increase by about 45% quarter-on-quarter, significantly higher than KIS's forecast of 28.9%, with operating profit at approximately 55 trillion Korean won, beating market consensus, mainly supported by a quarter-on-quarter surge of about 60% in commodity DRAM pricing. Analysts believe that after this round of correction, SK Hynix 'is currently one of the investment opportunities with the best risk-reward ratio in the semiconductor sector.'

Meanwhile, the South Korean government announced that it would hold an emergency meeting on Thursday to study countermeasures regarding the impact of single-stock leveraged ETFs on the stock market. This marks the first time the issue has entered discussions at the highest-level economic coordination platform.

On the same day, at the annual SoftBank World conference held in Tokyo, SoftBank CEO Masayoshi Son predicted that by 2040, the artificial intelligence sector would require an annual investment of $5 trillion, and flatly dismissed market concerns about an AI bubble, which significantly bolstered sentiment, synergistically supporting the afternoon rebound of Asia-Pacific chip stocks.

Have SK Hynix’s Fundamentals Changed?

Despite the massive stock price volatility, SK Hynix's fundamental narrative did not experience a material reversal in mid-July:

Fundamental Dimension | Current Status |

HBM Capacity | Full-year capacity for 2026 has been completely booked by customers, with some orders scheduled out to 2027 |

Customer Structure | Nvidia ( NVDA ), AMD and other major AI chip makers are core customers, providing strong order visibility |

Technological Barriers | HBM3E 12-layer stacking technology still leads Samsung and Micron Technology ( MU ) |

Pricing Power | Demand exceeds supply, and average selling prices for HBM continue to rise sequentially |

Earnings Outlook | Market consensus forecasts full-year operating profit to grow by over 60% year-on-year in 2026 |

If the tech giants' earnings starting July 22 show a slowdown in AI revenue growth, the market may revise down 2027 HBM demand forecasts, which is the real fundamental risk.

How Wall Street Sees SK Hynix

Optimists dominate. UBS ( UBS) released a report in early July, raising its target price to 3.2 million Korean won and reiterating a "Buy" rating. The bank expects SK Hynix's 2026 operating profit to reach 32.7 trillion Korean won, about 27% above the market consensus, and further rise to 62.3 trillion Korean won in 2027, beating expectations by about 54%. UBS believes that the finalization of long-term supply agreements, mass production of HBM4, and potential share buybacks following an ADR listing will serve as three major catalysts driving a valuation re-rating. Citi ( C) had already raised its target price to 3.1 million Korean won in May, representing an upside potential of about 68% from the stock price at the time.

Although Korea Investment & Securities (KIS) lowered its Q2 earnings forecast, it maintained its target price of 3.8 million Korean won and an "Overweight" rating, stating that the downward revision was merely an adjustment to long-term agreements rather than a deterioration of fundamentals.

The July 29 earnings of Microsoft ( MSFT) and the July 30 earnings of Amazon ( AMZN )—both indirect major customers of Nvidia and SK Hynix—will directly validate the strength of HBM demand through the AI revenue growth rate of their cloud businesses.

Long-Term Logic: HBM Long-Term Contracts Are Reshaping Valuation Systems

The core controversy of this turmoil is precisely the constraint that the HBM long-term contract mechanism imposes on short-term price elasticity. Korea Investment & Securities believes that the locked-in prices under HBM long-term contracts have limited the extent to which SK Hynix benefits from the conventional DRAM price hike cycle. Meanwhile, SemiAnalysis bets that the robust price increases of commodity DRAM will be sufficient to offset this impact, and the mass production of HBM4 will also provide subsequent momentum.

SK Hynix CEO Kwak Noh-jung previously stated that 2027 will become the tightest year of supply in the history of the memory industry. The Bank of Korea also released a report in an attempt to reassure the market, stating that the AI-driven industry supercycle is expected to persist, with the current momentum driven by competitive corporate investments in anticipation of the AI revolution, rather than traditional cyclical demand.

The essence of this volatility is a collective revision by the market of SK Hynix's valuation logic. Prior to the ADR listing, the domestic share price in South Korea had already fully priced in the "price increase restriction" effect of HBM long-term agreements; after the ADR listing, investors began to evaluate the company through a different framework. While short-term volatility may not be over, what is more worthy of attention than the decline itself is whether long-term contracts can truly alter the inherent cyclicality of the memory industry. If future earnings indeed stabilize, the current valuation logic may need to be reexamined.

What to Do at Current Position?

Already holding ADRs: A single-day sharp decline should not be used as a basis for trading decisions. If the buying thesis is based on the HBM supply shortage and elevated AI capital expenditures, there has been no material change in the fundamentals for now, and the long-term AI trend remains intact. However, volatility is highly likely to amplify during the earnings season; investors could set stop-loss levels or trim positions in tranches to manage risk.

Preparing to build or add to positions: Current levels may not be the absolute bottom, but they have entered a relatively reasonable range. Investors can adopt a 'pyramid-style' approach to buy in tranches, first establishing a 30% initial position, and adding more if the price falls further.

Just observing: It might be better to wait for Microsoft's earnings report on July 28. If Azure's growth exceeds expectations, SK Hynix is highly likely to rebound; if it misses expectations, there may be lower price points ahead.

SK Hynix's current decline stems more from technical corrections and liquidity shocks following excessive earlier gains, and the medium-term supply-demand dynamics of HBM have not undergone any directional shift. Investors with light or no positions can use this correction to reassess entry levels, though the specific timing should be determined in conjunction with upcoming earnings data.

Recommended Articles