Why Micron’s New NAND Factory Feels Like a Sweet Treat to Investors

TradingKey - Micron (MU) shares jumped 12% this week to $435.28, extending a six‑month rally of nearly 270%.

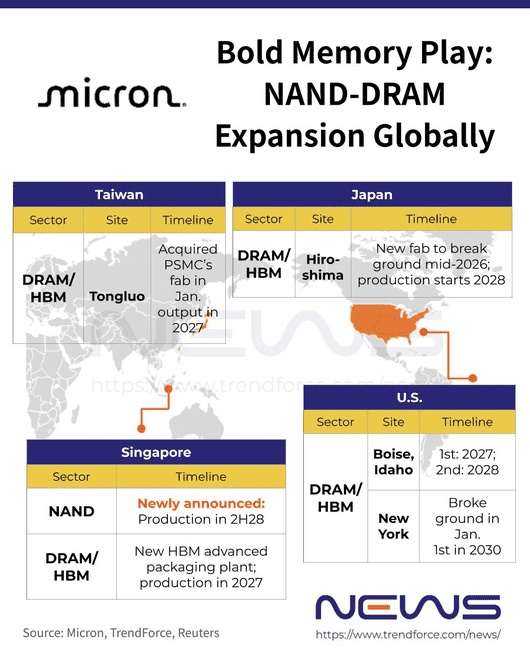

The catalyst came late Monday, when the company announced a $24 billion investment to build a new advanced fab at its Singapore campus focused on NAND flash manufacturing. The move pleased both camps of investors—those seeking long‑term growth visibility and those focusing on near‑term profitability. It landed, as many put it, right on the “sweet spot.”

Together with the ongoing $7 billion HBM packaging plant in Singapore (expected to contribute significant capacity from 2027), Micron will create an integrated “NAND + HBM Packaging + R&D” base, greatly enhancing its stickiness with AI‑server and data‑center customers.

Reason 1: Reinforcing the Structural Demand Story

Micron’s message was clear: structural demand is real—and enduring.The rise of Agentic AI, defined by autonomy and memory, is fueling continuous storage needs. Intelligent agents must preserve historical conversations, task states, file iterations, and multimodal data externally to function and evolve.Several trend reports predict that by 2026, enterprise applications will embed agents en masse into workflows, forming distributed, multi‑agent systems that constantly write, append, and record. Such architectures are natural consumers of massive, persistent storage.

The company’s existing production capacity—especially in HBM, DRAM, and NAND for AI—is already running at full utilization. In earlier earnings calls, management admitted it could satisfy only 50% to two‑thirds of key customer demand, calling it “the most severe supply‑demand imbalance” in its 25‑year corporate history.

To address the shortage, Micron has repeatedly announced capacity expansions. On January 18, the company confirmed plans to acquire TSMC (TSM)’s Taichung (Tongluo) fab for $1.8 billion (excluding equipment). According to TrendForce, Micron will begin staged deployments between 2026 and 2027, focusing on front‑end systems for advanced DRAM, with full production expected in 2027. At the same time, it is constructing a $7 billion advanced HBM packaging facility scheduled for mass output in 2027. The newly announced Singapore fab will primarily focus on NAND flash, adding another strategic pillar.

Once operational, the new plant will nearly double Micron’s current NAND capacity. As a rule of thumb, roughly $15 billion in CapEx equates to 100 k wafers per month (wpm). Using that metric, the $24 billion investment would provide approximately 150 k – 200 k wpm of new NAND capacity.That projection strengthens the view that NAND demand will continue rising through the decade. A commitment of this scale signals that Micron is planning for the next ten years, not just the next few quarters—underlining management’s conviction in structural growth.

Reason 2: Protecting Short‑Term Pricing Power

In modern data centers, NAND flash has become integral to AI inference—the process of running trained models. Its non‑volatile nature, meaning it retains data even when power is off, makes it vital for servers, drives, and everyday devices alike.

Memory suppliers historically hesitate to add production because cyclical oversupply devastates pricing. Once the market senses that risk, share prices often fall pre‑emptively, triggering the familiar “valuation and earnings double compression.” The industry then enters a clearing stage—shutting lines, lowering utilization, and depreciating assets—until equilibrium returns.

The previous memory cycle illustrated this pitfall perfectly: at peak prices and strongest sentiment, producers over‑expanded, and one to two years later, as demand softened, the glut erupted, forcing an entire round of painful capacity cuts.

Micron is determined not to repeat that mistake. By delaying volume production at its Singapore facility until after 2028, the company helps ensure that the current tight‑supply condition persists. In the short term, NAND prices and industry sentiment are unlikely to weaken because of the expansion. Management emphasized that ramp‑up schedules will remain flexible and “market‑responsive,” leaving room for demand evolution and natural digestion of existing inventory.

Strategic Intention: Anchoring Next‑Gen Technology Leadership

Industry research from Global Semi Research shows that Micron also intends to develop High‑Bandwidth Flash (HBF) and other advanced NAND technologies at the new Singapore site. Such components align directly with NVIDIA (NVDA)’s roadmap and reflect a strategic shift in AI infrastructure design.

NVIDIA plans to incorporate HBF into its Integrated Compute‑Memory‑Storage (ICMS) framework because current enterprise SSDs cannot meet the bandwidth demands of next‑generation AI computation. As model sizes and inference workloads multiply, storage I/O has become the new bottleneck.

NVIDIA is collaborating with Western Digital (WDC) to co‑develop HBF chips—evidence that it seeks multiple supply sources. Micron’s $24 billion commitment signals that it too is positioning itself as a critical supplier in this emerging, strategically important segment.

Why the Market Rewards the Story

From a valuation perspective, the expansion delivers what investors love most: a coherent long‑term growth narrative.

Valuation can be simplified as expected earnings × the multiple investors are willing to pay. Micron’s successive capacity announcements send several reinforced messages: demand is durable and multi‑year. The company has already secured or is finalizing long‑duration contracts with strong commitment clauses. News such as its fully booked 2026 HBM capacity tells investors that future revenue visibility is high.

More importantly, most spending targets high‑margin areas—HBM, advanced DRAM, and AI‑optimized NAND—rather than low‑end, low‑margin categories. As scale rises, profit quality improves.

When markets conclude that a the memory sector’s growth is structural, driven by long‑term AI demand, and (b) Micron has effectively locked in that demand via expansion and contracts, they reprice the stock as a growth business, not a cyclical one.

Cyclical companies trade at low multiples because earnings swing widely and durability is uncertain. Growth companies warrant higher valuations because earnings are sustainable and have a visible trajectory.

Micron’s clear expansion roadmap and secured HBM orders demonstrate to the market that this isn’t just a one‑off windfall—it’s the groundwork for harvesting the AI storage dividend for years to come. Analysts have begun placing Micron within the “AI infrastructure core supplier” category, lifting both price targets and valuation multiples accordingly.

Recommended Articles