U.S. September Nonfarm Payrolls: Two-Scenario Analysis, Will U.S. Stocks Diverge in Short-Term and Medium-to-Long-Term Trends?

- Gold Price Trend Forecast: Expectations of Easing US-Iran Tensions Boost Gold Prices, $4,070 Becomes Key Level for Bulls and Bears

- TradingKey Daily Market Brief: Gold Falls Below $4,000, TSMC’s Strong Earnings Fail to Stop AI Trade Cooling, Chip Stocks Sold Off

- Gold Price Forecast: Cooling Inflation Fails to Offset Fed Hawkish Pressure, Gold Price May Fall to $3,500

- Euro declines to near 1.1400 as US launches fresh strikes on Iran

- Tesla Q2 Earnings Preview: Record Deliveries Fail to Hide Profit Pressure, Can Musk Rely on AI and Autonomous Driving to Unlock New Growth Space?

- Today’s Market Recap: Unexpected PPI Drop Boosts Markets, Apple Hits All-Time High, AI Hardware Stocks Remain Under Pressure, Micron, SanDisk Slump

1. Introduction

Affected by the U.S. government shutdown, the September nonfarm payrolls report—originally scheduled for release in early October—will be officially published on 20 November. As a key "barometer" for gauging the health of the U.S. economy, this report will guide investors in assessing the Federal Reserve’s next policy moves. Amid the Fed officials’ hawkish stance and fading expectations of a rate cut in December, U.S. stocks have recently pulled back from record highs and entered a phase of sharp volatility (Figure 1). This paper conducts an analysis of the U.S. September nonfarm payroll data and the subsequent employment market through two scenario-based assessments, alongside a short-term and medium-to-long-term outlook for U.S. stocks.

Our research conclusions are as follows: In the medium-term perspective, sustained weakness in the U.S. job market will prompt more aggressive interest rate cuts, which in turn will benefit U.S. stocks. If the job market rebounds, it will boost economic recovery and also provide support for U.S. stocks. Therefore, passive investors may focus on U.S. broad-market ETFs such as SPY and QQQ. For active investors: if anticipating interest rate cut trades driven by slowing employment, they can prioritize tech giants including NVIDIA (NVDA), Apple (AAPL), and Tesla (TSLA); REITs sector leaders like Prologis (PLD) and American Tower (AMT); gold mining companies such as Newmont (NEM) and Barrick Gold (GOLD); as well as General Motors (GM) and Ford (F) in the discretionary consumer and high-leverage sectors, plus United Airlines (UAL) in the aviation industry. If expecting a job market recovery to enhance U.S. economic resilience, they may focus on consumer staples players, including Amazon (AMZN) and Dollar General (DG); Johnson & Johnson (JNJ) in the healthcare sector; and JPMorgan Chase (JPM) and Goldman Sachs (GS) in the financial sector.

It is important to note that while we hold a medium-term bullish view on U.S. stocks, the job market and Federal Reserve monetary policy exert a countervailing force. A recovery in employment will prompt the Fed to slow its interest rate cut pace, while the opposite may accelerate rate cuts — leading to continued sharp short-term volatility in U.S. stocks. However, a significant pullback would present an excellent entry opportunity for medium-to-long-term investors.

Figure 1: S&P 500 Index

Source: Mitrade

2. Scenario 1: Persistently Weak Job Market

2.1 Causes of the Weak Job Market

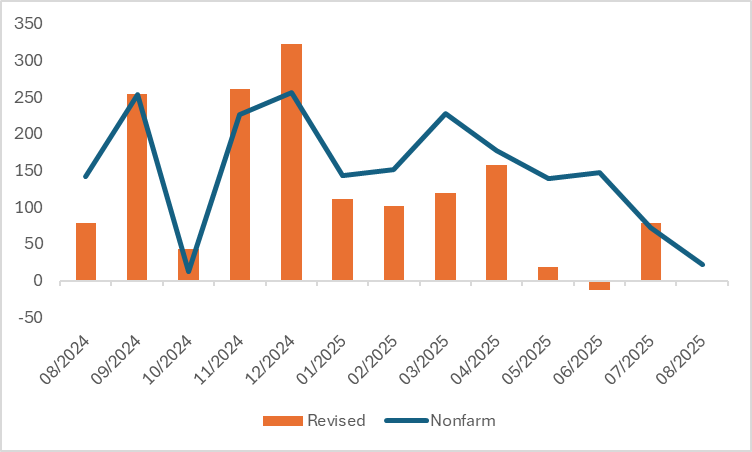

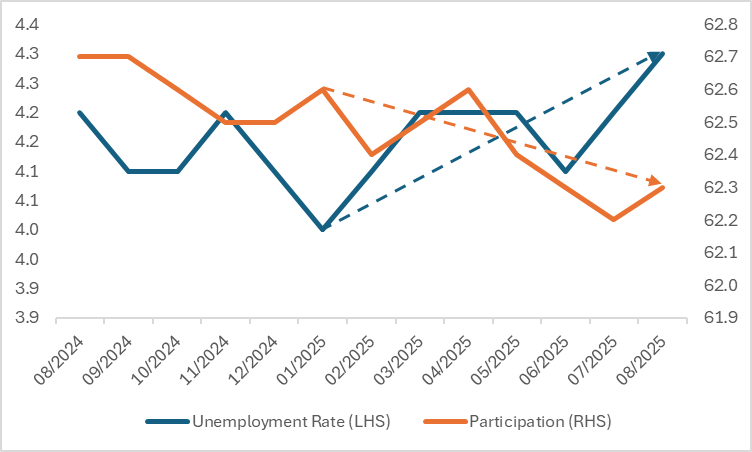

Scenario 1 assumes that the U.S. job market will remain weak in September and the subsequent months. The reasons include the following: First, the momentum of the labour market continues to fade. Although the release of official data has been suspended due to the government shutdown, data published before the shutdown have already painted a clear downward trend. Since the end of last year, U.S. nonfarm payrolls have been on a steady decline, dropping to just 22,000 in August alone (Figure 2.1.1). Over the same period, the unemployment rate has risen to 4.3%, leading to a continuous decline in the labour force participation rate (Figure 2.1.2). This has created a triple pressure of "slowing job growth, rising unemployment, and insufficient labour supply." More alarmingly, since the start of this year, revised nonfarm payroll data has shown a cumulative reduction of over 480,000 jobs, further confirming the authenticity of the market weakness.

Second, the demand side of employment has been hit by economic uncertainty. Unclear macroeconomic prospects and rising tariff costs have forced enterprises to scale back recruitment. The private sector has witnessed severe job losses, particularly in cyclical industries — the construction sector has tightened amid a cooling housing market, while the manufacturing industry is trapped in a dual dilemma of "demand exhaustion + rising costs". Third, the drying up of labour market liquidity has led to mutual caution between enterprises and employees. Enterprise hiring rates have shown a downward trend, with layoff rates edging up, while employees' willingness to switch jobs has dropped to a low level. On one hand, layoffs and weak recruitment have undermined job-seeking confidence. On the other hand, the narrowing of salary increases from job-hopping has reduced the motivation to resign. Rising unemployment duration and the number of continuing unemployment benefit claimants indicate increased difficulty in reemployment, further freezing labour market liquidity.

Figure 2.1.1: U.S. Nonfarm Payrolls (000)

Source: Refinitiv, TradingKey

Figure 2.1.2: U.S. Unemployment and Participation Rate (%)

Source: Refinitiv, TradingKey

2.2 Weak Employment Strengthens Fed's Rate Cut Momentum

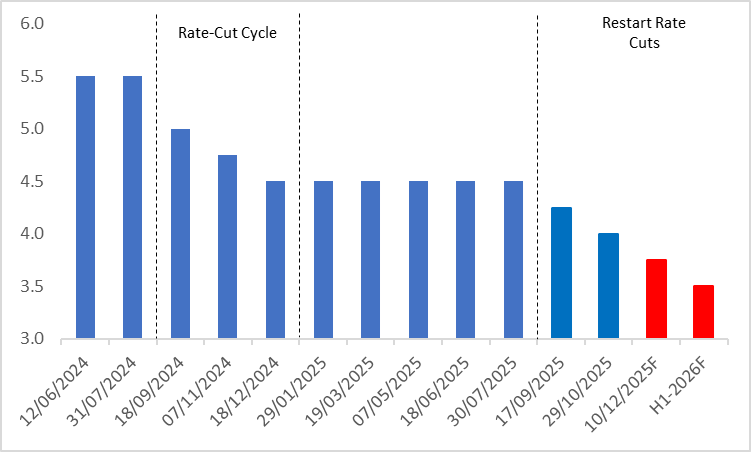

While voices supporting a December rate cut within the Federal Reserve have weakened, with market pricing for such a move falling below 40%, the likelihood of successive rate cuts by the end of this year and early next year will increase if nonfarm payroll data from September and onward continues to soften (Figure 2.2). The core signals of a weak labour market—disappointing job growth, a surge in layoffs, and a decline in both labour supply and demand—will directly trigger the Federal Reserve's risk prevention and control mechanism. Persistently weak employment dampens economic growth momentum, and without intervention, it could trigger a chain reaction leading to recession. Fed officials have explicitly defined rate cuts as a "risk management measure," and downside risks in the labour market have become a key consideration for policy adjustments. After all, a cooling labour market directly curbs consumption and investment, intensifying downward pressure on economic activity.

From the perspective of balancing policy objectives, weak employment and under-controlled inflation have created a favourable window for interest rate cuts. While core CPI and PCE remain above the 2% target, Federal Reserve officials view tariff-driven goods inflation as a one-time shock, and slowing employment is easing the risk of a wage-price spiral. Interest rate cuts serve as an "insurance measure" to support employment; against the backdrop of controllable inflationary pressures, prioritising the prevention of employment deterioration may be a reasonable choice.

Furthermore, the sustained weakness in employment data has reinforced market expectations for accommodative policies, forming a positive cycle of "weak data → rising expectations → policy response." Following the release of soft employment data, the probability of interest rate cuts increases — this market consensus has pressured the Federal Reserve to stabilise economic expectations through actual rate cuts. Historical experience also shows that significant weakness in the labour market often precedes a sharp decline in economic growth. The Federal Reserve needs to lower financing costs via rate cuts, stimulate corporate hiring and investment, and block the transmission path of recession.

Figure 2.2: Fed Policy Rate (%)

Source: Refinitiv, TradingKey

2.3 Interest Rate Cuts Are Bullish for U.S. Stocks

Sustained interest rate cuts, especially the current preventive rate cuts, are bullish for the U.S. stock market through three core mechanisms: improving corporate profitability, guiding capital flows, and stabilising market expectations. Preventive rate cuts occur when the economy has not fallen into recession and corporate profitability remains strong, featuring significant policy forward-looking. First, rate cuts directly reduce corporate financing costs. Companies can allocate the saved interest expenses to R&D and capacity expansion, which not only improves profitability but also strengthens valuation support—highly leveraged and growth-oriented enterprises benefit particularly significantly.

Second, declining interest rates lower the yield of low-risk assets such as bonds, driving capital to shift from fixed-income assets to the stock market. This injects incremental liquidity into the broader market and pushes the valuation upward. Meanwhile, interest rate cut signals convey the central bank’s determination to stabilise the economy, effectively curbing the market risk premium and alleviating investor panic. Historical data fully validate this logic — after the Federal Reserve’s preventive rate cuts in 1995, 1998, and 2019, both the S&P 500 and Nasdaq indices recorded significant gains. Additionally, the accommodative environment will activate merger and acquisition (M&A) transactions, facilitating industry consolidation and optimal resource allocation, and providing extra upward momentum for the stock market.

At the sector and individual stock levels, the Federal Reserve's ongoing interest rate cuts will benefit interest rate-sensitive sectors and those with confirmed growth prospects by reducing financing costs and easing liquidity. Based on historical patterns and current market characteristics, the core beneficiary sectors and leading stocks are as follows: Technology stocks stand out as the biggest winners — rate cuts lower R&D and financing costs while boosting the discounted value of future cash flows, with the AI and semiconductor tracks being particularly prominent. Leading enterprises include NVIDIA (NVDA), Apple (AAPL), and Tesla (TSLA). After the 2019 preventive rate cuts, the Nasdaq surged sharply, and these companies have maintained their leading position.

REITs (Real Estate Investment Trusts) directly benefit from lower financing costs and enhanced attractiveness of rental yields. Leaders like Prologis (PLD) and American Tower (AMT) are expected to deliver strong performance amid the interest rate cut cycle. Driven by the dual tailwinds of a weaker U.S. dollar and falling real interest rates, gold mining stocks such as Newmont (NEM) and Barrick Gold (GOLD) will likely show significant earnings flexibility. Discretionary consumer and high-leverage sectors are undergoing recovery: General Motors (GM) and Ford (F) in the automotive industry, along with United Airlines (UAL) in the aviation sector, are gaining from reduced auto loan pressure and lower financing costs. All these sectors align with the core logic of "liquidity easing + valuation recovery" during the rate cut cycle. With technological barriers and market share advantages, leading enterprises may become key targets for capital focus.

3. Scenario 2: Job Market Hits Bottom and Recovers

3.1 Reasons for Employment Recovery

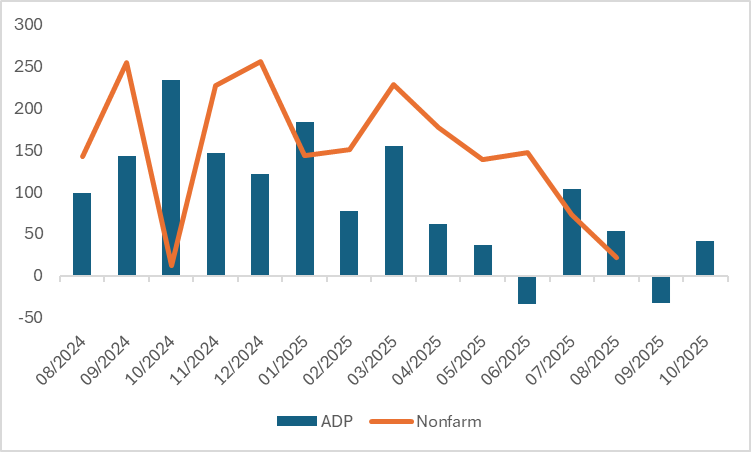

Scenario 2 assumes that U.S. nonfarm payrolls will start to increase in September and onwards, with the job market hitting bottom and recovering, and this possibility stems from two key reasons: first, support from ADP employment data signals—since October last year, ADP nonfarm payrolls have moved downward, even turning negative in September this year, but the latest October data shows signs of recovery in private sector employment (Figure 3.1), and if this recovery trend persists, it will boost nonfarm payrolls in the coming months; second, the dual drivers of industrial investment and structural growth—sustained fiscal policy efforts, combined with massive private sector investments in semiconductors, clean energy and other fields, will directly drive steady employment growth in manufacturing and non-residential construction, while the AI boom is spurring new job growth with expected significant surges in demand for positions in IT, data analysis and related sectors, and service industries such as healthcare and education maintain rigid demand, acting as stabilizers for the job market.

Third, restarting the interest rate cut cycle unlocks easing benefits. Since 17 September this year, the Federal Reserve has officially launched a new interest rate cut cycle. To date, the benchmark interest rate has been reduced by 50 basis points. Interest rate cuts will continuously lower corporate financing costs, particularly benefiting small and medium-sized enterprises (SMEs) in expanding recruitment. Meanwhile, the decline in mortgage rates will drive growth in residential investment, indirectly boosting employment demand in the construction sector. In short, lower interest rates create a favourable environment for employment expansion.

Fourth, consumption resilience and the wealth effect are stimulating labour demand. In recent years, as U.S. stocks, cryptocurrencies, and gold prices have repeatedly hit record highs, U.S. household net worth has surged significantly. The wealth effect is expected to support sustained consumption recovery. The positive cycle of "consumption → employment → wages" may emerge, and contact-intensive industries such as leisure and hospitality, as well as commercial services, may accelerate recruitment to fill vacancies. The steady performance of the consumer market will continue to drive labour demand in the service sector.

Figure 3.1: U.S. ADP Nonfarm Employment and Nonfarm Payrolls (000)

Source: Refinitiv, TradingKey

3.2 Employment Recovery Supports US Stocks

Recently, multiple Federal Reserve officials have indicated a preference for pausing accommodative monetary policy. Vice Chair Philip Jefferson also said on 17 November that as interest rates approach neutral levels, subsequent rate cuts should be gradual. If Scenario 2 materialises, the recovery in the job market will constrain the scale of rate cuts, implying that this cycle of rate cuts may be drawing to a close. On this sole basis, the development would weigh on US stocks.

However, the recovery in employment is inherently bullish for U.S. stocks. Looking ahead, a warmer labour market will benefit the broader U.S. stock market through two core dimensions: economic fundamentals and market capital flows. A rebound in employment directly reflects the resilience of the U.S. economy, as new job additions and a declining unemployment rate will strengthen market confidence in economic recovery. Consumption accounts for approximately 70% of U.S. GDP, so stable employment translates to higher household income and stronger purchasing power, which will directly drive corporate revenue growth and improve profit expectations. On the capital front, positive employment data will attract global capital inflows into U.S. stocks. It will also reinforce expectations of an economic "soft landing" and enhance the relative attractiveness of U.S. stocks compared to assets like bonds. With the resonance of multiple factors, the recovery in employment will provide sustained support for the broader U.S. stock market.

At the sector and individual stock levels, the recovery of the U.S. job market will most benefit the consumer staples, healthcare, and financial sectors. Leading stocks in these areas are likely to see simultaneous growth in earnings and valuations. Specifically, in the consumer staples sector, improved employment will boost household income and consumption willingness, benefiting areas such as retail. Amazon (AMZN), a sector leader, is expected to see steady growth in retail orders amid consumption recovery; discount retailer Dollar General (DG) will benefit from increased spending by low-income groups.

The healthcare industry is a consistent driver of job growth, with the employment recovery simultaneously boosting industry demand and labour expansion. This bodes well for industry leader Johnson & Johnson (JNJ) in the medium to long term, as its diversified healthcare businesses will benefit from rising industry demand. In the financial sector, stable employment underpins economic resilience, favouring the expansion of financial services. JPMorgan Chase (JPM) and Goldman Sachs (GS) will see reduced credit default risks amid improved employment conditions, while stable policy expectations will support profit growth in their investment banking and wealth management businesses.

4. Conclusion

In summary, from a medium-term perspective, whether the strength or weakness of nonfarm payroll data starting from September will be beneficial to the U.S. stock market. A sustained softening of the U.S. job market will push for more aggressive interest rate cuts, thereby boosting U.S. stocks. If the job market rebounds, it will support economic recovery and similarly underpin U.S. stock performance. Therefore, passive investors may consider U.S. broad-market ETFs such as SPY and QQQ. For active investors: if anticipating rate-cut trades driven by slowing employment, focus on tech giants including NVIDIA (NVDA), Apple (AAPL), and Tesla (TSLA); REITs sector leaders like Prologis (PLD) and American Tower (AMT); gold mining companies such as Newmont (NEM) and Barrick Gold (GOLD); as well as companies in discretionary consumption and high-leverage industries—General Motors (GM), Ford (F)—and airline sector player United Continental Holdings (UAL). If expecting a job market recovery to enhance U.S. economic resilience, prioritise consumer staples stocks like Amazon (AMZN) and Dollar General (DG); healthcare giant Johnson & Johnson (JNJ); and financial sector leaders JPMorgan Chase (JPM) and Goldman Sachs (GS).

It is important to note that while we hold a mid-term bullish view on U.S. stocks, the job market and Federal Reserve monetary policy exert a countervailing force — a recovery in employment will prompt the Fed to slow its rate cut pace, while the opposite may accelerate rate cuts, leading to continued sharp short-term volatility in U.S. stocks. However, any significant pullback would present an excellent entry opportunity for mid-to-long-term investors.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.