Apple (AAPL) Stock Price Forecast: Chinese Chip Talks Drove $300 Return - Can It Break $317?

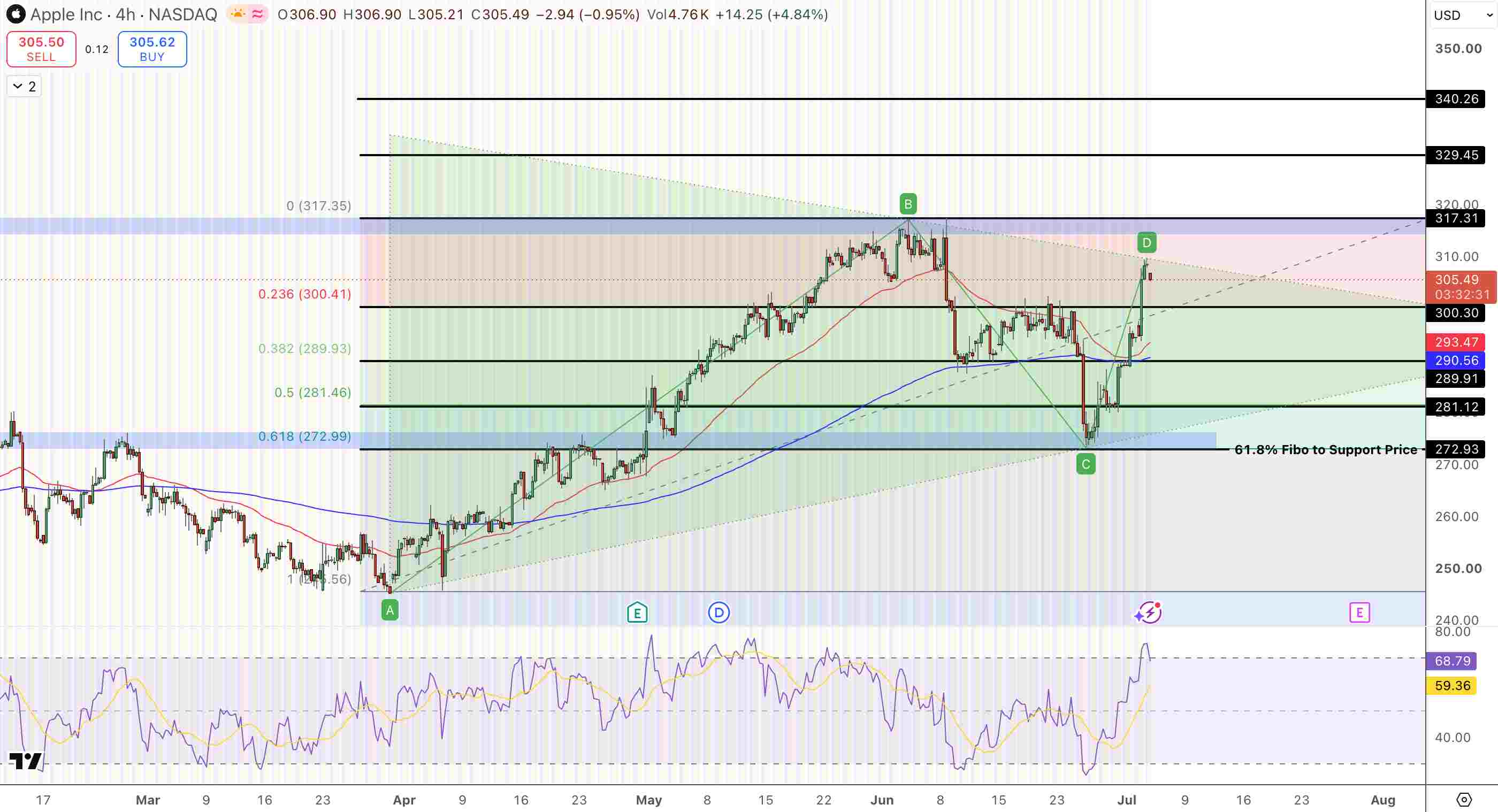

TradingKey - Apple (NASDAQ: AAPL) changed hands at $305.49 as it builds the base for the symmetrical triangle after reclaiming the $300 level on July 2 with a 4.59% gain. The rally was triggered by the news Bloomberg published that Apple was talking with the Chinese memory chip suppliers, CXMT and YMTC, for chips that will be included in iPhones sold inside the country. This move could come from Apple to keep memory costs down after reportedly increasing 271.79% for the iPhone 18 Pro. Relative Strength Index is 68.79 as Apple is not yet considered overbought.

Apple reports its Q3 2026 earnings (Fiscal quarter 3, or the period from April 1 through June 30) on July 30. A breakout and close above the triangle at roughly $317.30, could pave the way to the 52-week high of $317.40. A move above the triangle resistance could see the stock rise toward the $340.30 measured move.

Why Apple Is Considering Chinese Memory Suppliers

Apple’s discussions with Chinese memory chip makers CXMT and YMTC could show how Apple is looking at managing its supply chain. Though both memory chip makers are on the Commerce Department’s Entity List that prohibits U.S. companies from doing business with them, Bloomberg reported that Apple was considering buying chips from these companies for products that will only be sold in China.

Memory costs for the iPhone 18 Pro have reportedly surged 271.79%. A drop in memory chips can ease the strain. DRAM and NAND prices have also risen for the wider industry. Apple is reportedly planning on making around 10 million foldable iPhones, as well as bringing on board a slew of iPhone 18s, a refreshed entry-level MacBook Pro, and a new iPad Pro. With more phones coming out, there’s also increased demand for memory chips. Whether sourcing memory chips from Chinese chipmakers can help Apple cut costs remains to be seen. It could help ease the burden, but could bring up other challenges.

July 30 Earnings Will Test Apple's Margin Outlook

Apple's fiscal Q3 2026 earnings, scheduled for release on July 30, will likely offer investors their first substantive indication of the impact rising memory costs are having on profitability. Management previously indicated that gross margins would land in the range of 46.5% to 47.5% in fiscal Q3, representing the early effects of the increase in component costs. Whether these increases across Macs, iPads and iPhones were sufficient to keep the margins intact will be a key thing to keep an eye on.

The report will also contain guidance for fiscal Q4, which includes the launch of the iPhone 18. That guide should provide the first look at what management expects demand, pricing and profitability to look like. JPMorgan expects to see an average selling price increase of around $50 per device, driven by AI features, the launch of a foldable iPhone and the rising memory costs.

Services have been the source of stability in Apple's earnings profile. They generated $31 billion in revenue in Q2 and enjoyed operating margins that came very close to 49%, benefiting from:

- App Store

- Apple Music

- iCloud

- Apple TV+

- Apple Pay

on more than 2.2 billion active devices. This provides Apple with consistent cash flow, in spite of pressures on the hardware gross margin. While analysts aren't convinced AI alone will lead to increased upgrade cycles this year, a more robust product roadmap, including the development of a foldable iPhone reportedly expected to ship around 10 million units, could lead to stronger demand relative to years past.

AAPL Technical Analysis: Triangle Pattern Targets $340.30

On the 4-hour timeframe AAPL is continuing to form within a symmetrical triangle pattern near $305. RSI is at 68.79, which has not yet become negative, while buyers are continuing to defend the 0.618 fibonacci retracement near $273.

Apple (AAPL) Stock Price Chart - Source: Tradingview

A breakout above $317.30, which is just below the 52-week high at $317.40, would conclude the pattern and send price toward $340.30. A close below $272.90 would rule out the bullish scenario.

Entry: Long above $317.30 Target: $340.30 Stop Loss: Close below $272.90

Catalysts

- Apple is investigating memory sources from CXMT and YMTC for devices to be sold in China

- iPhone 18 Pro's memory costs reportedly rising 271.79%

- Foldable iPhone target increased to 10 million units

- Q3 results on July 30 with gross margin, plus guidance on iPhone 18

Why Is Apple Talking to Chinese Memory Chipmakers?

According to reports, Apple appears to be looking to Chinese DRAM and NAND chipmakers CXMT and YMTC to source memory chips for iPhone models manufactured in China. While these companies are on the US Commerce Department's entity list, it looks like this deal would only apply to devices made in China and sold to Chinese consumers. This comes at a time when component costs have increased. It's expected that memory costs for the iPhone 18 Pro have climbed by 271.79%. DRAM prices are up by as much as 58 to 63% quarter over quarter. This would appear to make sense for Apple to look to source components from China in one of its most important markets.

What Is Apple's Foldable iPhone Strategy?

Apple has reportedly increased its production target for the foldable iPhone to 10 million units. The Cupertino, California company is getting ready for the arrival of the first iPhone in its product lineup with a foldable screen. Bloomberg adds that the company also has five additional iPhone model launches set to come out between now and 2027, as well as additional launches for the Mac and iPad. With the Apple hardware product lineup becoming more diverse and extensive, demand for additional memory chips might be required for these new products. The decisions on chip sourcing made today could help Apple maintain its profit margins on iPhone 18 Pro sales going forward.

Bottom Line

Apple's stock bounced from support near $273 before trading in a tight range just below its $317.40 52-week high and closed at $305.49 Friday. A news report that Apple is looking at alternative chip manufacturers from China could mean there are additional component costs coming up in the iPhone 18 product line. Apple's earnings call on July 30 could reveal how the company is handling supply chain moves to protect margin while continuing to launch new products to complement the iPhone 18 product line. On the technical chart, Apple is still in a symmetrical triangle. A breakout and close over $317.30 would have $340.30 in sights. A close below $272.90 would mean a bullish case is no longer in place.

Recommended Articles