U.S. CPI Falls Short of Expectations for Fourth Month – Why Isn’t Trump Tariffs’ Inflationary Impact Showing?

TradingKey - Contrary to widespread concerns that Trump tariffs would push inflation higher, the U.S. May CPI report revealed a surprisingly mild inflation reading, marking the fourth consecutive month of below- or in-line-with-expectations data — prompting analysts to reassess the true impact of trade policy on price pressures.

On Wednesday, June 11, the U.S. Bureau of Labor Statistics released the May Consumer Price Index (CPI) report:

Headline YoY CPI: +2.4% (vs. forecast +2.4%, previous +2.3%)

MoM CPI: +0.1% (vs. expected and prior +0.2%)

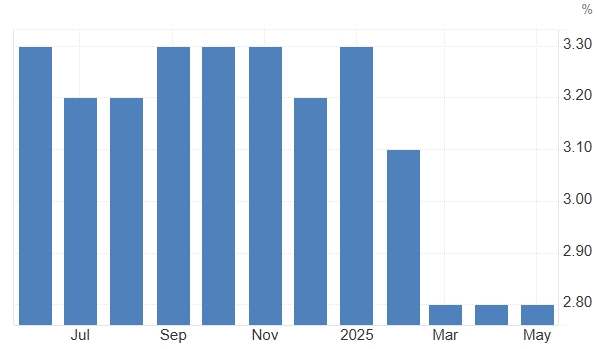

Core CPI YoY (excluding food and energy): +2.8% (vs. forecast +2.9%, previous +2.8%) — remaining at the lowest level since March 2021

Core MoM CPI: +0.1% (vs. expected and prior +0.2%)

The softness was driven by declines in prices across categories such as used and new cars, apparel, airfares, and hotel rates, while persistently weak energy prices also kept inflation in check.

U.S. Core CPI YoY, Source: Trading Economics

Why Isn’t Trump’s Tariff Policy Pushing Up Inflation?

The unexpectedly mild inflation print contrasts with earlier forecasts that tariff-driven cost pass-through would spark a renewed inflationary surge. Analysts have proposed several possible explanations:

1. Inventory Build-Up Ahead of Tariff Implementation

Many companies stockpiled goods ahead of tariff hikes, delaying the inflationary effects. This inventory buffer has helped keep shelves full and prices stable — for now.

Fitch economists noted that a rise in core goods inflation in the months ahead still looks very likely.

2. Tariff Delays and Policy Uncertainty

Repeated delays in implementing new tariffs have given businesses more time to adjust pricing strategies and absorb costs internally rather than passing them on to consumers.

3. Deflationary Pressures in Key Sectors

Sectors like used vehicles, leisure services, and durable goods are experiencing deflationary trends, reflecting weaker consumer confidence and cautious spending behavior — which is offsetting any inflationary pressure from tariffs.

Bloomberg economists added, “Ultimately what matters is the trade war’s net impact on inflation — and so far it has been disinflationary. Still, we think the Fed’s internal forecasts point to higher inflation in the months ahead.”

4. Consumer Caution Amid Economic Uncertainty

Despite strong labor market data, households remain cautious about future income growth, leading to lower demand elasticity and limited pricing power for retailers and manufacturers.

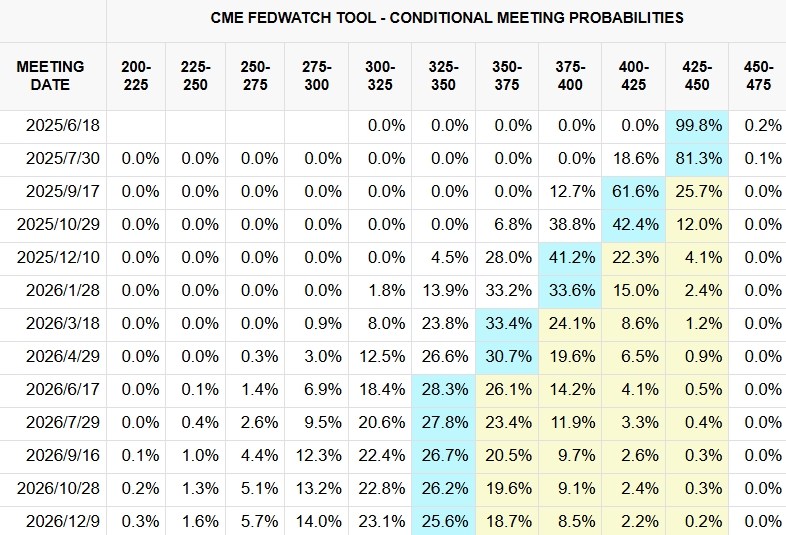

Market Reaction: More Bets on Fed Rate Cuts

Following the release of the CPI report, traders increased bets that the Federal Reserve will cut interest rates twice in 2025, with cuts expected in both September and December, each by 25 basis points.

Fed Rate Cut Bets, Source: CME

However, CICC expects that the June FOMC meeting — set for June 19 — may include a slight upward revision to inflation forecasts, and Fed Chair Jerome Powell is likely to adopt a hawkish tone during his press conference.

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.