Japan’s 2026 Debt-Servicing Budget Hits Record High, Fueling a Bond Yield Spiral

TradingKey - To address rising "national debt service costs" caused by climbing Japanese government bond (JGB) yields, Japan’s Ministry of Finance is planning to request a record $220 billion for debt servicing in the 2026 fiscal year. Amid Bank of Japan rate hikes and concerns over fiscal deficits, larger borrowing needs could further fuel the upward trend in JGB yields.

According to a draft document seen by Reuters on Tuesday, August 26, the cost of paying interest and repaying debt in the next fiscal year, starting in April, will rise from ¥28.2 trillion in the current fiscal year to ¥32.4 trillion — approximately $219.8 billion — a 15% increase.

The total fiscal budget is expected to reach ¥34.1 trillion, meaning debt servicing costs will dominate the government’s borrowing needs. Japan’s Kyodo News noted this is intended to counter the trend of rising long-term bond yields, and the fiscal pressure from debt servicing is expected to persist.

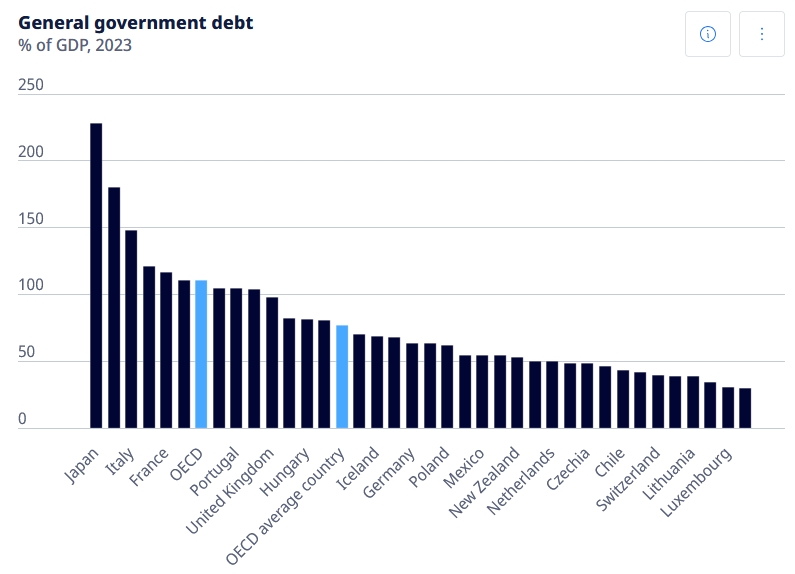

If approved, this would be the highest debt-servicing budget in the history of Japan’s Ministry of Finance, accounting for roughly one-quarter of the national budget. Japan carries the heaviest debt burden among all developed economies, and the severely "insolvent" nation must continue to bear the costs of an aging population and declining birth rates.

Government Debt Burden by Country, Source: OECD

Last week, Japan’s 10-year JGB yield hit a high of 1.615%, the highest since 2008, driven by strong economic data boosting expectations of BOJ rate hikes and ongoing fiscal concerns after the ruling coalition lost its majority in the July upper house election.

Japan’s Finance Minister acknowledged market unease over the bond market, calling it a reflection of concerns about national fiscal policy. He pledged to conduct appropriate debt management, improve fiscal health, and maintain market confidence.

Sources said the planned interest rate assumption for the 2026 fiscal year will rise from 2.0% in the current budget to 2.6% — the highest in 17 years.

Using record-level borrowing to cover rising interest costs could signal an even stronger wave of bond issuance ahead. This concern may further exacerbate upward pressure on JGB yields, doing little to curb the growing debt burden.

Recommended Articles