Cisco Q3 Preview: Can Traditional Hardware Stabilize After Pressure and AI Orders Turn the Tide?

TradingKey - After the U.S. market close on May 13, Cisco (CSCO.US) will release its third-quarter financial results for fiscal year 2026. The company previously provided a revenue guidance range of $15.4 billion to $15.6 billion, with the Wall Street consensus sitting around $15.56 billion. The adjusted earnings per share (Non-GAAP EPS) guidance is $1.02 to $1.04, with the analyst mean estimate at approximately $1.04.

Cisco has been a subject of ongoing controversy for years, with investors deeply divided over the networking giant. On one hand, its legacy networking business has seen year-over-year revenue declines for five consecutive quarters; on the other hand, AI networking orders are beginning to materialize.

As Cisco continues to play catch-up in the AI race, the core question for the market is whether its efforts in the AI space are sufficient to offset the ongoing retreat of its legacy hardware division.

AI Networking Orders Rise; Scale Remains Key

According to data disclosed by Cisco in its fiscal Q2, the AI order backlog from hyperscale customers has exceeded $2 billion. JPMorgan analyst Samik Chatterjee noted that the company's guidance for more than $4 billion in hyperscale AI orders for fiscal 2026 is merely a minimum target, suggesting significant upside potential.

[ Cisco Silicon One G300, source: Cisco]

In February this year, Cisco released its revolutionary networking chip, Silicon One G300, providing 102.4 Tbps switching speeds. Designed specifically for gigawatt-scale AI clusters, it claims to reduce GPU cluster job completion times by 28%.

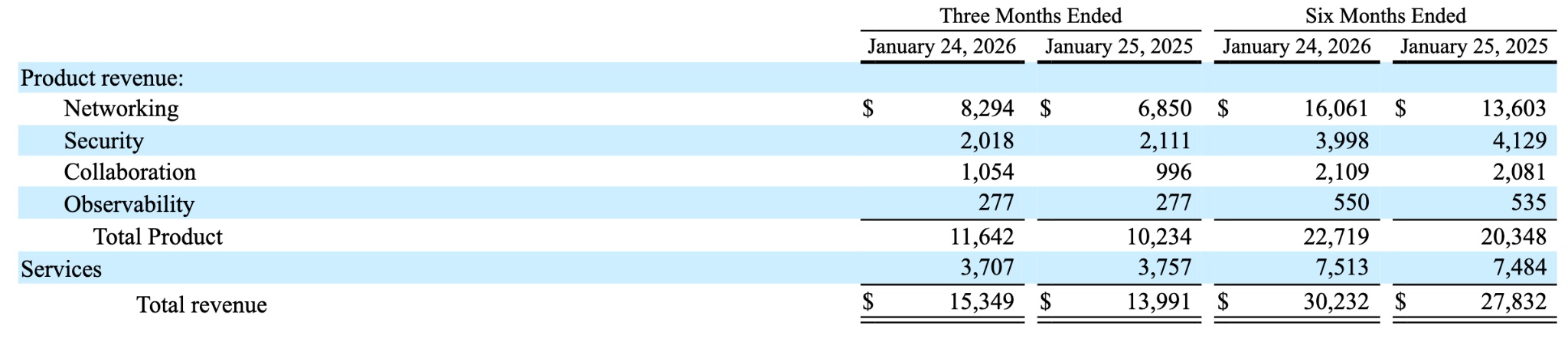

[ Fiscal Q2 Revenue Performance, source: Cisco]

Against the backdrop of long-term market share erosion by NVIDIA's Spectrum-X in the data center Ethernet switch market, the G300 is a critical product for Cisco to regain its leadership. However, several quarters often pass between the product announcement and its deployment in customer racks, so the actual revenue contribution from this product this quarter is expected to be quite limited.

Of particular note is the strategic depth of Cisco's series of acquisitions. Following its $28 billion acquisition of data security and observability leader Splunk, the company announced the acquisition of AI observability startup Galileo Technologies in April, integrating it with the Splunk platform to provide customers with full lifecycle management for LLM agent development.

Although the Galileo transaction is expected to close in Cisco's fiscal Q4 and will not contribute to Q3 results, it adds more potential to the Q4 guidance and serves as a catalyst for bullish investors to further bet on Cisco's deep commitment to the AI space.

Security business becomes core; traditional hardware under pressure.

Security and observability operations have become a core pivot for Cisco's overall growth. Market consensus expects year-over-year revenue growth for security and observability, including Splunk, to remain between 20% and 25% this quarter. Splunk is projected to be accretive to non-GAAP earnings per share this fiscal year, with sustained positive operating cash flow.

However, the traditional networking and switch hardware business is still in a structural digestion phase. Enterprise customers continue to scale back capital expenditures, and an 8% year-over-year decline in Ethernet switch revenue continues to weigh on overall top-line results. To sustain positive revenue growth, Cisco's security business and AI-related orders must continue to fill the gap left by the traditional hardware segment at an accelerated pace.

Market Divergence Persists; Earnings Guidance in Focus

Institutional sentiment toward Cisco is generally optimistic. JPMorgan analyst Samik Chatterjee raised the price target from $95 to $96 earlier this month, reiterating an "Overweight" rating. UBS also raised price targets across the networking hardware sector in its Q1 earnings preview. Wedbush analyst Moshe Kattri stated that Cisco is transforming into an AI infrastructure giant.

However, divergence is equally apparent, with the core market debate centering on profit absorption capacity. Cisco's Q2 non-GAAP gross margin was 68.8%, slightly below analyst expectations of 69.0%, primarily due to persistent pricing pressure on legacy hardware.

While most institutions have been raising price targets, their earnings forecasts include stringent assumptions regarding sustained gross margin pressure. With current quarter gross margin guidance between 65.5% and 66.5%, if actual data approaches the lower end, the bullish thesis—which has already factored in optimistic AI valuations—could be weakened.

What should investors focus on?

From a valuation perspective, Cisco's stock price has climbed more than 27% year-to-date, yet many institutions remain cautious about the translation of Cisco's AI narrative into earnings contributions.

The traditional networking hardware business remains in a phase of "order digestion coupled with destocking," while AI hyperscale orders are in a transition period as initial deliveries are being realized and the G300 volume ramp-up awaits verification. Cisco is currently undergoing a repricing phase as it transitions from a traditional networking equipment vendor to a dual-engine model of AI networking and security—a long-term transformation that will take time to validate.

For investors, the highlight of Cisco's third fiscal quarter lies in management's qualitative judgment regarding the pace of AI order conversion over the next 12 to 18 months. Meanwhile, whether bottoming signals for traditional hardware orders have emerged is also an anchor of certainty that more and more sidelined capital is seeking in this valuation play.

Recommended Articles