Intel Corp Stock (INTC) Moved Down by 9.87% on Jul 7: Drivers Behind the Movement

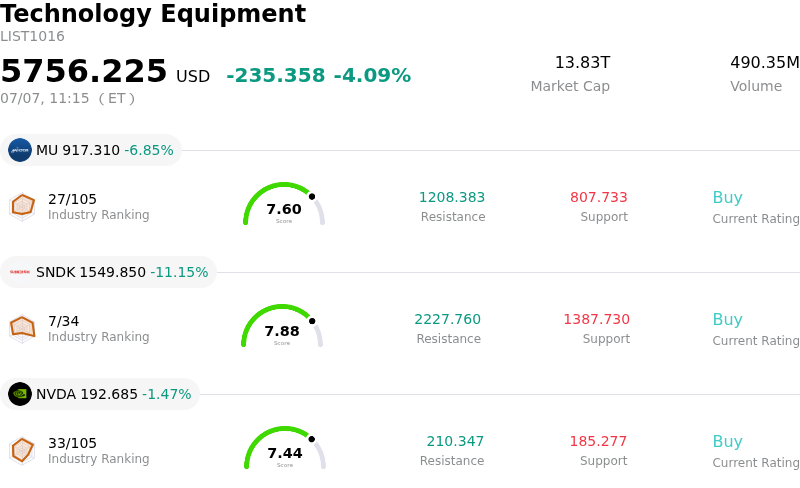

Intel Corp (INTC) moved down by 9.87%. The Technology Equipment sector is down by 4.09%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 6.85%; SanDisk Corporation (SNDK) down 11.15%; NVIDIA Corp (NVDA) down 1.47%.

What is driving Intel Corp (INTC)’s stock price down today?

Intel’s stock experienced a pronounced downward correction as part of a broader, high-volume retreat across the semiconductor sector. After a historic first-half rally in 2026, which saw chipmakers surge on immense artificial intelligence optimism, market sentiment shifted sharply. This momentum reversal was primarily triggered by warnings of rising semiconductor bubble risks and overstretched valuations. Investors increasingly rotated out of high-flying technology names to lock in profits, placing significant selling pressure on Intel as macro-sector anxieties intensified.

This industry-wide profit-taking has exposed company-specific vulnerabilities, particularly regarding the disconnect between Intel’s valuation and its underlying fundamentals. While speculative enthusiasm drove the stock to premium multiples earlier in the year, the chipmaker continues to navigate a highly capital-intensive turnaround. The financial reality of heavy ongoing losses in its foundry division, coupled with massive capital expenditure requirements, has led to increased valuation discipline among institutional investors. This tension is particularly acute as the market looks ahead to the upcoming second-quarter earnings release on July 23, where Intel must prove it can convert its structural turnaround promises into real, profitable growth.

Adding to these valuation worries are persistent execution concerns surrounding Intel's ambitious manufacturing and technology roadmap. Although the company has made progress with its advanced next-generation nodes, such as the 18A process, analysts do not expect profitable, commercial-scale yields until late 2026 or 2027. This timeline lag threatens to dilute near-term gross margins and prolong reliance on internal product demand rather than lucrative external customer contracts. In the first quarter, external foundry revenue remained minimal, emphasizing that Intel’s transition into a highly profitable contract manufacturer is still in its infancy.

Furthermore, rising global supply chain and input costs have forced the company to implement selective price hikes on certain consumer and server processors. While this strategy aims to protect margins, it adds downstream pressure and underscores the persistent operational headwind of running a highly capital-intensive domestic manufacturing business.

Technically, the stock’s downward momentum has broken below key near-term support levels, including its 20-day simple moving average. This breach has accelerated the shift toward a more cautious, risk-off posture among traders, transforming previous support into immediate resistance. Collectively, the combination of sector-wide valuation reassessments, near-term margin dilution risks, and execution anxieties ahead of the upcoming earnings report has driven the sharp pullback in Intel's shares.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of -3.031, indicating a neutral signal. The RSI at 50.343 suggests neutral condition and the Williams %R at 76.471 suggests sell condition. Please monitor closely.

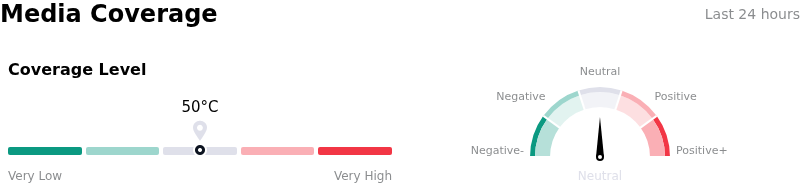

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 50, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $97.33, a high of $200.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Unprofitable Next-Gen Node Yields: While Intel has moved its critical 18A-P process node into the risk production phase, current yields remain below commercial-scale profitability thresholds. Institutional analysts flag that profitable yields are unlikely to materialize until late 2026 or 2027, exposing the company to near-term gross margin dilution amid heavy capital expenditures.

- Severe Valuation Premia and Sentiment Vulnerability: Following a massive multi-quarter run, Intel’s valuation has stretched to highly sensitive multiples (e.g., a Price-to-Sales ratio over 12x versus the industry average). This elevated valuation relies heavily on unproven external foundry revenues, making the stock highly susceptible to sharp intraday sell-offs during broader market rotations out of high-multiple semiconductor equities.

- Imminent Margin Squeeze: On July 6, 2026, Intel confirmed selective price hikes on specific consumer and Xeon server processors to counteract rising global supply chain costs and advanced node capacity constraints. Analysts warn that these rising input costs, paired with the expensive ramp-up costs of new manufacturing nodes, present a substantial threat to near-term gross margins that could offset revenue gains in upcoming quarters.

- Foundry Scaling Execution Risk: A substantial portion of Intel's current market premium assumes rapid scaling of its contract manufacturing business, yet the segment posted a $2.4 billion operating loss in Q1 with external customer revenue standing at a minimal $174 million. If the upcoming Q2 earnings report on July 23, 2026, fails to show tangible commercial contract wins and revenue progress, the stock faces significant downside risk.

Recommended Articles