TradingKey Previous Week’s Market Review & Analysis

TradingKey - Macroeconomic Landscape: The first full trading week of 2026 was largely shaped by crucial labor market data. The December 2025 Employment Situation Report, released on January 9, 2026, indicated that U.S. employers added a modest 50,000 jobs in December, with the unemployment rate falling to 4.4%. This marked a significant deceleration in annual job growth for 2025, with an average of 49,000 jobs per month, compared to 168,000 per month in 2024. Wage growth remained strong, up 4.1 percent in the last three months, while inflation reportedly hit its lowest level in nearly five years. The Services Purchasing Managers' Index for December also showed continued expansion but at a decelerated pace, falling to 52.5 from November’s 54.1. Geopolitical developments saw crude oil prices tick higher and gold prices advance following a U.S. intervention in Venezuela on January 5, 2026. Ten-year Treasury yields edged slightly higher, reflecting ongoing fiscal and inflation concerns.

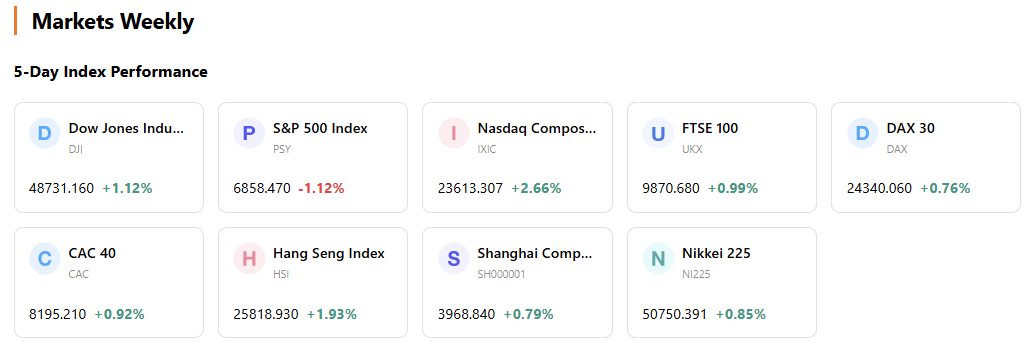

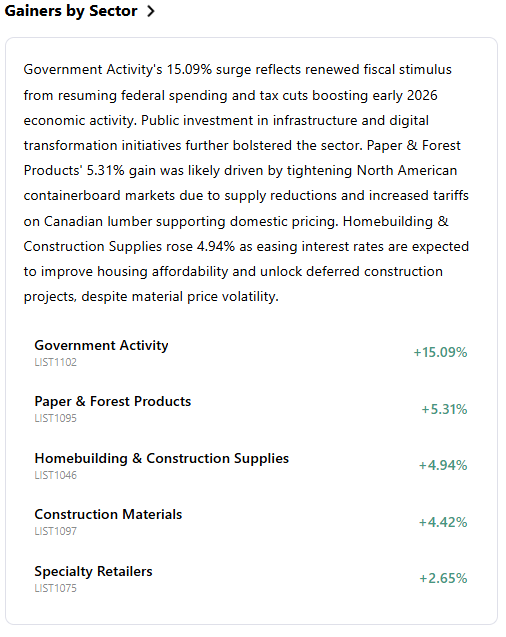

Market Performance Overview: U.S. equity markets posted solid gains, recovering from declines in the final week of 2025. The Dow Jones Industrial Average, Nasdaq, and S&P 500 closed the week up 2.3%, 1.9%, and 1.6% respectively. The Dow Jones Industrial Average surged past 49,000, and the S&P 500 also hit a new record high. Small-cap stocks, represented by the Russell 2000 Index, surged 4.6%, indicating an expanding market breadth. Energy, utilities, industrials, and materials sectors moved higher.

Key Events Analysis: The December 2025 jobs report was a primary driver for the week, with the declining unemployment rate and moderated job growth supporting investor optimism around potential Federal Reserve rate cuts later in the year, despite inflation remaining above target. However, the release of the December 2025 FOMC meeting minutes on December 30, 2025, highlighted a lack of unanimity among committee members on future rate decisions, with some favoring maintaining current rates for an extended period. The Consumer Price Index for December 2025 is scheduled for release on Tuesday, January 13, 2026, outside this reporting period.

Flows & Sentiment: Global risk assets rallied, driven by a surge in investor sentiment and aggressive exits from defensive assets. The CBOE Volatility Index (VIX) decreased to 14.51 on January 5, 2026, reflecting a relatively calm environment. U.S. equity funds saw $15.5 billion in net inflows for the week ending December 31, 2025, with large-cap funds attracting $37.2 billion in a subsequent week, indicating shifting risk appetite. However, long-term mutual funds recorded estimated outflows of $4.90 billion for the week ended December 30, 2025.

Overall Assessment: The market started 2026 with strong bullish momentum, propelled by positive investor sentiment and a jobs report signaling a potentially more accommodative Fed stance later in the year. The rally was broad-based, with small-caps showing notable strength. However, underlying caution remains regarding inflation and the path of future rate cuts.

Next Week’s key market drivers & Investment Outlook

Upcoming Events: The release of the December 2025 Consumer Price Index on Tuesday, January 13, 2026, will be a critical data point, influencing inflation expectations and the Fed's monetary policy outlook. Additionally, the earnings season will begin to pick up, with a few companies scheduled to report.

Market Logic Projection: The market will likely remain highly sensitive to inflation data, as any surprises could re-evaluate the timing and extent of anticipated rate cuts. Continued moderation in economic data, balanced with signs of sustained growth, would support the current bullish sentiment.

Strategy & Allocation Recommendations: Investors should maintain a diversified portfolio while selectively increasing exposure to cyclical sectors that stand to benefit from an improving economic backdrop and potential Fed easing. Given the strong start for small-caps, tactical allocations to this segment could be considered. Overweight industrials and energy due to geopolitical factors and infrastructure spending.

Risk Alerts: Key risks include potential upside surprises in inflation data, which could lead to a hawkish repricing of Fed expectations. Geopolitical tensions, particularly regarding energy supplies, could also introduce volatility. The strong market rally at the start of the year warrants vigilance for potential profit-taking.

Recommended Articles