China’s May CPI Flat at -0.1%, PPI Deflation Accelerates as Auto Price Wars Intensify Factory Pressures

TradingKey - Weighed down by domestic manufacturers’ price wars, uncertainty from the U.S.-China tariff conflict, and weak domestic consumption, China’s May Consumer Price Index (CPI) and Producer Price Index (PPI) both continued to decline, with the PPI now in deflation for a 32nd consecutive month.

According to data released by China's National Bureau of Statistics on June 9, China’s CPI fell 0.2% month-on-month in May and declined 0.1% year-on-year, matching April’s reading. Core CPI, which excludes food and energy prices, rose 0.6% year-on-year, up 0.1 percentage points from the previous month.

Dong Lijuan, chief statistician at the NBS Department of Urban Statistics, noted that the shift from growth to a decline in CPI on a monthly basis was mainly driven by falling energy prices — which dropped 1.7% in May and accounted for about 70% of the overall decline in CPI.

However, consumer demand continues to recover gradually, supported by holiday travel and various cultural and entertainment activities across cities. Prices for hotels and tourism rose 4.6% and 0.8%, respectively, above seasonal levels.

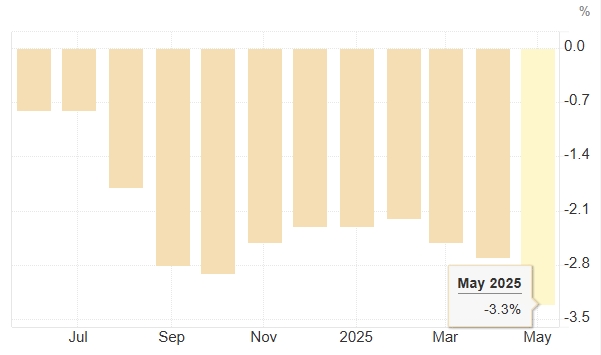

May’s PPI fell 0.4% month-on-month, unchanged from the previous month, while the annual decline widened to 3.3%, compared with a 2.7% drop in April. This marks the 32nd straight month of deflation in factory-gate prices and the largest annual decline in 22 months, exceeding market expectations of a 3.2% fall.

China’s May PPI Price Index, Source: Trading Economics

Analysts say the cooling industrial activity highlights the impact of U.S. tariffs on China, the world’s largest manufacturing hub, and is also dampening rapid growth in the services sector.

Markets are now closely watching the first meeting of the U.S.-China Economic and Trade Consultation Mechanism held in the UK this week, where tariff rates, rare earth exports, and semiconductor export controls will be key topics of discussion.

Meanwhile, Chinese consumers remain cautious after years of prolonged weakness in the property market, while price competition intensifies in industries such as new-energy vehicles (NEVs). Last month, BYD cut prices on certain electric vehicle models by up to 34%, raising concerns over a potential market correction in the NEV sector.

JPMorgan economists forecast that deflationary pressures in China may deepen rather than improve, with economic growth expected to slow sharply in the second half of the year due to weakening exports and subdued consumer confidence.

Dong Lijuan, however, expressed optimism, noting that with stronger macroeconomic policy support, supply-demand dynamics have improved in some sectors, and prices in certain areas are showing signs of recovery. For example, growing consumption momentum has lifted prices for consumer goods, while the development of advanced manufacturing sectors — such as integrated circuit packaging and testing, aircraft manufacturing, and wearable smart devices — has contributed to rising industrial prices.

Recommended Articles