Rate Cuts or Hikes in 2026? Here’s What the Fed Just Signaled in Today’s FOMC

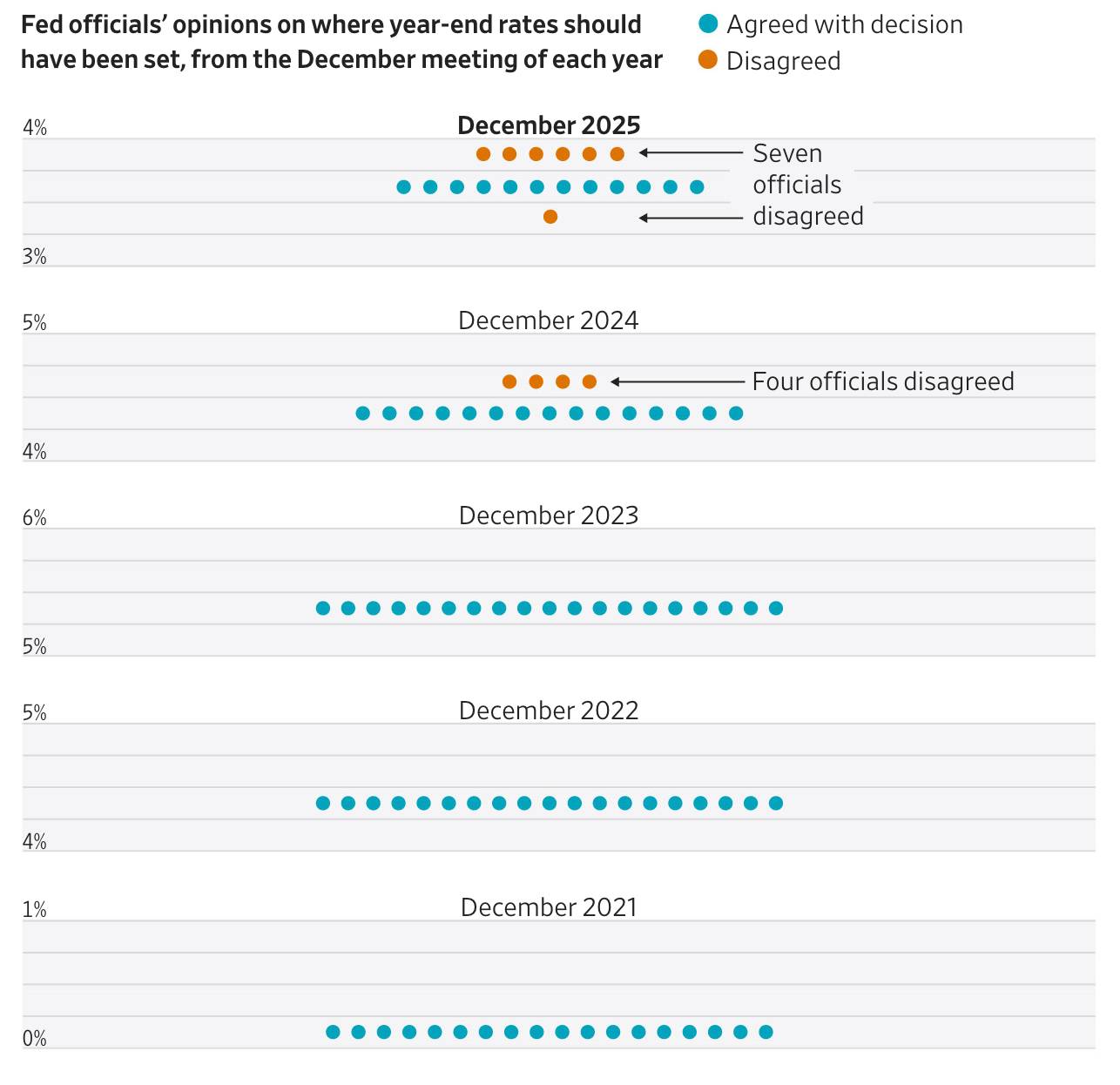

TradingKey – The Federal Reserve cut interest rates by 25 basis points on December 10, US Eastern Time, as widely anticipated, with the resolution passing by a 9-3 vote. This marked the first time in six years that three officials dissented, with two arguing against a rate cut and newly appointed Fed Governor Smirlan favoring a larger reduction.

[Fed Internal Dissent Overview, Source: Federal Reserve]

Fed Chair Jerome Powell has repeatedly stated that a certain degree of disagreement is normal. He emphasized that these differences primarily center on the relative weighting of two key risks and the pacing of policy adjustments. Such thorough, respectful debate is crucial for the Fed to make optimal decisions, and therefore, it will not constrain any policy options for the next meeting, nor will it create any preconceived outcomes.

While the rate cut met market expectations, investors focused more on the Fed's implicit guidance for next year's interest rates.

Powell indicated that, after accounting for duplicate counting, job growth might have been slightly negative since April. He suggested the labor market could be weaker than initially projected. Notably, Powell has increasingly weighed the impact of labor market weakness during the past two rate cuts.

Furthermore, Powell stated that no one anticipates a rate hike as a baseline expectation. The number of dissenting votes against the cut did not exceed market expectations, and Powell's remarks were less "hawkish" than anticipated. This injected confidence into the market and simultaneously set the tone for potential rate cuts in 2026.

[FED Dot Plot, Source: Federal Reserve]

Wall Street widely projects that the Fed will cut rates by significantly more than the 25 basis points indicated by the dot plot in 2026. This view is based on expectations of weakening wage growth and little sign of an inflation rebound in the first half of 2026.

Therefore, the path for rate cuts in 2026 remains the market consensus, indicating a significantly more dovish mainstream market view, at least until the U.S. Labor Department releases October and November employment data next week.

It should be noted that the Fed is still deliberating whether inflation or the job market poses a greater concern. If employment data in the coming months does not show significant weakening, a benchmark interest rate adjustment is unlikely at the January FOMC meeting.

Secondly, despite inflation remaining elevated, current data does not indicate a sustained increase but rather relative stability. Compared to persistent labor market weakness, the quality of employment data remains the dominant factor guiding the Fed's decision on whether to cut rates.

In addition, when addressing questions about reserve levels and money market tensions, Powell clarified that the resumption of balance sheet purchases constitutes technical reserve management, not quantitative easing. He reiterated that these Reserve Management Purchases (RMP) aim to maintain ample reserve levels, guard against seasonal liquidity fluctuations (such as the April 15, 2026 tax day shock), and support long-term economic expansion needs, remaining "completely separate" from monetary policy easing.

Recommended Articles