Synopsys (SNPS): Strategic Opportunities and Risks Amid 40% Drawdown

Source: TradingView

Hook

Chip giant Synopsys teetering on the edge? The ultimate "pick-and-shovel" supplier in the AI frenzy, but hammered by China's sudden market freeze and export clamps, sending shares crashing 40%! Is that $35 billion Ansys mega-deal a rescue rope or a bigger sinkhole? Dive into the EDA powerhouse's nail-biting reversal and hidden investment gems! Worth jumping in now?

Summary

· Synopsys leads globally in electronic design automation (EDA) and semiconductor intellectual property (IP), partnering with Cadence to dominate the industry. By late 2024, Synopsys has about 31% of the EDA market. Its tools are important for creating advanced semiconductor chips.

· The company’s recent fundamentals have faced significant challenges. Due to U.S. export controls on China and slowing demand in the Chinese market, Synopsys lowered key financial guidance in Q2. This exposed its business vulnerability to geopolitical risks and specific markets. The market’s expectation of sustained high growth was disrupted. The stock price fell over 40% from its July peak.

· The $35 billion acquisition of Ansys gains strategic importance. It is not just business expansion. It is a critical step to find new growth avenues and reduce risk dependency amid challenges in core business.

· Although the company has grown strongly in the past, the recent guidance downward suggests less predictivity for its performance over the next one to two years. The company’s growth story has increased some uncertainties from previous consistent high growth.

Investment Thesis

Synopsys drives innovation in the semiconductor industry. It supplies key EDA (electronic design automation) software tools and IP modules for complex chip design. We are optimistic about its long-term investment value for these reasons:

· Irreplaceable industry position: EDA is the foundation of chip design. It has high technical barriers and loyal customers. As a top global player, Synopsys works closely with leading semiconductor firms. Switching to competitors is costly for clients. This helps it to build a strong competitive edge.

· Key player in the AI boom: AI chips are increasingly complex. Demand for EDA tools is increasing a lot. Synopsys’ products are key for NVIDIA’s GPUs and cloud companies’ custom AI chips. It serves as an important supplier in the AI growth surge.

· Ansys acquisition is a new growth story: Acquiring Ansys helps to expand Synopsys into system-level design and simulation. It strengthens product portfolio value for current clients. In addition, it also opens cross-selling opportunities in automotive and aerospace sectors.

· Solid business model: The revenue source is very stable, with over 85% of revenue coming from subscriptions and maintenance services. With a light-asset business model, Synopsys could maintain around 80% gross margins. Also, cash flow is strong and stable, supporting R&D and acquisitions.

However, recent issues call for a cautious investment views:

· Growth certainty is not certain: Performance guidance cuts due to China market issues, indicating sensitivity to macroeconomic and geopolitical factors. Short-term performance predictability has declined.

· Customer budgets is tightening: Synopsys’ role of providing "pick-and-shovel" is clear in AI trend. However, some clients, especially in China, are cutting their budgets because of external pressures. This would result in cautious spending on EDA tools, impacting orders and revenue.

· Ansys acquisition is risky: Acquiring Ansys is a key move for expansion and risk mitigation, especially when the current core business is under pressure. However, the financial burden and integration uncertainties of this acquisition cannot be ignored.

· Valuation must rely on fundamentals: The stock has rebounded sharply from its lows because of market enthusiasm for AI instead of full recovery in fundamentals. The current valuation premium carries some risk until the company’s fundamentals stabilize.

Industry Overview

Industry Role

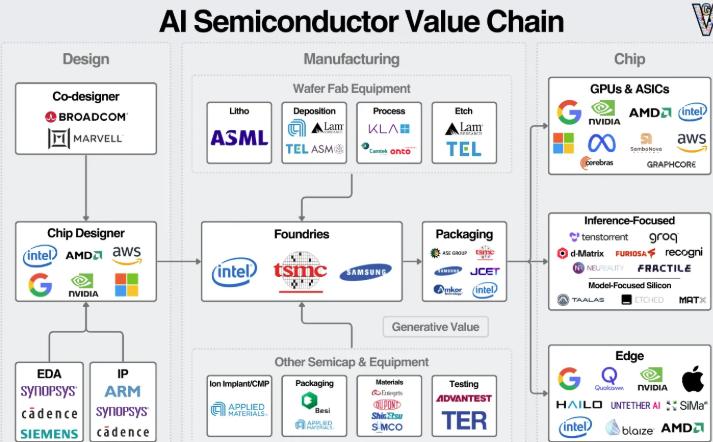

In simple terms, the chip manufacturing process begins with the design. EDA companies like Synopsys provide platforms to chip design manufacturers such as Intel, AMD, and NVIDIA. After the chip design is completed, manufacturing equipment enterprises like ASML support wafer fabrication plants such as Intel and TSMC in chip production by providing lithography machines. Then, Samsung and Intel carry out packaging and testing. Finally, NVIDIA, Google, and others integrate the chips into AI applications such as GPU/ASIC or edge computing, completing the entire value chain from design to application.

Synopsys is at the very top of the semiconductor supply chain. It doesn't make chips by itself, but it supplies EDA software and IP modules to global chip designers (like NVIDIA, Apple, AMD, and Intel). In terms of the function, EDA tools can help engineers efficiently handle the full process of chip design from idea to production, this could help to decrease errors, shorten the design timelines, and saving cost. They're essential for today's complex chip designs. On the other hand, Synopsys’s IP business provides pre-designed and pre-verified circuit blocks for chip companies, and they can license and plug right in. This shortens development time, reduces technical risks and costs, and gets products to market faster.

Source: generative value

Competitive Landscape

The EDA industry is a classic oligopoly, controlled by three big players: Synopsys, Cadence Design Systems, and Siemens EDA (formerly Mentor Graphics). Data from TrendForce shows that in 2024, Synopsys and Cadence held about 31% and 30% market share respectively, giving them clear dominance together.

Market Potential

According to Stellar Market Research, the global EDA software market hit $13.26 billion in 2024 and is projected to reach $26.62 billion by 2032, with a compound annual growth rate (CAGR) of 9.1%. Under the trends in AI, data centers, smart cars, and IoT, the CAGR could climb to 12-15% over the next decade. The followings are the details:

· AI and Data Centers: The complexity of AI chips keeps increasing. The demand for designs of advanced nodes like 3nm or 2nm drives rapid growth in EDA tools.

· Automotive Intelligence and Electrification: The number of semiconductor chips in each vehicle has increased from several hundred to 1,000 to 3,500, and the demand for EDA tools in the design of automotive-grade chips has risen significantly.

· IoT and Industrial Applications: The demand for diversified and low-power chip designs continues to expand, providing new growth momentum to the EDA market.

Competitive Advantages

Leading Technology and R&D Investment: As chip manufacturing processes is in the era of the nanometer scale (such as 3nm, 2nm), the complexity has grown a lot. Synopsys invests a large amount of R&D expenses each year (typically more than 30% of its revenue) to maintain its technological lead. Such R&D investment is hard for new entrants to catch up.

High Switching Costs for Customers: The process of designing chips is very complex. Engineers need to spend years learning and getting used to a set of EDA toolchains. Once a company selects Synopsys' platform, its design process, project data, and talent skills will be deeply integrated with this platform. Switching suppliers means huge risks of time, money, and project failure. Therefore, Synopsys' customer retention rate is close to 100%.

Strong Ecosystem: Synopsys has partnered with top foundries (like TSMC, Samsung, and Intel). This kind of partnership helps to ensure its EDA tools are compatible with the latest manufacturing processes. This provides clients with a seamless transition from design to mass production.

AI-Powered Next-Gen EDA: Synopsys first used AI in EDA tools (such as DSO.ai™). Now it could automatically optimize the power consumption, performance and area (PPA) of chips because of using machine learning. This boosts efficiency and raises new tech barriers.

Business Model

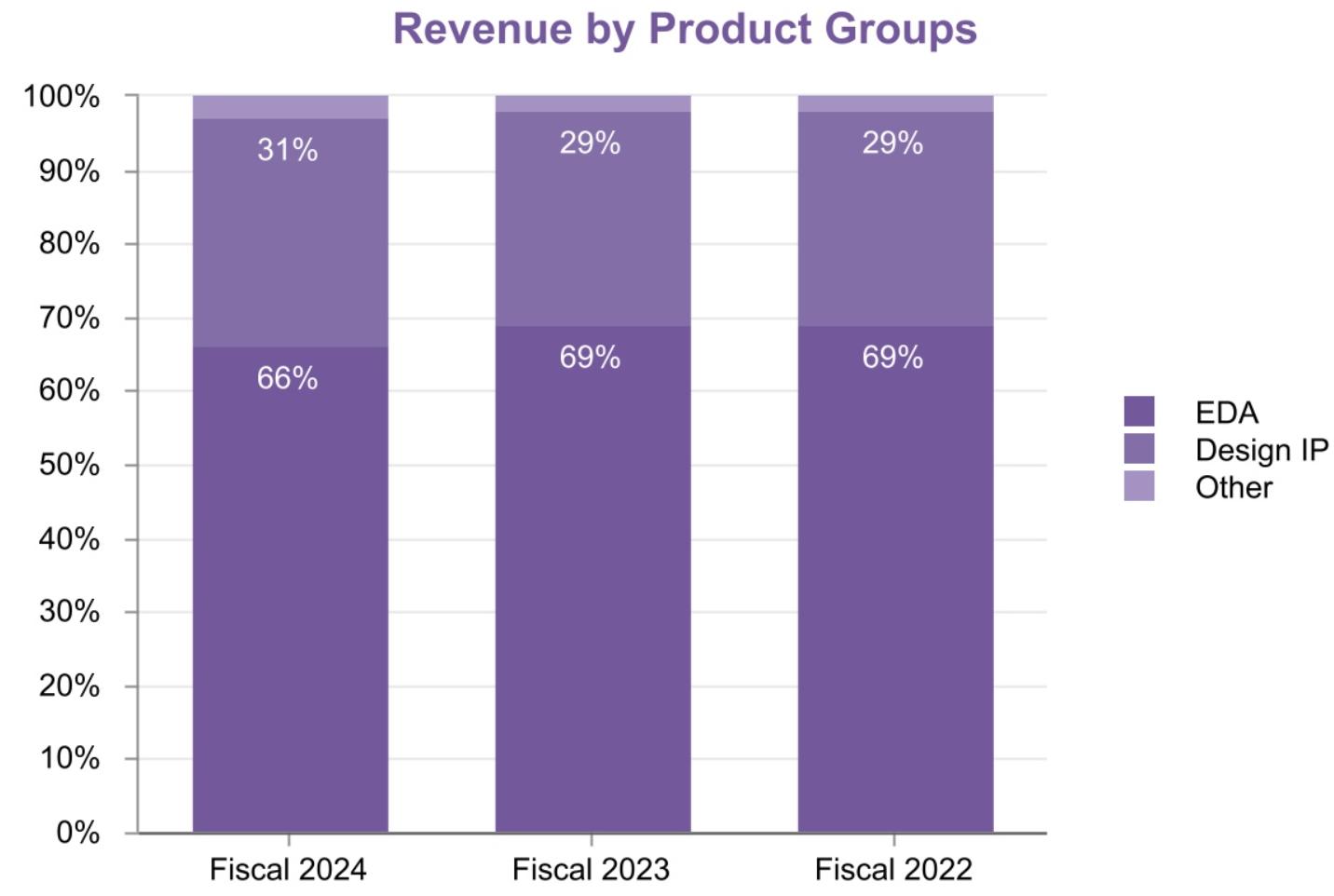

Synopsys' revenue has two main parts: 1) Design Automation (EDA): This is the core business, including software licenses and maintenance, accounting for around two-thirds of total revenue. It's important for chip design efficiency and quality. 2) IP Licensing: one-third of Synopsys' total revenue, including around 60% of the upfront licensing fees and around 40% of the royalty income. Royalties are the fees generated when clients want to produce or sell chips with Synopsys IP. They usually pay these fees on a per-unit basis or based on sales volume. In addition, Synopsys has the most comprehensive IP portfolio in the industry, which is used in high-value chip designs. Synopsys keeps leading in the licensing market. However, due to the smaller shipment volume, it lags behind Arm in the royalty market, which is dominated by the consumer electronics sector, because its IP shipment volume is larger.

Most of the revenue comes from time-based licensing (subscriptions), usually for a period of 2-3 years, ensuring highly predictable and stable recurring income. Moreover, this model has a typical "upfront payment" nature, as clients usually pay for years of licensing fees in advance, which enables the company to have a very strong operating cash flow, often higher than its accounting profit. Plus, the customer base is diverse, from tech giants like NVIDIA and Apple to up-and-coming AI chip startups. Lately, as carmakers and consumer electronics firms ramp up their own chip designs, the client pool has grown even more.

Source: SEC, Company Report

Why Did the Stock Price Plunge?

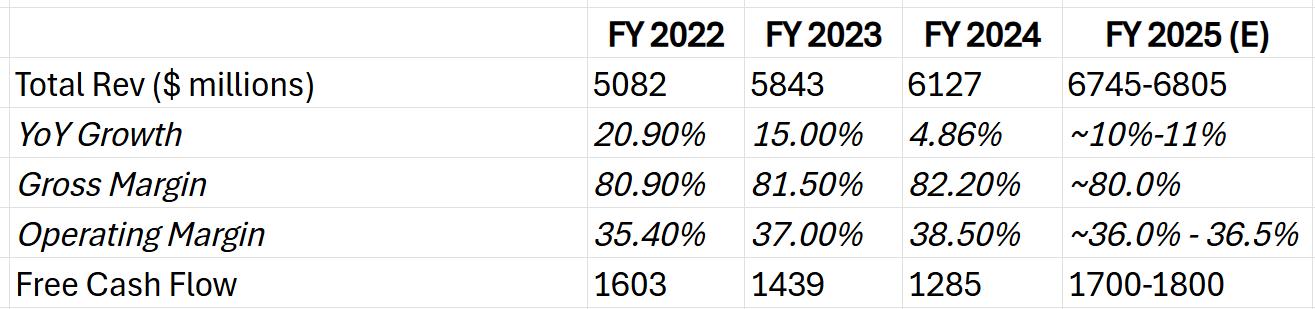

Over the past three years, Synopsys' revenue went from rapid growth to gradual slowdown and then mild recovery. In the fiscal year 2022, the semiconductor boom and the demand for advanced process tools contributed to the growth. However, the slowdown in the fiscal years 2023-2024 was affected by the sluggishness of consumer electronics and the delay of orders. The gross profit margin remained above 80%, reaching 82.2% in 2024. The EDA business (85%-87%) was higher than the IP business (75%-78%), and the operating profit margin increased from 35.40% to 38.50%. Free cash flow dipped to $1.285 billion in 2024, mainly from accounts receivable days stretching from 68 to 85 and higher R&D spending.

In the third quarter of 2025, Synopsys' stock price plummeted by more than 40%, mainly due to the failure to meet expectations in the financial report, which was caused by the intensified trade tensions between China and the United States and the associated risks in the Chinese business. U.S. tightened export curbs on EDA software to China, delaying or canceling IP deals there. Add in soft Chinese semiconductor demand and firms working through excess capacity, and IP revenue took a big hit. A key foundry client's project cutbacks dragged IP down further. Even though IP isn't directly restricted, the company paused China IP ops for compliance. Since IP revenue gets recognized at milestones like project starts, integration, and verification, clients need to finish designs with EDA tools first before embedding IP. If designs stall due to external factors like export limits, IP delivery and revenue recognition get pushed way back. In contrast, the EDA business adopts a subscription model, which is less affected by short-term market fluctuations.

Due to this impact, although the revenue in the third quarter of the fiscal year 2025 reached 1.74 billion US dollars (increase 14% YoY), the GAAP net income was 248 million US dollars, showing a year-on-year decrease. The gross profit margin and operating profit margin were under pressure. Geopolitical uncertainties prompted many clients to adopt a wait-and-see attitude, suspend or postpone projects. As a result, the company released a much lower-than-expected fourth-quarter guidance and a conservative outlook for the full-year revenue, which led to a loss of investor confidence.

Source: SEC, Company Report

Is It Time to Buy Now?

Lately, news like NVIDIA investing in Intel, pumping $100 billion into OpenAI, and Oracle teaming up with OpenAI has lifted semiconductor supply chain stocks, pushing Synopsys back up to around $500. But these short-term boosts only give temporary lifts; long-term gains need solid performance backing. We figure for Synopsys to regain real stock momentum, keep an eye on these:

China Market Order Recovery: China makes up over 10% of revenue and is crucial for IP rebound. If the Chinese orders resume smoothly in the coming quarters, it is expected that the revenue from the IP business will improve in the fourth quarter of 2025 or early 2026, providing sustained upward momentum for the stock price.

Major Foundry Client Projects Restarting: Watch if key foundry clients kick off design projects again—that directly juices growth.

Ansys Acquisition's Effect Plays out: Synopsys is buying Ansys for about $35 billion; Ansys leads in industrial simulation software for things like structural mechanics, fluid dynamics, and electromagnetics, while Synopsys focuses on chip design. Combining them lets designers simulate how chips perform in end products—like heat dissipation or power use in phones, cars, or planes—right during the design phase, boosting efficiency and reliability big time. The deal expands Synopsys' market from semiconductors to industrial, automotive, and aerospace sectors, bumping total addressable market (TAM) to $31 billion, about 1.5 times bigger. This not only taps high-growth areas but integrates EDA with system-level workflows, sticking clients tighter and building a wider moat that's hard for rivals to cross short-term.

Valuation

The 2025 expected P/E industry average is 38.2x, with Cadence at 45.7x, and Mentor and Keysight around 34.5x. Markets used to give Synopsys a premium for its "high growth + high certainty" story. With fundamentals dinged now, valuations need to be more conservative. But given its edge in AI design tools and automotive electronics IP, we're assigning a 36x-38x target P/E. Based on $12.83 EPS, that gives a 12-month target price range of $462-$488.

Looking at valuation drivers, short-term catalysts could be exploding demand for AI chip tools and IP growth recovery; longer-term, the company's plays in emerging tech like quantum computing tools, Ansys synergies, and edge AI solutions will decide if the premium holds.

Source: Macrotrends

Risk

· Geopolitical and China Market Risks (Already Hit and Core Issue): This is the biggest, most immediate threat right now. Management called it out in earnings as the main reason for misses—tighter U.S. export controls to China, plus resulting soft demand and order delays, slamming short-term performance. There's still a chance controls tighten more or the market stays weak.

· Acquisition Integration Risks: The massive Ansys buyout spikes Synopsys' debt from $700 million to $15.14 billion, assets to $48.23 billion, and debt-to-equity to 0.55. Leaders plan to cut debt to under 2x adjusted EBITDA in two years, relying on strong cash flow. However, the weak performance of the IP business and the increasing macro risks have intensified the financial pressure, and close monitoring of cash flow and the deleveraging process is necessary.

· Tech Evolution and Competition: The competition with Cadence remains intense. When the market is not favorable, customers may be more inclined to choose solutions with better cost-effectiveness. Any technological lag could lead to the loss of market share. In addition, in the short term, Chinese competitors may erode its low-end IP market share in China. In the long term, if China breaks through the bottleneck of high-end IP technology, competition is expected to intensify.

· Macroeconomic Cycles: The global semiconductor sector is cyclical. A recession would see companies cut R&D budgets, hitting Synopsys broadly, not just in one area.

Conclusion

As a leader in EDA and IP, Synopsys enjoys long-term investment value thanks to its technological barriers, customer loyalty, and the AI boom. The acquisition by Ansys has expanded its market boundaries and strengthened its competitive moat. However, geopolitical risks, weak demand from the Chinese market, and uncertainties in the acquisition integration have put pressure on short-term performance and challenged the valuation premium. Currently, the increase in stock prices is mainly driven by the AI craze. The company's fundamentals have not yet fully recovered. It is expected that the recovery of orders in the Chinese market and the synergy effect brought about by the Ansys integration will become the key driving forces. The target price range is $462 - $488. We recommend that investors closely monitor the market dynamics in China, the progress of customer projects, and the process of debt deleveraging. Make prudent investments to balance risks and long-term growth potential.

Recommended Articles