Microsoft Stock Forecast: Is Spending $190 Billion on AI Infrastructure in 2026 — Is MSFT a Buy at $452?

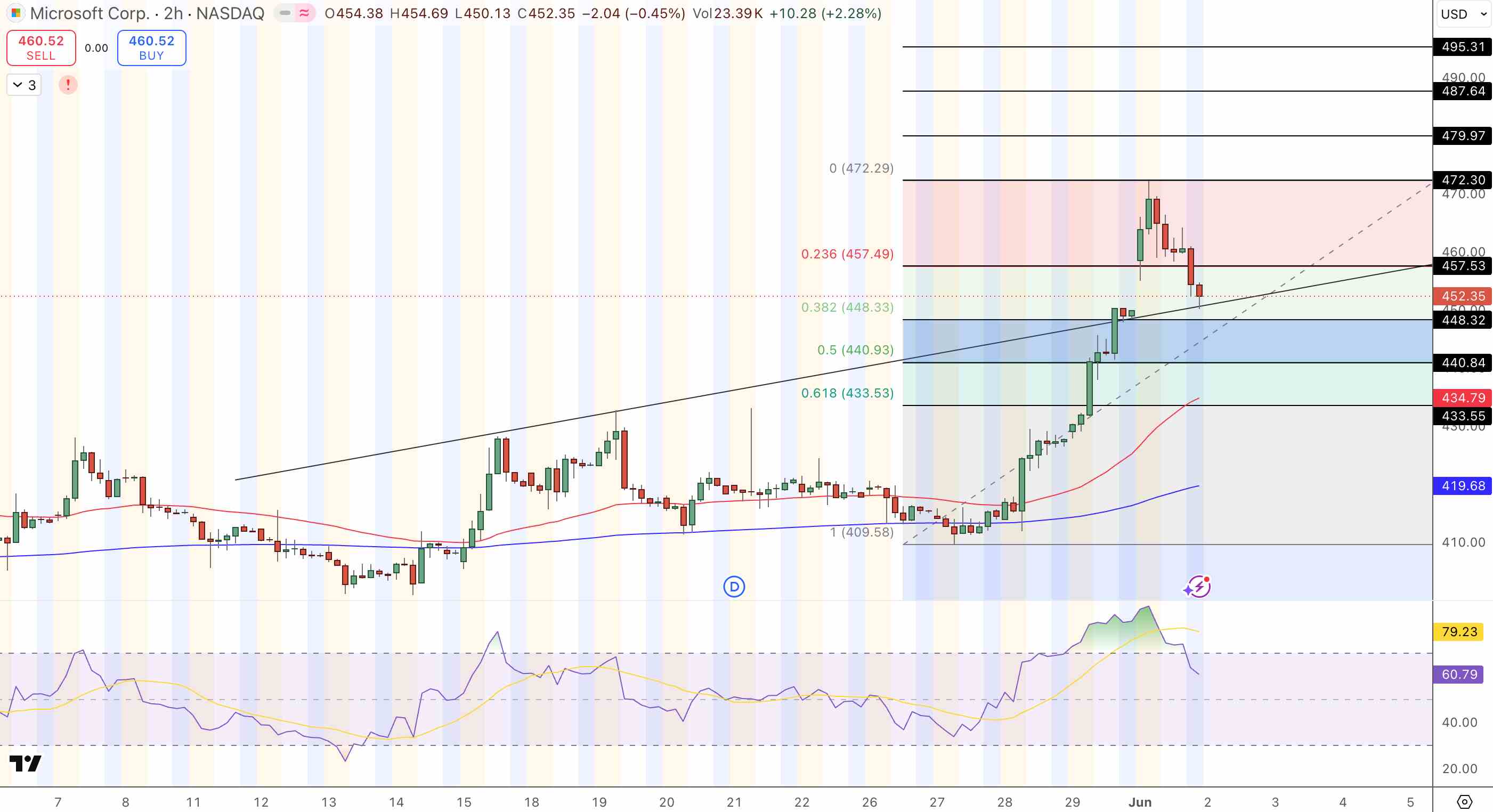

TradingKey - As of June 2, Microsoft (NASDAQ: MSFT) is trading at $452.35. This marks a breakout above the 0.618 Fibonacci retracement at $433.53, underpinned by strong bullish candles and an RSI nearing 79, all while the stock trades within an upward-sloping two-hour channel originating from the $409.58 lows.

Just as the stock moves higher, Microsoft Build 2026 begins today, an annual gathering for developers where we expect headlines on AI agents, Copilot upgrades and Windows AI functionality. However, Microsoft's Q3 FY2026 earnings from late April already provide the fundamental context: Revenue of $61.9 billion increased 13% year-on-year. Azure revenue rose 31% and was aided by a surge in the growth of AI services. Further, over 80% of Fortune 500 companies were using Azure AI services.

That number stands out above all others as the figure that will define both the upside and downside scenarios for MSFT: Capital expenditures of $190 billion in 2026.

What Microsoft's $190 Billion AI Capex Commitment Really Means

Microsoft has said it plans to invest approximately $190 billion in capital expenditure in calendar year 2026, mostly to build data centers, GPUs and AI infrastructure. To put it in perspective, that is more than the yearly revenue of most S&P 500 companies, greater than AWS's annual revenue in total, and an extraordinarily risky bet that the AI-driven growth in cloud consumption will be sufficiently large and rapid enough to yield a return on that money over a reasonable timeframe. That's not discretionary IT spend. It's a declaration of intent that Microsoft wants to become the AI infrastructure go-to for the global corporate sector, and it is willing to bear some short-term margin pain to accomplish that goal.

For MSFT shares at $452, the main question of ROI is what bulls are counting on. The $190 billion capex is expected to reduce free cash flows and reduce capital allocation in 2026. But that same Azure growth rate, 31%, is the key bullish thesis, as the fastest growth in the peer group of hyperscalers on a $26.7 billion revenue base is a leading indicator that there is demand that can absorb that capacity increase. Azure AI services account for a portion of that 31%. According to management's language, demand for AI services, on some GPU-enabled services in particular, exceeds supply. A company that is supply-constrained on its highest-growth product isn't betting that $190 billion in capacity is speculative; they build capacity when the signals are there to support the spending.

Azure at 31% Growth and the Copilot Monetization Layer Above It

Azure grew revenue by 31% on the surface, but the real story is what is happening underneath. Enterprises turn to Azure for training and deploying large language models, and not for general-purpose computing economics but because of the OpenAI partnership, along with Azure's AI-optimized tooling in Azure AI Foundry, Azure OpenAI Service and the availability of AI-optimized compute. Over 80% penetration into Fortune 500 companies for Azure AI services proves that this isn't just a marketing exercise; these are production deployments at scale. Once you have 80% of Fortune 500 companies already using Azure to run their AI workloads, the costs of migrating to a competing cloud platform continue to escalate with each model trained, API used and workflow configured to take advantage of Azure-specific tools.

Copilot is the monetization layer built on top of infrastructure deployment. Microsoft has put Copilot into all of its applications: Microsoft 365, GitHub, Power Platform, Teams and Windows, the core of its commercial installed base. The revenue story is a straightforward $30 per user per month Copilot add-on over existing Microsoft 365 E3 and E5 enterprise licenses. Given that there are hundreds of millions of commercial users of Office apps alone, any meaningful deployment of Copilot can add billions of high-margin revenue per year to Microsoft's top line. Microsoft Build 2026 today will likely announce the next generation of Copilot agents, the AI-driven software that can take on multiple steps to perform a given task instead of just answering questions. Agent-powered Copilot is a product in a new tier with a higher price, representing another step forward in the monetization curve.

MSFT Technicals: 0.618 Fib at $433 Cured at $452, RSI 79, Price Targets Are $472 and $480

On the 2H chart, MSFT broke out above the 0.618 Fib retrace at $433.53 and 0.5 level at $440.93 with a string of big bullish candles starting at the $409.58 trendline foundation. Current price stands at $452.35 on the $448.32 to $452.35 horizontal cluster above the black ascending trendline. RSI is currently just around 79 but there is no bearish signal of divergence, strong momentum but not exhaustion.

The wicks on pullback show resistance at the 0.236 Fib at $457.49. Price targets are $472.29, the 0% Fib extension, and $479.97, the upper band of the channel. A sustained close below $448.32 would invalidate the short-term bullish structure.

- TRADE ENTRY: Long above $457.49, 0.236 Fib breakout

- TARGET 1: $472.29, 0% Fib extension

- TARGET 2: $479.97, channel upper bound

- STOP: $448.32, daily close below, invalidation of horizontal support

What Did Microsoft Report in Q3 FY2026 Earnings?

Microsoft's Q3 FY2026 revenue came in at $61.9 billion, a 13% increase over the same period last year. The company's Intelligent Cloud division brought in $26.7 billion, a jump of 17% from a year ago. Azure, the company's cloud computing platform, saw a 31% revenue increase, primarily fueled by the popularity of AI-based services. Over 80% of Fortune 500 companies are currently adopting Azure AI services. The company's adjusted EPS also surpassed analysts' expectations. For calendar year 2026, the company expects to spend nearly $190 billion on capital expenditures. This spend will mostly be on data centres, GPU clusters, and AI infrastructure. The company is slated to announce its Q4 FY2026 earnings results in late July.

Why Is Microsoft Going All Out with a $190 Billion Spending Plan on AI Infrastructure This Year?

Microsoft's $190 billion 2026 capex commitment shows how confident management is that demand for AI services within cloud computing will grow big enough to warrant such a heavy expenditure. Azure revenue growth at 31% year-on-year against the already bloated $26.7 billion revenue base and the significant AI contribution to Azure growth are signs enough of this. Management has gone so far to say that current AI demand is exceeding Azure's ability to supply AI services on GPU-backed compute.

A business on short end of supply won't construct $190 billion worth of capacity in a speculative manner; it does so because it sees that demand is clearly present. While there's a chance margins could temporarily take a beating due to the large investment, the longer-term narrative is that this new capacity will ensure Microsoft stays at the top of the AI infrastructure chain over the next 10 years.

What Is Copilot?

Microsoft Copilot is essentially an AI assistant integrated into Microsoft 365, GitHub, the Power Platform, Teams, Windows, and several other areas of the Microsoft ecosystem. The commercial version adds about $30/user/month to enterprise MSFT 365 software. MSFT has hundreds of millions of commercial Office users and even very modest Copilot adoption would generate a few billion in incremental high-margin annual revenue. The company is expected to announce the next generation of Copilot, which consists of AI agents capable of taking autonomous multi-step actions rather than just answering questions, during today's opening of Microsoft Build 2026. It represents higher-end products with a higher price.

Bottom Line

Microsoft's $190 billion AI capex commitment, Azure's 31% growth rate, 80%+ penetration of AI services among Fortune 500 companies, and hundreds of millions of Copilot enterprise seats are what constitutes the bull case for the stock right now. That said, the aforementioned AI capex is expected to squeeze Microsoft's free cash flow in the near term, constituting the bear case.

With the stock trading at $452, it has cleared the 0.618 Fib in its rising channel with an RSI of 79 but no divergence. The stock has an upside target of $472.29 with a subsequent target at $479.97 provided it closes above $457.49.

The Microsoft Build 2026 today will be an immediate catalyst for this bullish scenario to play out. Microsoft's Q4 FY2026 earnings report in late July and the Warsh FOMC June 16 to 17 meeting are next on the fundamental and macro agenda respectively.

Recommended Articles