1 Jaw-Dropping Metric Proves Wall Street Is Completely Wrong About This Battered Artificial Intelligence (AI) Hyperscaler

Key Points

Meta has AI aspirations, but it's still mostly an advertising business.

Its revenue growth is among the fastest for the big tech companies.

- 10 stocks we like better than Meta Platforms ›

Wall Street loves some stocks and despises others. There can be a lot of reasons for a stock to fall out of favor, with some of them being legitimate and others being a bit less concrete. It's the battered stocks in the latter category that I'm looking for, as they often have the potential to turn into massive long-term winners.

One stock that I've got my eye on that has been battered over the past year is Meta Platforms (NASDAQ: META). It's down by more than 25% from its all-time high, but I think Wall Street has its analysis of Meta all wrong, which is why now may be the perfect buying opportunity.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

The market views Meta as an AI company. It isn't.

The market typically lumps Meta in with the other three AI hyperscalers: Alphabet, Microsoft, and Amazon. They are the four biggest spenders in the AI sector, and are pouring hundreds of billions of dollars annually into building data centers. What sets Meta apart from the other three is that it is using all of the computing power it's building for internal purposes. The others have thriving cloud computing business units that help them generate profits to offset their costs and make their investments viable in the long term.

Meta is only using its AI data centers to train and power its AI systems, and so far, the results from those efforts have been relatively lackluster. When you hear about a cutting-edge AI model that's wowing the world with its capabilities, the one being discussed is rarely Meta's Llama. That's a problem, as it indicates that Meta is likely behind the pack on large language model development. However, some of the expected use cases for its AI model haven't arrived yet. Meta is going all in on a different form factor for its AI interface: smart glasses. It envisions a future where AI will be connected to cameras that allow it to perceive the world around the user, analyze what it sees, and deliver contextualized AI for the user. Meta's current AI glasses are only a fraction of what it hopes to produce in the future.

In the meantime, it's just an advertising company. Meta derives most of its revenue from selling ads on its social media platforms, which it has improved using its AI models. This is leading to strong growth in its own right; revenue rose 33% year over year in the first quarter. I think most investors should think of Meta as a social media business. Viewed through that lens, Meta looks like a pretty cheap stock right now.

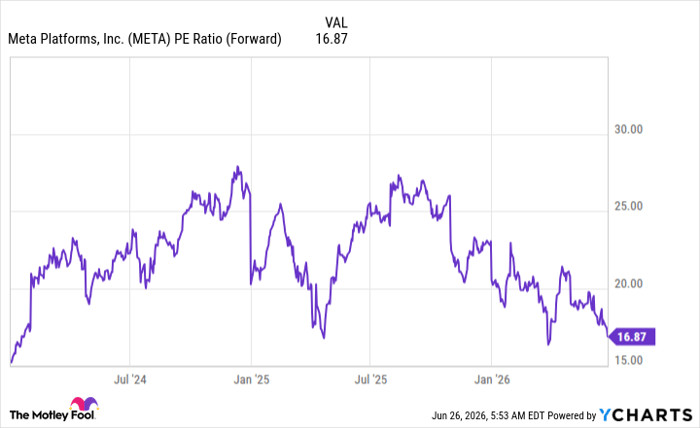

META PE Ratio (Forward) data by YCharts.

Meta trades at a dirt-cheap 17 times forward earnings, which is among the cheapest levels it has traded at over the past few years. That's a low price to pay, especially considering the S&P 500 (SNPINDEX: ^GSPC) trades for around 21 times forward earnings. The contrast between Meta's rapid growth and its low price shows why Wall Street is wrong on this one. Long-term investors would be smart to load up on shares now.

Should you buy stock in Meta Platforms right now?

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $385,055!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,228,089!*

Now, it’s worth noting Stock Advisor’s total average return is 902% — a market-crushing outperformance compared to 209% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 1, 2026.

Keithen Drury has positions in Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool has a disclosure policy.

Recommended Articles