The Simplest Graph Shows Exactly Why GM Is a Big Buy -- but There's 1 Huge Drawback

Key Points

Automakers have negative narratives for being cyclical, capital-intensive, and low-margin.

General Motors and Ferrari have both broken free of historically low P/E ratios.

Buybacks have been critical to GM's valuation rise, and that could slow as the stock becomes more expensive.

- 10 stocks we like better than General Motors ›

Detroit automakers such as General Motors (NYSE: GM), Ford Motor Company (NYSE: F), and Stellantis (NYSE: STLA) (if you still count the latter) have long been plagued by low valuations. While Wall Street is slowly changing its perception of these automakers as investments, thanks to a more intriguing and lucrative future centered on driverless vehicle technology and increasing software monetization, automakers' valuations seldom rise above a modest 10 times price-to-earnings ratio.

Let's cover what holds valuations down and, with one simple graph, show how GM has finally broken free of this confinement.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Stereotypes are changing

In the past, investors shunned automakers as long-term investments due to many negative factors. Those include the view that automakers were highly cyclical, leaving them exposed to boom-and-bust economic volatility; ballooning legacy costs such as pension and healthcare obligations; capital-intensive operations that left them with thin margins; and the "dinosaur" narrative, in which management was slow to adapt and sometimes arrogant.

Image source: General Motors.

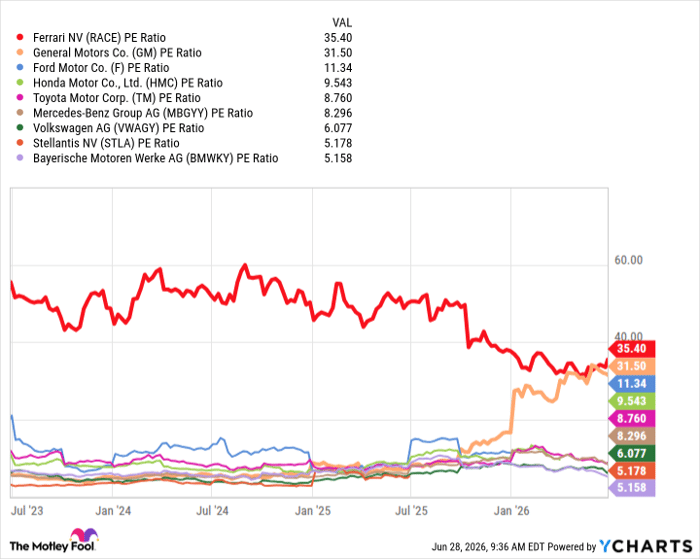

Those narratives are slowly changing, but for the most part, automakers' valuations have stayed stuck in neutral -- that is, except for General Motors. A rare longtime exception to these low valuations was Ferrari (NYSE: RACE), which has long recorded absurdly high margins and broke free of being viewed as a traditional automaker long ago, and is treated more as an ultra-luxury stock. That's why the following graph is so telling for long-term investors, because finally, another automaker has broken free of these chains and, impressively, matched Ferrari's lofty valuation.

Data by YCharts.

As you can see, especially over the past year, GM's valuation has rapidly approached Ferrari's lofty position, while the remainder of the automotive industry struggled to break a 10x P/E ratio.

How did GM break free?

One of the primary driving forces behind GM's rapid valuation increase is how it chooses to return value to shareholders. While crosstown rival Ford is heavily lauded for its often lucrative dividend yield, which generally checks in between 4% to 5% and in recent years has been boosted with an annual special dividend due to better cash flow, General Motors has taken a different approach and essentially bet on itself and repurchased massive amounts of stock on the cheap.

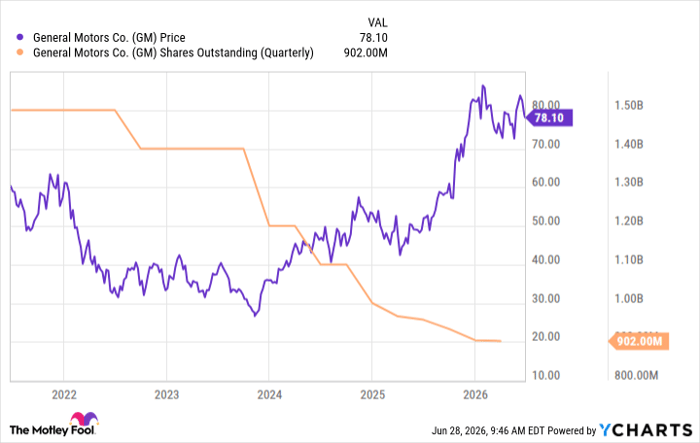

In fact, GM has spent a staggering $30 billion on share buybacks over the past five years and retired about 500 million shares over that span. Going hand-in-hand with share buybacks is that Wall Street is rewarding GM's free cash flow, enabling it to make these massive purchases: GM has generated roughly $53 billion in free cash flow since 2021 despite the COVID-19 pandemic, inflating prices, tariffs, and trade policy changes. The next graph shows just how drastically GM has reduced its shares outstanding and the price increase it helped drive.

Data by YCharts.

One major drawback right now is that, because share repurchases have been a big driver of GM's improving valuation, it's become more challenging as the shares aren't nearly as cheap as they once were. Don't expect GM to pull back on its strategy just yet, but it could change the benefits the strategy has driven recently.

What it all means

Investors could certainly argue that Ford deserves a better valuation than it's currently receiving, especially given that it returns significant value to shareholders through its dividend and has seen a large boost in market capitalization following the unveiling of Ford Energy, which seizes on the growth in AI infrastructure and energy demand. However, Ford also has much work to do on its vehicle quality and has led the U.S. industry in massive recalls, which have increased warranty costs that dinged its earnings on a couple of occasions.

However, Ford's crosstown rival, GM, is doing something that only Ferrari has achieved, driving its P/E multiple nearly three times that of many of its competitors. That's because Wall Street is recognizing not only GM's impressive cash flow, but its reduced share count thanks to buybacks, as well as growing high-margin business and recurring revenue from digital services such as OnStar and Super Cruise. One major reason for investors to buy into GM over its competitors is that it's finally broken free of historically low automaker P/E multiples. These graphs may be simple, but they speak volumes.

Should you buy stock in General Motors right now?

Before you buy stock in General Motors, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and General Motors wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $385,055!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,228,089!*

Now, it’s worth noting Stock Advisor’s total average return is 902% — a market-crushing outperformance compared to 209% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 1, 2026.

Daniel Miller has positions in Ford Motor Company and General Motors. The Motley Fool has positions in and recommends Ferrari. The Motley Fool recommends Bayerische Motoren Werke Aktiengesellschaft, General Motors, and Stellantis. The Motley Fool has a disclosure policy.

Recommended Articles