Alphabet Q1 Preview: How Much Upside is Left

Alphabet (GOOG/L) entered 2026 as a true AI champion, with the stock price being up 115% (118% for GOOGL) in the last 12 months.

For 2025, the GOOG revenue machine can be simplified into 3 components

- Advertising (which is mostly search advertising, Google Network and YouTube advertising) – 73% of the total revenue in 2025, growing at low teens % y/y

- Subscription (YouTube Premium, YouTube Music, App Store) – 12% of the total revenue, growing at high teens % y/y

- Cloud – 15% of the total revenue, growing at +35% to 40% y/y

Overall, it looks great – the ad cash cow is stable, and the cloud is in a hypergrowth stage

In terms of profitability, things have been great too. The operating margin of the advertising and subscription businesses (the management piles them up together as “Google Services”) is above 40%. Further to this, Google Cloud operating margins also expanded a lot: in 2025Q1, the OPM was 18%, and in 2025Q4 it reached 30%.

Advertising

So far, the fears that AI will cannibalize GOOG ad revenue seem unjustified; if not, AI is boosting the revenue growth with better-targeted advertising and higher ROI for the advertisers. We can see this from the recent Google Search revenue growth numbers: 2025Q1 Google Search revenue growth was 9.8% y/y, in 2025Q2 it was 11.7% y/y, in 2025Q3 it was 14.5% y/y and in Q4 the growth rate event went further up -16.7% y/y. If Google AI was cannibalizing search revenue, we would have seen growth numbers decelerating, but that’s not what is happening right now.

The reasons behind this are multiple. Firstly, more complex search queries in the past could not drive revenue, but now with Gemini and Google AI, monetization is possible. Secondly, more AI tools for advertisers will bring more advertisers’ money drawn by the high ROI. Thirdly, non-search products like Map, Gmail, and Discover are still in a rather early stage of monetization

The whole idea is that if advertising is a product, Google is moving from selling a standardized product to more specialized (tailor-made) products at a higher price.

On the YouTube side, ad revenue growth is maturing, but we will see more users switching to subscription plans, which, in fact, is a better margin business. Why? Because running digital ad bidding in general is more compute-intensive than just running a subscription business. It is estimated that revenue from 1 subscription plan ($12-$16 per month) is equivalent to watching thousands of videos on an ad-only plan

The YouTube/FIFA 2026 deal (showing highlights from games) will bring a near-term boost to both ad and subscription revenue, but on the contrary, Google has higher exposure to middle east (29% of revenue comes from EMEA, much larger than META) and the recent Iran crisis might be a short-term headwind for Ad revenue growth there.

Cloud

Google Cloud Revenue is $58.7 bn for 2025, and it is expected to grow at an impressive rate of roughly 40% y/y driven by the following factors:

- Massive backlog of $240bn, which is 4x of the 2025 revenue, will gradually flow into the revenue line;

- Growing sales of TPUs to third parties: TPU sales to third parties are still less than 10% of the cloud revenue, but with time, they will become a larger portion of it. Anthropic will utilize GOOG’s TPUs, and more clients are expected to follow. Moreover, TPU sales to 3rd parties will be highly accretive to the margins, due to its licensing business model

Google Cloud is transforming from enterprises using AI to more of a network of agents; the more AI agents are embedded in the customers, the harder it is for them to move away from Google as a cloud provider.

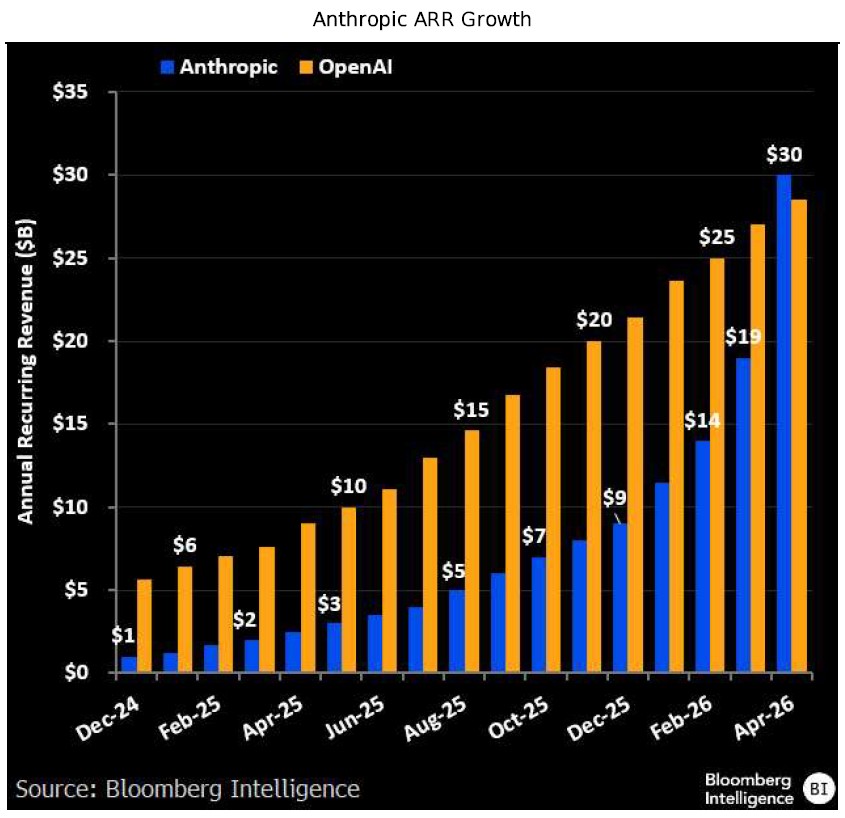

Investment in Anthropic

Google has committed to investing up to $40 billion in the AI startup, providing $10 billion immediately and up to $30 billion more based on performance milestones, valuing the company at $350 billion (15% ownership). Anthropic ARR is already outpacing OpenAI, but the valuation is still less than half of OpenAI, which means GOOG investment has a big room for appreciation

For Google, Anthropic is less of a threat compared to OpenAI; OpenAI is more toward retail, challenging Google Search, while Anthropic is more of an enterprise. The main purpose is to sell TPUs and cloud computing to Anthropic. With more computing power from GOOG, Anthropic will be unblocked and deliver even more revenue and profit – hence more investment return for GOOG.

Source: Bloomberg Intelligence

How to View GOOG Margins

GOOG reports operating margins the following way:

- Google Services (ad + subscription) OPM

- Cloud OPM

- Both are offset by FX hedging and other smaller loss-making businesses like Waymo and “other bets”

The advertising business margins are around 40%-41%; these are rather mature margins, and there is just modest room for growth. Traffic Acquisition Costs and revenue sharing from YouTube are rather stable and unlikely to go down as a percentage of revenue.

With Capex growing at a much faster rate than revenue (Capex is expected to be $185bn or 2x as big as 2025), we expect depreciation as % of revenue to increase. However, the increase in usage of home-made TPUs will decrease expenses related to computing power.

The cloud business is where we will see more meaningful margin expansion. Cloud margin in 2025 stands at 23.7%, but that is not a mature level yet, and will expand more towards 30%.

TPUs will cut computing costs, neutralize the Nvidia tax, and the sales of TPUs to third parties will boost margins too. We expect in the coming 2-3 years cloud margins to reach nearly 40% and can even surpass the level of MSFT (whose cloud margins are around 42%). GOOG can go even higher due to its in-house tech stack.

Source: Bloomberg Intelligence

How can proprietary chips improve profitability, looking into GOOG cost structure?

Cost of revenue for GOOG is around 40% of the total revenue:

o Roughly 30% of the CoR, or 12% of the revenue, goes for TAC (total acquisition costs)

o Depreciation represents around 5-10% of the total revenue

o Power and Cooling represent 10-15% of the total revenue

o Rest is networking, content licensing, servers etc…

Component | Approx. % of Revenue | Notes |

TAC | 8–12% | Partner payouts (Apple, creators, AdSense); closer to 10–12% of revenue than 22–30%. |

Depreciation | 5–10% | Servers, DCs, TPUs; rising with AI capex. |

Power + Cooling | 10–15% | Major share of DC OpEx; highly sensitive to chip efficiency. |

Network / Colo | 3–5% | Bandwidth, leased capacity, etc. |

Content Licensing | 2–4% | YouTube sports, music rights, etc |

Support / Review | 2–3% | Moderation, customer‑service vendors. |

Servers / Inventory | 2–4% | Hardware amortization beyond core depreciation. |

Total CoR | ~25–30% |

Realistically, TPUs can deliver 2-3 percentage points (pp) of operating margin expansion. This comes primarily from cutting the power + cooling cost line by 25-40%, another 4-5pp will come from cloud business expansion, so we can assume around 40% operating margin by the end of this decade.

Risks

Perhaps the major concern for investors is the fact that GOOG's free cash flow (FCF) in 2026 may turn negative. Capex is expected to be $185bn or 2x as big as 2025, but at the same time, Operating Cash Flow in 2025 was $165bn, and it is unlikely to see a big jump in OCF as net profit may grow by less than 30%. That certainly means FCF will drop a lot in 2026, and this may spook investors, but GOOG can still tap the debt markets for cheap capital,

To maintain an investment-grade rating, a rule of thumb is that total debt should be around 2.5x EBITDA. The 2025 EBITDA of GOOG was around $150bn ($129bn operating income + $21bn depreciation), this means around $375bn of total debt that GOOG can bear before their credit rating gets hurt, (and currently the total debt is just $47bn), so not only they can finance their capex with their FCF but they also have a great capacity to get more debt financing.

Slowdown in advertising due to macro headwinds – this can lower ad revenue growth, but GOOG (and META) are gaining more market share with their superior AI-driven ad products. Currently, the top 3 (META, GOOG and AMZN) control roughly 70% of digital advertising, but as mentioned above, this can expand on the back of the smaller advertising players who don’t have the capex and the tech stack to challenge the big 3.

Finally, the Antitrust case is not yet resolved. We are currently in the "remedy phase," where the court is deciding if Google must spin off Chrome or the Ad stack.

Conclusion

In terms of top-line growth, there will be around 10-15% growth per year, mostly due to maturing ad revenue growth, but boosted by the cloud growth.

In total, with the top line growth and margin expansion, we will see CAGR in EPS of around 20%-25% per year, which is not enough for the current valuation of slightly over 30x PE.

The main question is whether GOOGL can reach $400 per share – perhaps yes, the path seems quite clear without many risks. This is 16% upside from the current price, which is decent but not so big. Most of the gains here have already been made.

Recommended Articles