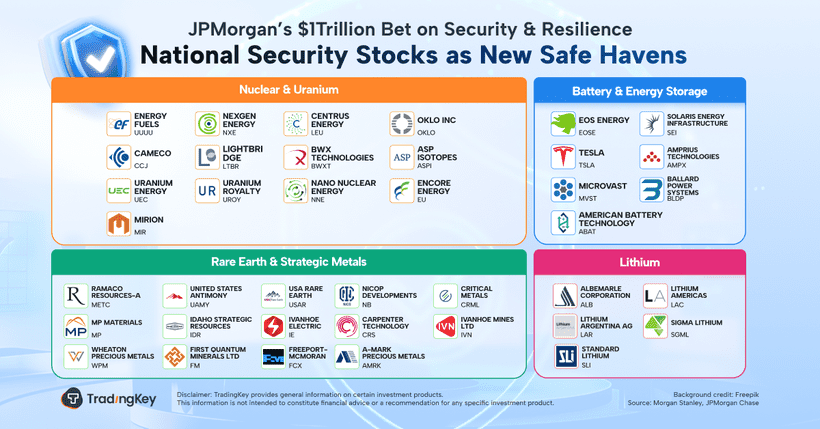

JPMorgan’s $1Trillion Bet on Security & Resilience: National Security Stocks as New Safe Havens

TradingKey - On Monday, JPMorgan announced a sweeping 10-year strategic investment plan under the theme of “Security & Resilience”—an initiative that could involve up to $1 trillion in capital deployment across four high-priority sectors.

The four main areas include: 1) Defense and aerospace; 2) Frontier technologies like AI and quantum computing; 3) Clean energy innovation; 4) Supply chain and advanced manufacturing.

Importantly, this isn’t just about traditional loans and direct investments. JPMorgan intends to leverage its full financial toolkit—including equity and bond underwriting, capital matchmaking, and third-party syndication—to pull in external investors and amplify the program’s impact. According to internal estimates, this could unlock an additional 500 billion in new financing beyond baseline expectations bringing total market impact to as much as $1.5 trillion.

Investors noticed. As the news broke, market focus around “national security–linked” assets surged.

Tensions Rise: Rare Earths Back at the Center of U.S.–China Frictions

In the backdrop, U.S.–China competition over critical materials and technology has intensified again—this time with rare earths back in the spotlight.

Last Thursday, China’s Ministry of Commerce announced that starting December 1st, all exports containing more than 0.1% Chinese-sourced rare earth material—or derived from extraction, processing, or magnet-making technologies developed in China—will require export permits. The message is clear: supply is tightening.

Given China supplies around 70% of global rare earth minerals, the new rule has sent shockwaves through global supply chains—especially in defense, EV batteries, and high-end semiconductors, where these materials are essential.

The U.S. government was quick to react. President Donald Trump announced a new round of tariffs targeting Chinese imports and formally unveiled a $1 billion “Strategic Critical Minerals Reserve” plan. Rare earths were explicitly labeled a national security priority, causing related stocks to spike.

This isn’t a new development—it’s the continuation of a trend. Since 2025, the U.S. has been accelerating its buildout of rare earth capacity, both domestically and through friendly partner countries.

The Department of Defense (DoD), U.S. Export-Import Bank (EXIM), and other agencies have been deploying direct investments, equity stakes, and warrant-based incentives to expand rare earth development in places like Australia, Canada, and Greenland.

Just in October, two major project financings were advanced: the first one is EXIM plans to back Critical Metals’ Tanbreez project in Greenland, targeting 85,000 tons/year of rare earth concentrate output by 2026. Another one is the U.S. also provided warrant support for Canada’s Thacker Pass project, which includes rare earth byproducts and further signals growing focus on the full resource lifecycle—including recycling and reuse.

Domestically, support is ramping up too. In July, the DoD committed 400 million to MP Materials to build a rare earth magnet manufacturing facility, aiming to form a fully domestic, end-to-end rare earth supply chain: from raw ore to finished magnets. MP has already invested over 1 billion into its Mountain Pass site in California, creating one of the few vertically integrated rare earth ecosystems globally.

Another key player is USA Rare Earth (USAR). The company is looking to replicate MP’s closed-loop model, adding integrated mine–process–manufacture–recycle capacity. The firm is also aggressively pursuing long-term government procurement contracts and funding support to improve its odds in a highly strategic and increasingly politicized—industry.

Quantum Computing: Speculative Fringe or Next Strategic Frontier?

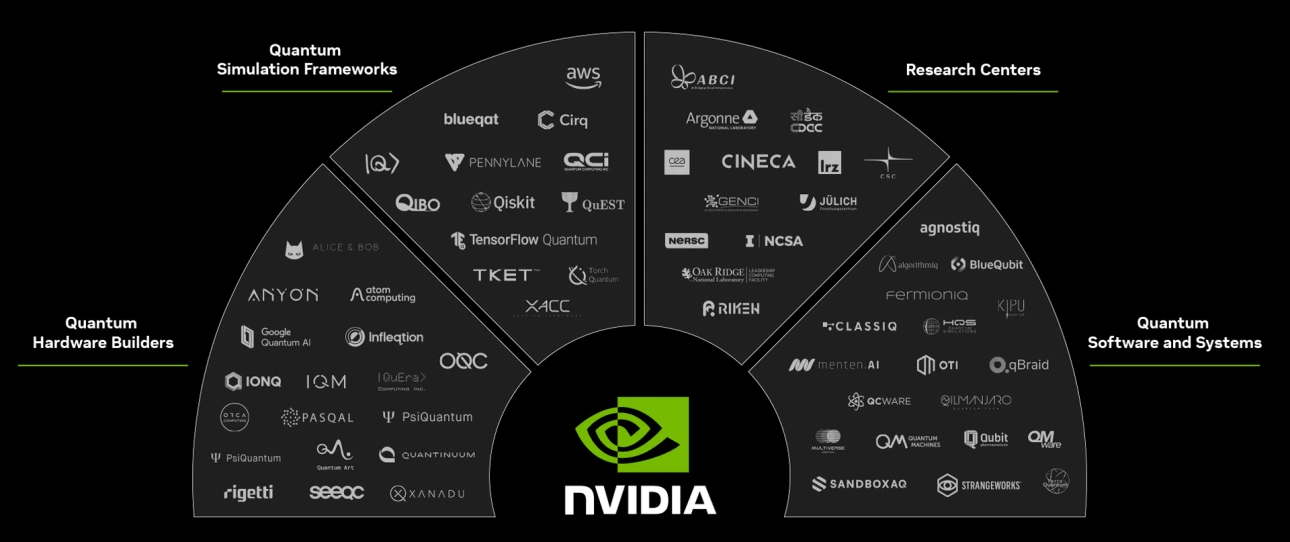

It’s not just rocks and magnets. JPMorgan’s framework for “Security & Resilience” explicitly includes quantum computing as one of 27 designated deep-tech priorities—and investors are paying attention.

Recent weeks have seen dramatic share price surges for listed quantum players. Rigetti and D-Wave are both up more than 100% month-to-date.

D-Wave’s quantum annealing machines are already being used in early enterprise pilots across finance, logistics, and precision manufacturing. The company saw revenue grow more than 500% YoY in Q1 2025—suggesting that monetization is finally starting to catch up with theory.

Meanwhile, on the enterprise side, Amazon is pushing hard into quantum services through its Braket platform, offering processing access via Rigetti and IONQ chips. This infrastructure-first approach gives AWS a clear early-mover advantage in enabling real-world quantum compute access.

At the bleeding edge, companies like Google continue to support longer-term research—and the results are showing. A Google-backed research team was recently awarded a Nobel Prize for work in quantum information science, reinforcing the value of long-horizon R&D bets.

For now, quantum-classical hybrid architectures seem to have the most commercial promise. By combining quantum processing units (QPUs) with GPU clusters, companies can tackle problems like climate modeling, financial risk simulation, and molecular analysis—scenarios where classical compute hits its limits.

NVIDIA’s CUDA-Q platform and IBM’s open-source Qiskit runtime are already core infrastructure within this hybrid model. NVIDIA has quietly built partnerships and investments across multiple quantum hardware verticals—ion trap players like Quantinuum, neutral atom firms like QuEra, superconducting startups like Anyon, and simulation specialists like Fermioniq—all part of its bid to build a QPU-friendly ecosystem anchored on GPUs.

AI Spending: Still Going Strong

If there’s one theme that's still clearly immune to valuation fatigue, it’s AI.

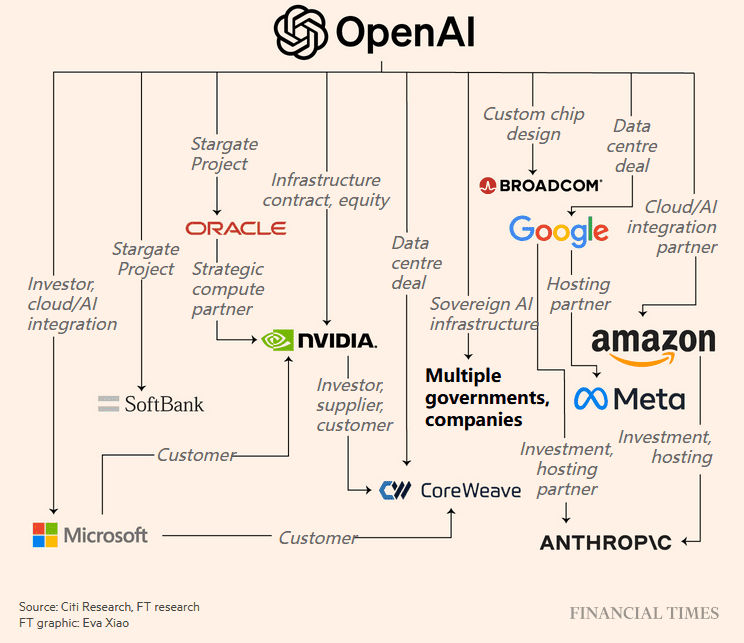

Sam Altman, OpenAI CEO, recently disclosed that the company has signed compute procurement agreements totaling at least 26GW with a handful of partners—including Oracle, NVIDIA, AMD, and Broadcom. That’s up-sized ambition any way you slice it.

According to estimates from the Financial Times, improvements in AI hardware and efficiency could save the industry over $1 trillion in infrastructure costs over the next decade. Meaning, even now—at scale—a lot of spend still makes economic sense.

Investors seem to agree. Each of these partner companies saw share prices jump on the news, suggesting the market still has plenty of appetite for the “AI economies-of-scale” narrative.

JPMorgan seems to agree too. AI sits prominently in its “Security & Resilience” map. But what’s changed is the nature of the investment: we’re now seeing the shift from discrete compute contracts to long-term ecosystem buildouts. The emphasis now appears to be on combining three factors—efficiency, cost, and vertical integration—into what can only be described as a coordinated AI industrial policy.

We may still be early. Jamie Dimon, in a recent BBC interview, compared the AI investment wave to the early years of television and automobiles—industries that eventually created trillions in value, but where many early players failed to capture it. In his words: “most people involved in it didn’t do well.”

The stakes are high, the optimism is real—but so is the risk.

Recommended Articles