If World War 3 Fears Spike, Does Bitcoin Crash or Become Digital Gold?

War scenarios do not reward clean narratives. Markets usually do two things at once. They sprint into safety, then they reprice the world after the first shock passes. Bitcoin sits right on that fault line.

That is why the “WW3 trade” is not a single bet. It is a sequence. In the first hours, Bitcoin often behaves like a high-beta risk asset. In the following weeks, it can start behaving like a portable, censorship-resistant asset, depending on what governments do next.

Are ‘World War 3’ Fears Real Right Now?

Given the current geopolitical escalations, the world world 3 conversation is more real than ever. Some might even say we are in the midst of a world war, but it’s functioning differently than it did 90 years ago.

Over the past few weeks, multiple flashpoints have tightened the margin for error.

Europe’s security debate has shifted from theory to operational planning. Officials have discussed post-war security guarantees around Ukraine, a topic that Russia has historically treated as a red line.

In the Indo-Pacific, China’s military drills around Taiwan have looked increasingly like blockade rehearsals. A blockade-style crisis does not need an invasion to break markets. It only needs shipping disruption and an incident at sea.

Add the United States’ broader posture. President Trump is basically ‘running Venezuela’ in his own comments after capturing its president from his home.

And now, the US government is talking about buying Greenland, a sovereign country that’s part of Denmark and the EU.

Then there’s Sanctions enforcement, higher-risk military signaling, and sharper geopolitical messaging. Add these, and you get a global environment where one mistake can trigger another.

This is exactly how crises become linked.

What “WW3” Means in this Model

This analysis treats “World War III” as a specific threshold.

- Direct, sustained conflict between nuclear powers, and

- Expansion beyond one theater (Europe plus the Indo-Pacific is the clearest route).

That definition matters because markets react differently to regional conflicts than to multi-theater confrontations.

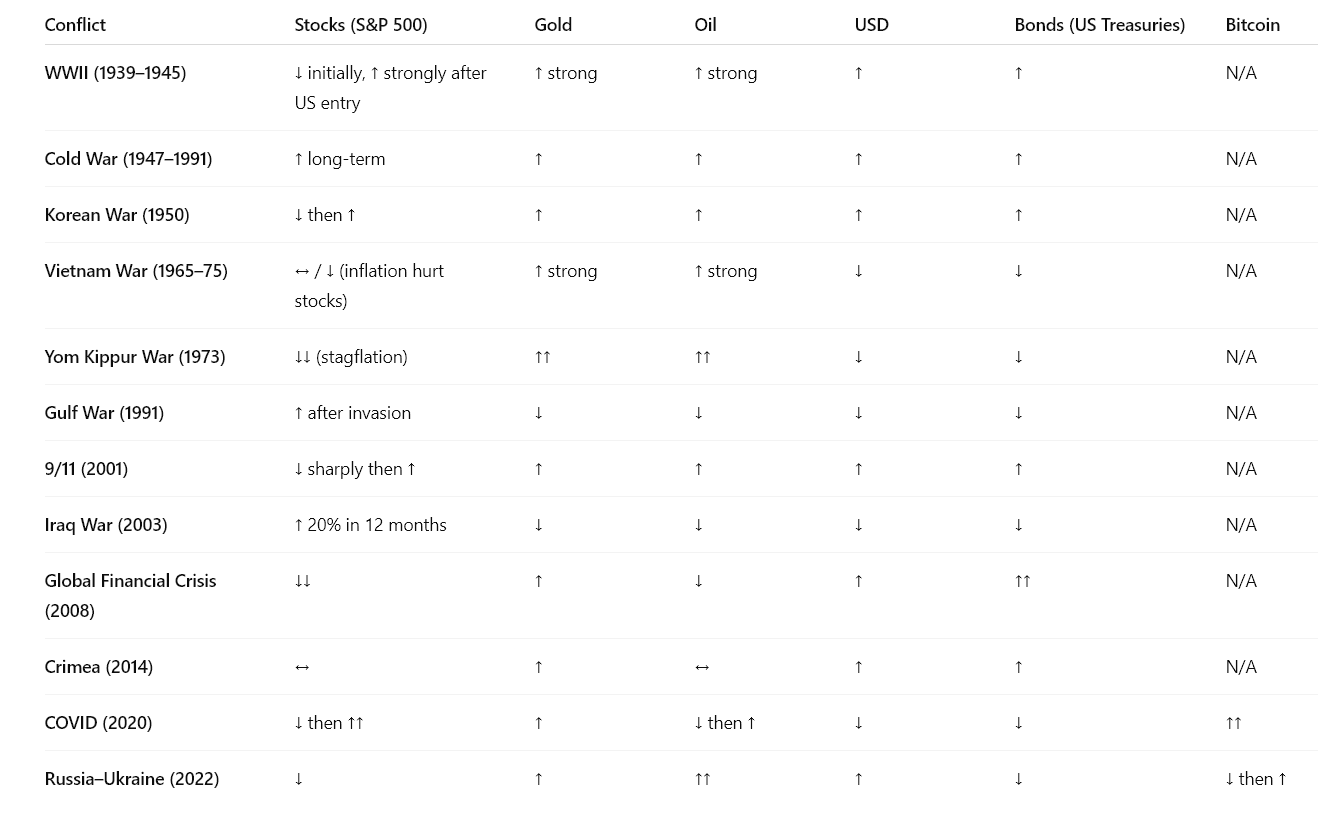

How Major Assets Behave Around War

The single most useful lesson from past conflicts is structural: Markets usually sell the uncertainty first, then trade the policy response.

How Major Assets Actually Performed During Wars & Crises

How Major Assets Actually Performed During Wars & Crises

Stocks

Equities often drop around the initial shock, then can recover once the path becomes clearer—even while war continues. Market studies of modern conflicts show that “clarity” can matter more than the conflict itself once investors stop guessing and start pricing.

The exception is when war triggers a lasting macro regime change: energy shocks, inflation persistence, rationing, or deep recession. Then equities struggle for longer.

Gold

Gold has a long record of rising into fear. It also has a record of giving back gains once a war premium fades and policy becomes predictable.

Gold’s edge is simple. it has no issuer risk. Its weakness is also simple: it competes with real yields. When real yields rise, gold often faces pressure.

Silver

Silver behaves like a hybrid. It can rally with gold as a fear hedge, then whipsaw because industrial demand matters. It is a volatility amplifier more than a pure safe haven.

Oil and Energy

When conflicts threaten supply routes, energy becomes the macro hinge. Oil spikes can shift inflation expectations quickly.

That forces central banks to choose between growth and inflation control. That choice then drives everything else.

Bitcoin in a World War: Bulls or Bears?

Bitcoin does not have a single war identity. It has two, and they fight each other:

- Liquidity-risk Bitcoin: behaves like a high-beta tech asset during deleveraging.

- Portability Bitcoin: behaves like a censorship-resistant, borderless asset when capital controls and currency stress rise.

Which one dominates depends on the phase.

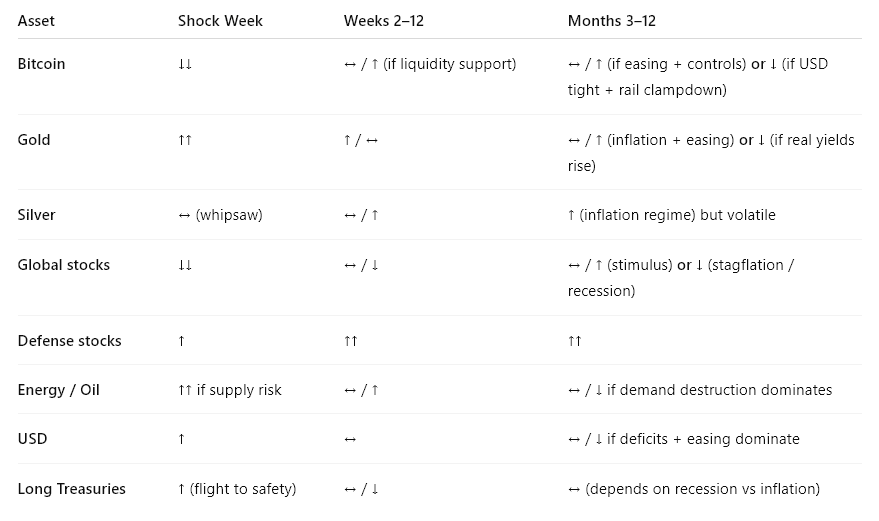

Phase 1: Shock Week

This is the forced selling phase. Investors raise cash. Risk desks cut leverage. Correlations jump.

In this phase, Bitcoin usually trades with liquidity risk. It can fall alongside equities, especially if derivatives positioning is crowded or if stablecoin liquidity tightens.

Gold tends to catch the first safety bid. The U.S. dollar often strengthens. Credit spreads widen.

Phase 2: Stabilization Attempt

Markets stop asking “what just happened?” and start asking “what does policy do next?”

This is where Bitcoin can diverge.

If central banks and governments respond with liquidity support, backstops, or stimulus, Bitcoin often rebounds with risk assets.

If policymakers tighten controls—on capital, banking rails, or crypto on-ramps—Bitcoin’s rebound can become uneven, with higher volatility and regional fragmentation.

Phase 3: Protracted Conflict

At this point, the conflict becomes a macro regime. Here Bitcoin’s performance depends on four switches:

- Dollar liquidity: tight USD conditions hurt Bitcoin. Easier conditions help.

- Real yields: rising real yields pressure Bitcoin and gold. Falling real yields support both.

- Capital controls and sanctions: increase demand for portability, but can also restrict access.

- Infrastructure reliability: Bitcoin needs power, internet, and functioning exchange rails.

This is where “Bitcoin as digital gold” can emerge, but it is not guaranteed. It requires usable rails and a policy environment that does not choke access.

Below is a simplified stress table that readers can actually use. It summarizes directional expectations across the three phases for two WW3-style branches: Europe-led and Taiwan-led.

Legend: ↑ strong positive, ↑ positive, ↔ mixed, ↓ negative, ↓↓ strong negative

Legend: ↑ strong positive, ↑ positive, ↔ mixed, ↓ negative, ↓↓ strong negative

The key takeaway is uncomfortable but useful: Bitcoin’s worst window is the first window. Its best window is often later—if policy and rails allow it.

What Would Most Likely Decide Bitcoin’s Outcome

The “Real Yield” Regime

Bitcoin tends to struggle when real yields rise and USD liquidity tightens. War can push yields down (recession fear, easing) or up (inflation shock, fiscal stress).

Which one wins matters more than the headlines.

The Rails Problem

Bitcoin can be valuable and unusable at the same time for some participants.

If governments tighten exchange access, banking ramps, or stablecoin redemption paths, Bitcoin can become more volatile, not less.

The network can function while individuals struggle to move capital through regulated choke points.

Capital Controls and Currency Stress

This is the environment where Bitcoin’s portability becomes more than a slogan.

If conflict expands sanctions, restricts cross-border transfers, or destabilizes local currencies, demand for transferable value increases. That supports Bitcoin’s medium-term case, even if the first week looks ugly.

Energy Shock Versus Growth Shock

An oil spike with persistent inflation can be hostile for risk assets. A growth shock with aggressive easing can be supportive.

War can deliver either. Markets will price the macro path, not the moral narrative.

The Simple Forecast Structure

Instead of asking “Will Bitcoin pump or dump in WW3?”, ask three sequential questions:

- Do we get a shock event that forces deleveraging? If yes, expect Bitcoin downside first.

- Does policy respond with liquidity and backstops? If yes, expect Bitcoin to rebound faster than many traditional assets.

- Do capital controls and sanctions widen while rails remain usable? If yes, Bitcoin’s portability premium can rise over time.

This framework explains why Bitcoin can fall hard on day one and still end up looking resilient by month six.

The Bottom Line

A World War III or major geopolitical escalation shock would likely hit Bitcoin first. That is what liquidity crises do. The more important question is what comes after.

Bitcoin’s medium-term performance in a major geopolitical conflict depends on whether the world moves into a regime of easier money, tighter controls, and fragmented finance.

That regime can strengthen the case for portable, scarce assets—while still keeping them violently volatile.

If readers want one sentence to remember: Bitcoin probably does not start a war as “digital gold,” but it can end up trading like one if conflicts drag on.

Recommended Articles