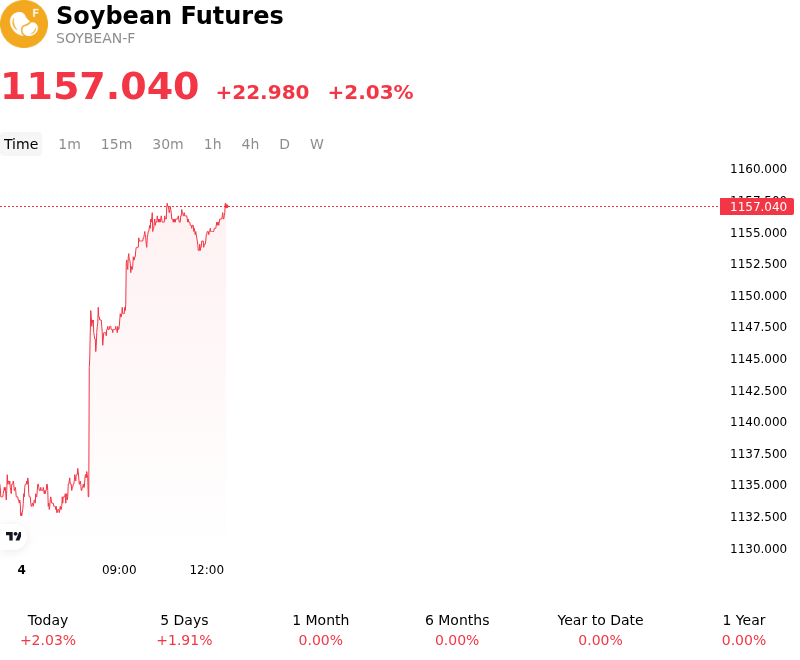

Soybean Futures (SOYBEAN-F) Is up 2.03% on Jul 6: Key Drivers to Watch

Soybean Futures (SOYBEAN-F) is up 2.03% at Jul 6 01:35(ET), now at $1157.04, with a 7-day up of 3.49%.

What is driving Soybean Futures (SOYBEAN-F)’s stock price up today?

Chicago Board of Trade soybean futures advanced as the market digested a combination of intensifying domestic demand indicators and localized weather concerns, which outweighed the long-term outlook of a highly productive upcoming harvest. This upward price momentum represents a critical recalibration of near-term balance sheets, reversing some of the bearish sentiment that had accumulated in the preceding weeks.

The primary catalyst for the price advance stemmed from the demand side. While the U.S. Department of Agriculture's acreage reports signaled a comfortable domestic supply cushion, the accompanying Quarterly Grain Stocks report revealed historically robust domestic consumption of soybeans. Domestic soybean disappearance during the third quarter of the marketing year reached exceptionally high levels. This rapid consumption pace was heavily supported by soaring domestic crush margins. Industrial demand for soybean oil—principally driven by its expanding role in renewable fuel production—has significantly accelerated domestic processing activities, tightening the immediate supply of physical beans.

On the supply side, seasonal weather risks in the Northern Hemisphere have re-emerged as a major trading catalyst. As the crop enters its critical mid-summer developmental phase, traders are increasingly sensitive to localized weather disruptions. Forecasts of high temperatures and mixed rainfall patterns across key portions of the U.S. Midwest have introduced localized crop anxieties. Since the planting phase is largely complete, the market's focus has transitioned entirely to yield potential. The potential for heat stress to limit optimal pod development and yield efficiency prompted short-sellers to trim exposure and led asset managers to rebuild risk premium.

Furthermore, although weekly export sales figures showed some volatility and recently dipped to marketing-year lows, the underlying domestic demand and the fast pace of domestic stockpile depletion have temporarily eclipsed the broader, supply-heavy outlook for the upcoming marketing year. Investors continue to monitor upcoming government production updates and macroeconomic factors, including fluctuations in the U.S. dollar and broader central-bank interest rate policies, which influence institutional capital flows into agricultural commodities. However, for the current session, the confluence of high domestic crush demand and summer weather premiums remained the dominant drivers of the upward price volatility.

More details about Soybean Futures (SOYBEAN-F)

Recent Events and Risks:

- Substantial Acreage and Production Expansion: The USDA’s June 30, 2026 Acreage Report confirmed that U.S. soybean plantings have expanded by 5% year-over-year to 85.37 million acres. This puts U.S. growers on track for a potentially record-breaking harvest of approximately 4.473 billion bushels, structurally limiting long-term upward price potential and creating deep downside vulnerability in futures.

- Bearish Quarterly Stock Pileup: The USDA's Quarterly Grain Stocks report revealed that U.S. old-crop soybean inventories as of June 1, 2026, jumped 5% year-over-year to 1.061 billion bushels. This exceeded average analyst expectations of 1.046 billion bushels, demonstrating a comfortable domestic supply cushion that actively pressures spot and nearby futures contracts.

- Deteriorating Export Demand and Cancellations: Weekly export data released ahead of the July 4th holiday weekend hit a marketing-year low. Old-crop export sales were weighed down by a massive cancellation of shipments from "unknown destinations", highlighting weak global purchasing interest and increasing dependence on sluggish international demand.

- Macroeconomic Pressures and Currency Headwinds: Soybean futures face persistent headwinds from a stronger U.S. dollar, fueled by expectations of domestic interest rate hikes. This currency strength makes U.S. agricultural exports significantly more expensive for foreign buyers, threatening to accelerate a shift in export volume toward cheaper South American competitors like Brazil.

Recommended Articles