Bitcoin Breaks $78,000 Amid U.S.-Iran Conflict, Can It Return to $100,000 in 2026?

TradingKey - On April 17, catalyzed by the announcement of a ceasefire between the U.S. and Iran, the temporary reopening of the Strait of Hormuz, and substantive progress in the U.S. crypto asset regulatory framework, Bitcoin touched $78,384 intraday. This successfully broke through the descending resistance line that has suppressed every rally since October 2025; Bitcoin has now rebounded approximately 21% from its March low of $62,500.

Nevertheless, Bitcoin (BTC) following the upward breakout, divergence between bulls and bears has increased rather than diminished.

On-chain metrics lack consistency—Glassnode's TMM (True Market Mean) indicator is currently near $78,000, and whether price can reclaim this level is the core dividing line between a rally and a trend reversal. New capital continues to flow out of the market, with realized capitalization falling from approximately $1.12 trillion at the start of the year to about $1.08 trillion, a 3.2% decline, as net capital has failed to flow in.

Crypto Legislation May Serve as Catalyst for Future Narratives

On April 16, JPMorgan analysts released a report noting that negotiations for the CLARITY Act have entered the final stage, with the number of disputed points dwindling from over a dozen to two or three core issues, primarily revolving around stablecoin reward rules, DeFi regulation, and token classification. Senate staff described the draft as "very close" to resolution, with a target date of mid-2026.

Once passed, the bill will end the SEC’s years of "regulation by enforcement," clearly delineating the regulatory jurisdictions of the SEC and the CFTC. Most mainstream tokens will fall under the CFTC’s jurisdiction, significantly reducing the compliance burden.

JPMorgan previously stated that the bill's passage will be the "ultimate catalyst" for the crypto market. A clear regulatory framework will unlock the allocation intent of large asset managers, pension funds, and corporate treasury departments that were previously on the sidelines due to legal uncertainty, thereby "opening the floodgates for institutional entry."

Meanwhile, the GENIUS Act (the federal regulatory framework for stablecoins), which was signed into law in July 2025, is moving from paper to implementation. On April 8, FinCEN and OFAC jointly released proposed rules requiring stablecoin issuers to establish anti-money laundering and sanctions compliance programs; on April 10, the OCC proposed a comprehensive federal regulatory framework covering reserve management, capital requirements, licensing, custody, and redemption.

This marks the crypto industry's transition from an opaque market into a manageable compliance framework.

Furthermore, Patrick Witt, Executive Director of the White House Digital Assets Advisory Council, confirmed on April 18 that the Trump administration plans to unveil a formal strategy for a strategic Bitcoin reserve within the next two months, utilizing Bitcoin seized in government enforcement actions to establish a national reserve.

The U.S. government currently holds approximately 200,000 BTC, a move viewed as official recognition of Bitcoin as a legitimate asset class.

Can Bitcoin break through $100,000?

Mainstream market institutions' predictions for the $100,000 level exhibit a polarized landscape.

Among the optimists, Bernstein maintains its $150,000 forecast for the end of 2026, arguing that the institutionalization process will break traditional bear market patterns. Janet Yellen's recent warnings about U.S. dollar hyperinflation have also added new policy-level credibility to the "digital gold" narrative for Bitcoin.

Conversely, signals from the pessimists suggest that a major uptrend remains difficult to foresee in the short term. Standard Chartered has downgraded its forecast twice, with the latest target at just $100,000, even warning of a potential preliminary drop to $50,000. Jurrien Timmer, Director of Global Macro at Fidelity, explicitly stated that October 2025 marked the peak of this cycle and that 2026 will be a "consolidation year."

Meanwhile, market capital structures also show divergence. JPMorgan pointed out that capital inflows into the crypto market during the first quarter were almost entirely driven by Strategy's purchases, while inflows from retail and most institutional investors remained weak.

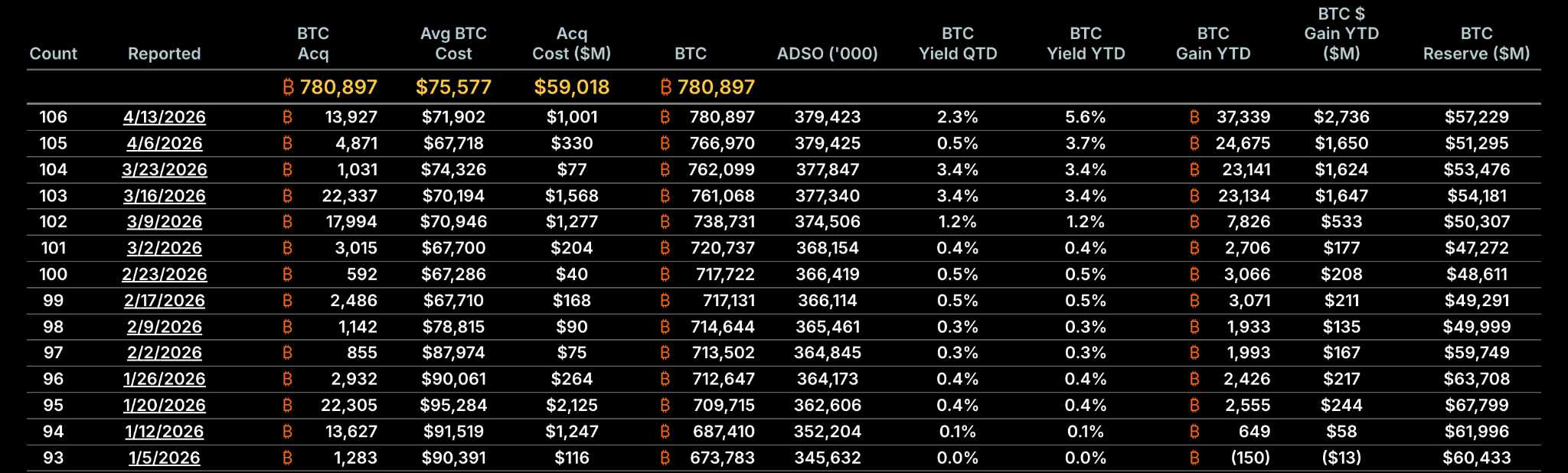

[MicroStrategy's Bitcoin Accumulation in Q1; Source: Strategy]

In the first quarter, Strategy purchased 89,599 BTC at an average cost of approximately $75,644. However, Bitcoin ETFs saw net outflows of $496 million during the same period, with $1.8 billion in outflows during the first two months being partially offset by $1.32 billion in inflows in March.

Andri Fauzan Adziima, Head of Research at Bitrue, stated that the Q1 decline was primarily driven by spot Bitcoin ETF outflows, compounded by persistently high inflation, the Federal Reserve's cautious stance, and a general market sentiment of risk aversion.

The derivatives market is accumulating the most significant volatility variables. Bitcoin perpetual contract funding rates have remained negative for a month and a half, marking the longest bearish streak since 2023. Bloomberg noted that this "divergence structure"—where spot prices remain strong while derivatives are bearish—often implies that short sellers will eventually be forced to close their positions, triggering a self-reinforcing "short squeeze" rally. The options market is similarly cautious, with risk reversal indicators showing that traders are more inclined to pay for downside protection than to chase gains.

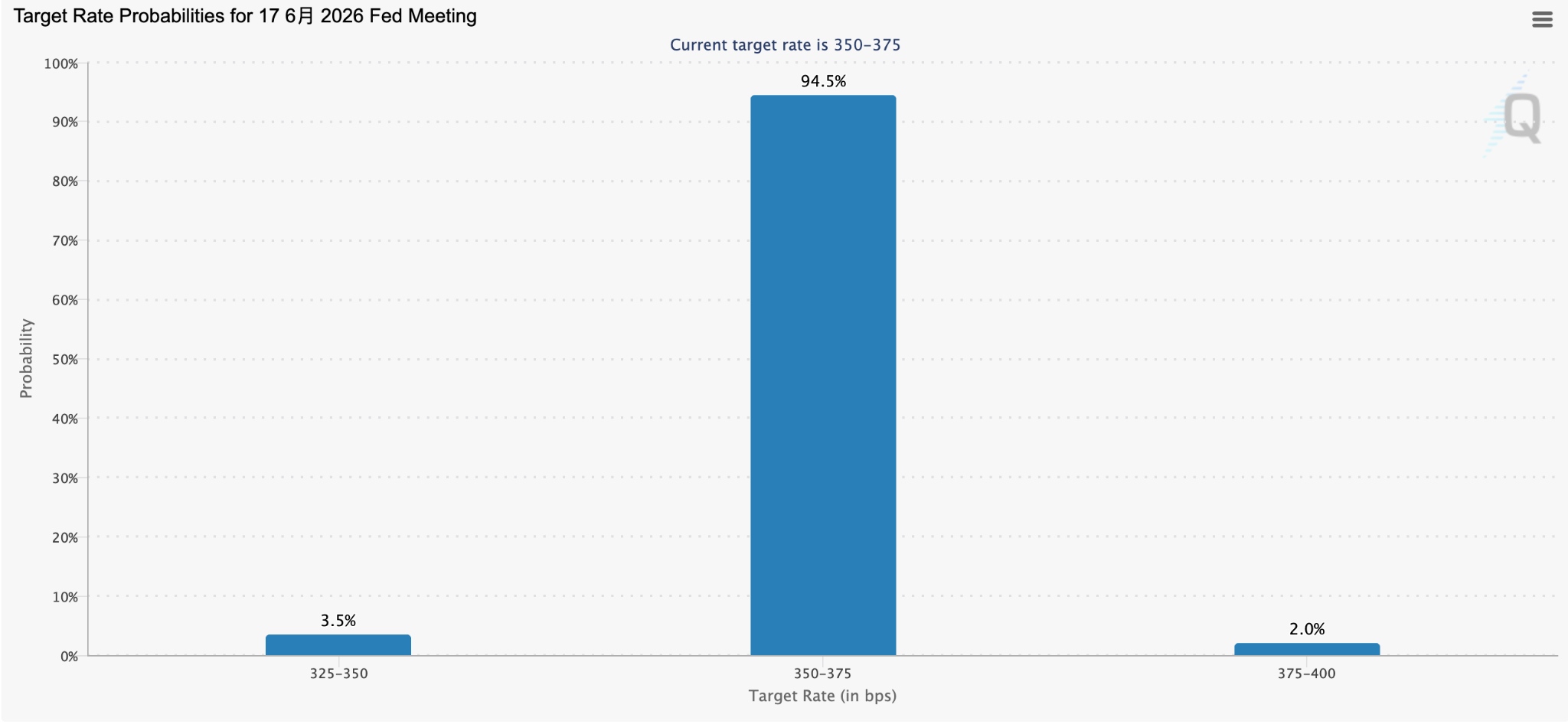

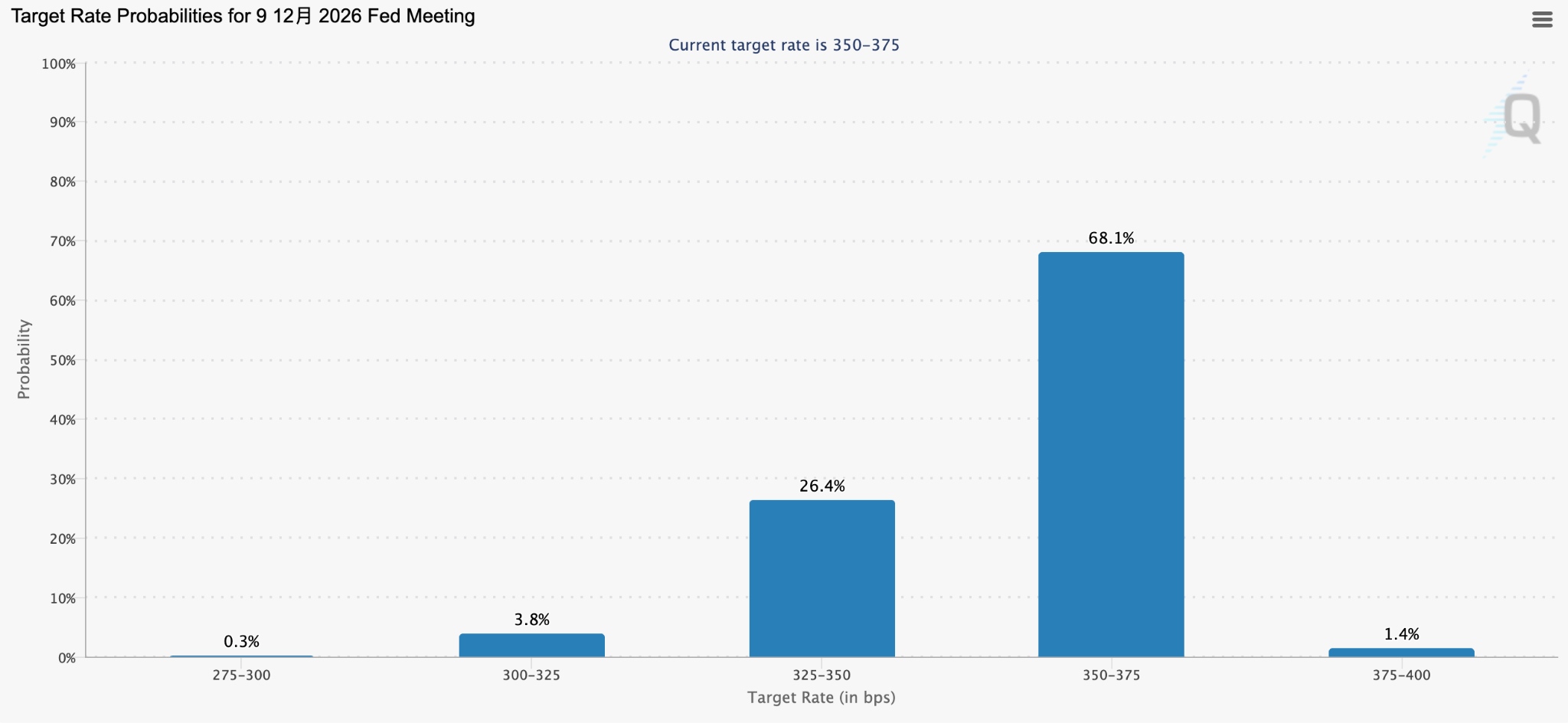

CME FedWatch shows that the market expects a 96.5% probability that the Fed will maintain interest rates in June, while the probability of no rate cuts this year remains as high as nearly 70%.

[Probability of a June Rate Cut vs. Full-Year Rate Cut; Source: CME group]

The high-interest-rate environment has led investors to view Bitcoin as a "high-risk, high-beta asset" for hedging, rather than increasing allocation during periods of risk aversion. Oil prices have dampened expectations for rate cuts via inflation expectations, exerting periodic pressure on Bitcoin.

Overall, Bitcoin is at a classic "long-short tipping point." Although touching the $78,000 mark provided a technical breakout signal, it has not been confirmed by on-chain capital and ETF flows. The risk of a short squeeze and uncertainty regarding macro interest rate policies continue to cloud Bitcoin's trajectory. While progress on regulatory clarity is the strongest structural support, there remains a risk that legislation could be delayed by the midterm elections.

Returning to $100,000 by 2026 implies that Bitcoin would need to achieve a gain of approximately 28%—driven by regulatory framework upgrades and its own demand logic—even in an environment where the Fed does not cut rates. This remains a possibility under the multiple catalysts of technical breakthroughs, short squeezes, and regulatory implementation.

Recommended Articles