What Investors Should Watch Behind Nike’s Stock Price Plunge?

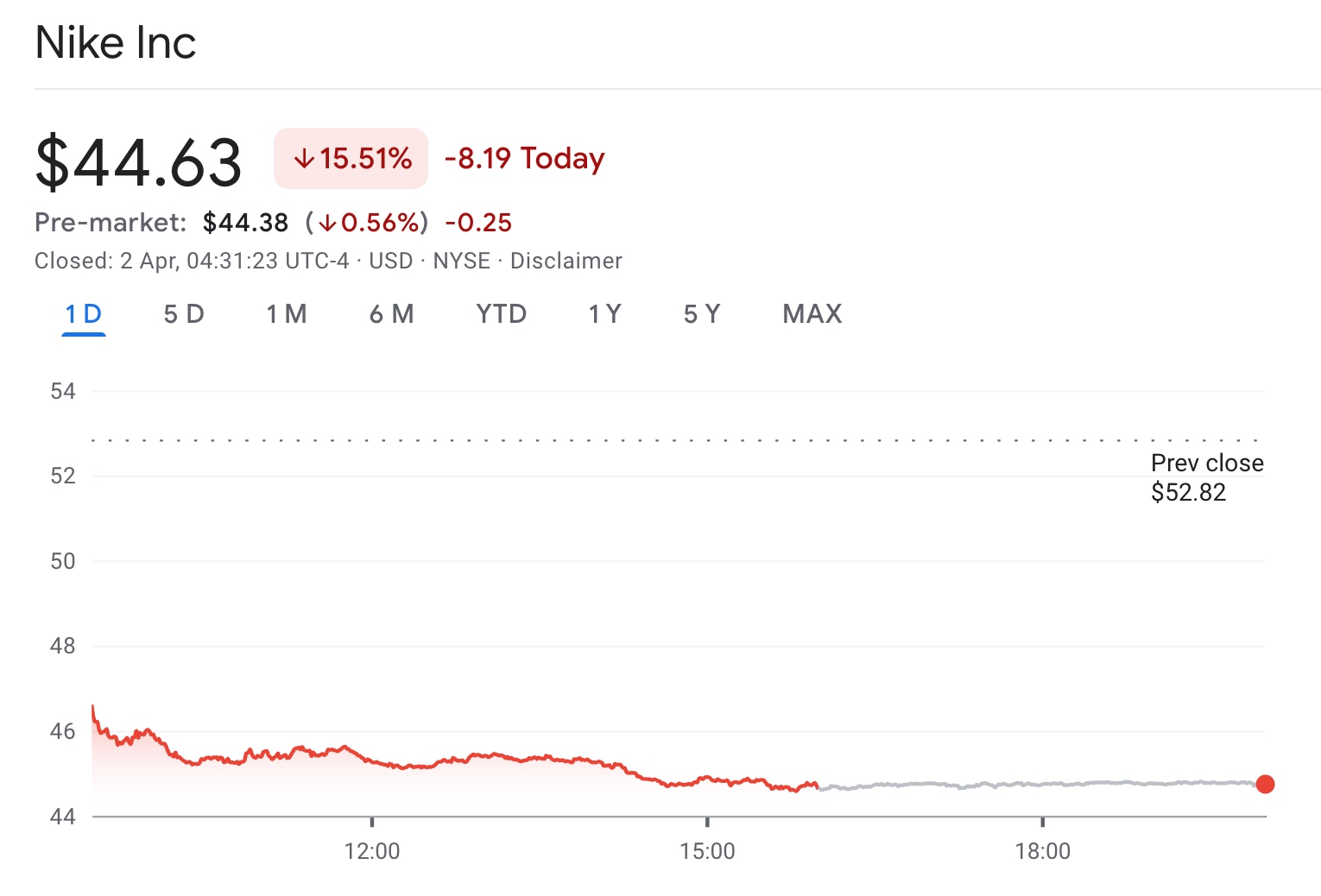

TradingKey - Nike (NKE.US) Nike's stock price suffered a heavy blow on Wednesday Eastern Time, plunging 15.51% to close at $44.63. This marked its worst single-day performance since June 2024 and weighed down the Dow Jones Industrial Average, bringing its cumulative decline in 2026 to nearly 30%.

[NKE stock price trend, Source: Google Finance]

Although the company's fiscal third-quarter earnings exceeded expectations, the results were overshadowed by weak guidance and a warning of a 20% drop in sales in Greater China.

In addition, the conflict in the Middle East has caused disruptions to its business in Europe, the Middle East, and Africa (EMEA). CFO Matthew Friend noted that the war is impacting consumer behavior and leading to rising inventory levels.

Affected by global supply chain instability triggered by the conflict in the Middle East, manufacturers like Nike and Adidas that rely on Southeast Asian manufacturing hubs are facing additional pressure from U.S. tariffs on imports from countries such as Vietnam.

Analysts warn that under the dual pressure of inflationary strain and geopolitical risk, Nike's stock performance for the remainder of 2026 will continue to struggle unless it can accelerate product innovation and effectively integrate its supply chain.

Why has Nike's stock price been on a steady decline?

Nike continues to be impacted by multiple factors. The 2025 Trump tariffs and the escalation of geopolitical conflicts in 2026 have rendered Nike's already-strained moat even more fragile.

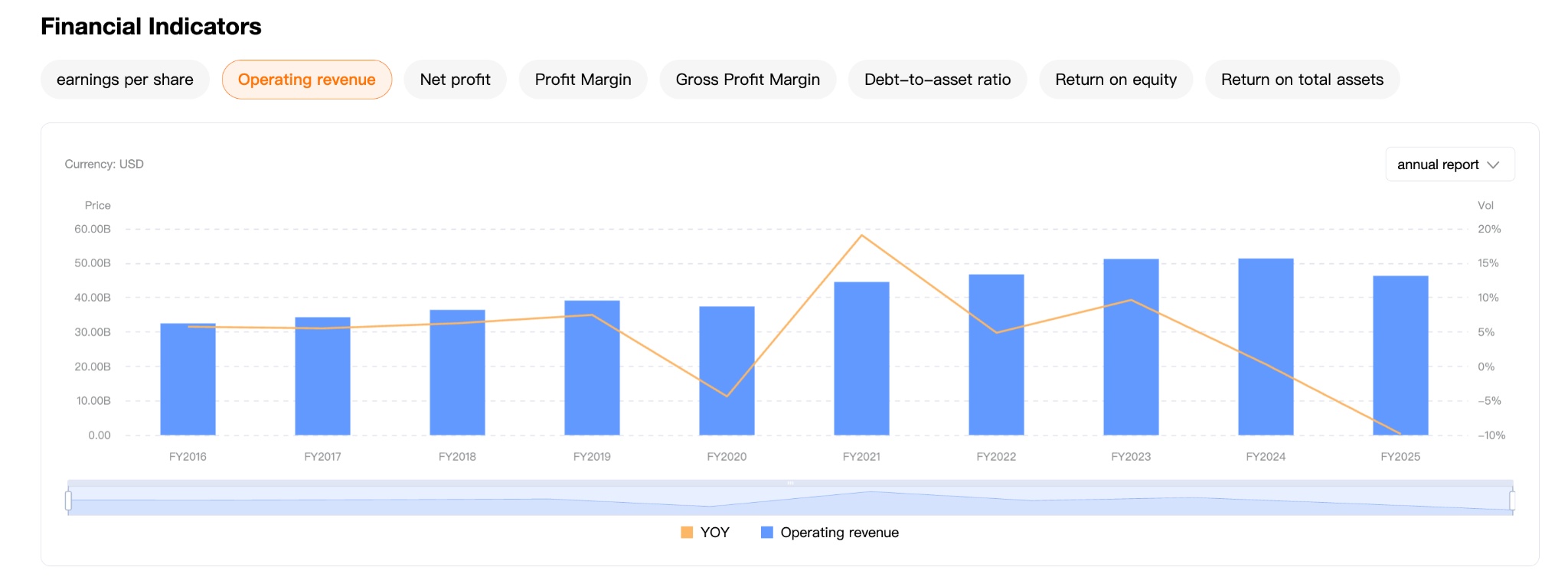

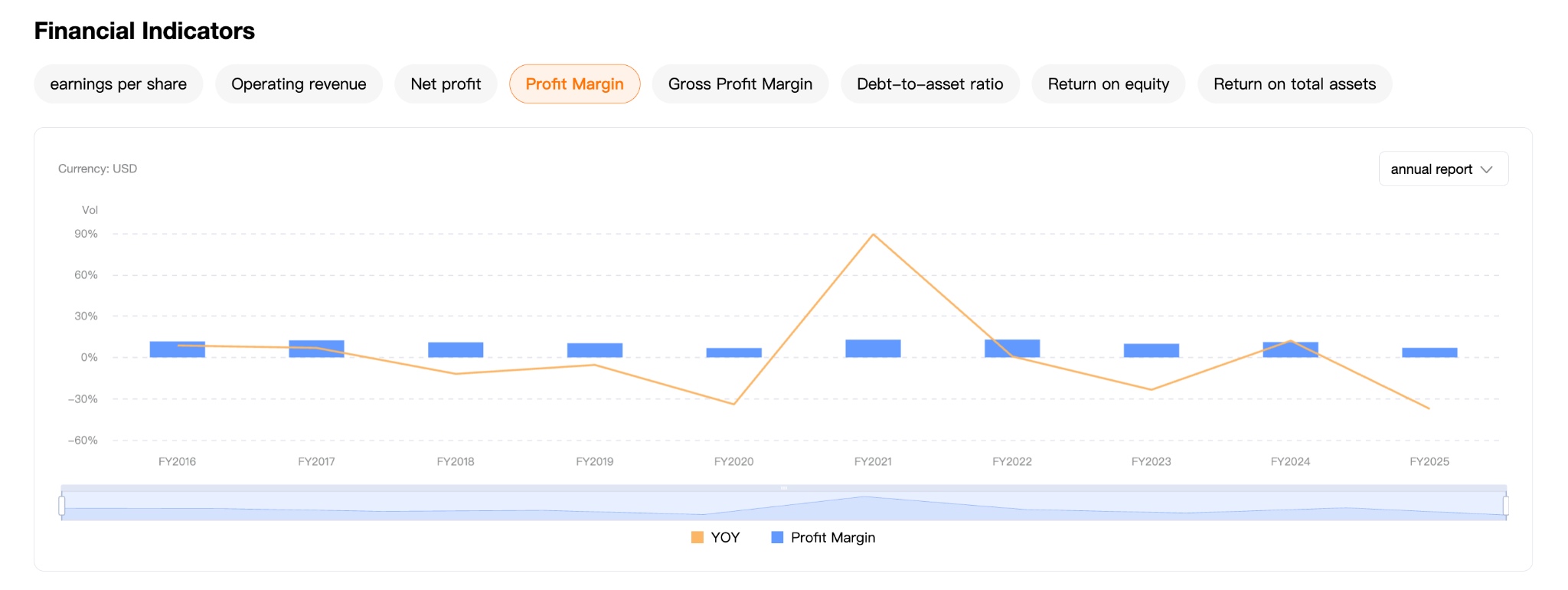

Nike reached its peak between 2021 and 2022. According to its financial reports, its net profit margin increased by 125% year-over-year in 2021, primarily due to the sharp rise in demand for home fitness during the pandemic and a significant increase in the share of online shopping, along with reduced store operating costs.

Since then, although net profit continued to grow in 2022, its growth rate slowed significantly year-over-year. Starting in 2023, the phenomenon of 'revenue growth without profit growth' emerged, and the stock price has been on a downward trend.

Fiscal Year | Greater China Revenue | Total Global Revenue | Greater China Share | YoY Change |

2021 | $8.290 billion | $44.54 billion | 18.6% | +24% |

2022 | $7.547 billion | $46.71 billion | 16.2% | -9% |

2023 | $7.248 billion | $51.22 billion | 14.1% | -4% |

2024 | $7.545 billion | $51.36 billion | 14.7% | +4% |

2025 | $6.586 billion | $46.30 billion | 14.2% | -13% |

[Nike Sales Data 2021-2025, Source: NKE Official Financial Reports]

In addition, market share in Greater China has been squeezed by local brands; against a backdrop of intensifying competition, its revenue contribution fell from 18.6% in 2021 to 14.2% in 2025.

Meanwhile, despite Nike's active pursuit of transformation in Greater China, the implementation of its new strategy still faces challenges. Nike CEO Elliott Hill admitted in an earnings call that the business turnaround is taking longer than expected.

Currently, Nike remains mired in the predicament of weak digital business, inventory backlog, and fierce competition from Chinese local brands like Anta and Li-Ning, which has resulted in the persistent underperformance of Nike's stock price.

What should Nike investors focus on?

Currently, investors need to focus on three key variables: demand structure and regional recovery capabilities, the rebalancing of supply chains and cost structures, and the actual returns on digital transformation.

First is demand structure and regional recovery capabilities. Greater China was once Nike's most profit-elastic market, but its share of revenue has continued to decline in recent years; coupled with the rise of local brands, its "brand premium" is being eroded. In the short term, the pace of inventory destocking and terminal discount intensity must be observed; in the long term, it depends on whether Nike's innovation capabilities can re-drive demand.

Second is the rebalancing of supply chains and cost structures. Under the disruption of tariff policies and geopolitical shifts, Nike's model of heavy reliance on Southeast Asian manufacturing faces challenges. If it cannot effectively redeploy production capacity and optimize its logistics system, its gross margins will continue to face pressure.

In other words, future profit elasticity will no longer depend solely on sales growth, but more on cost control and supply chain resilience.

In addition, Nike previously pushed its DTC (Direct-to-Consumer) strategy aggressively to enhance profit margins. However, slowing growth in online channels and rising customer acquisition costs have led to diminishing marginal returns for this strategy. The market will re-evaluate the ROI of its e-commerce and membership systems; if it fails to generate scalable compounding benefits, its valuation premium may further contract.

In summary, Nike's current trading logic has fully shifted to "turnaround pricing." Judging by its stock price, the valuation premium brought by the brand has almost entirely vanished; investors need to determine whether it still possesses the ability to return to structural growth, rather than just stabilizing short-term performance.

Recommended Articles