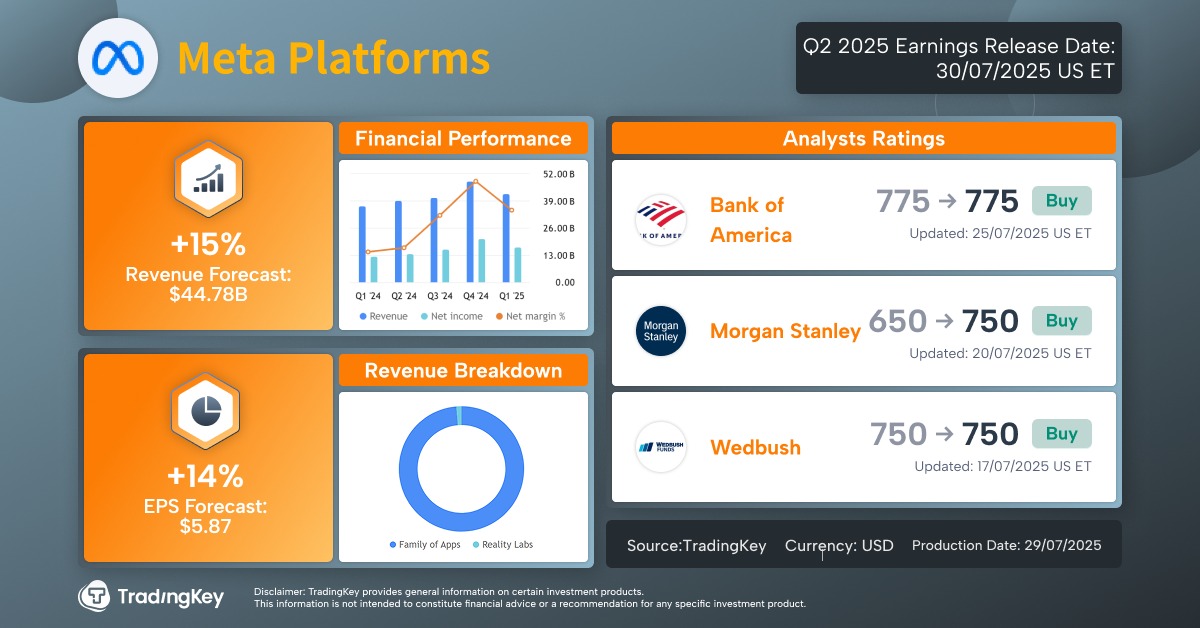

What to Expect From Meta Q2 Earnings: AI Push, Ad Strength — But Can Profitability Hold?

TradingKey - Meta Platforms (META), the parent company of Facebook, Instagram, and WhatsApp, will release its Q2 2025 earnings after the U.S. market close on Wednesday, July 30. After nine consecutive quarters of beating expectations, analysts expect another strong performance — driven by AI-powered advertising growth — but rising costs from Meta’s aggressive AI investments could pressure profit margins.

According to Bloomberg consensus estimates, Meta is projected to report:

- Revenue: $44.71 billion, up 14% YoY

- Adjusted net income: $19.92 billion, up 10% YoY

- EPS: $5.85

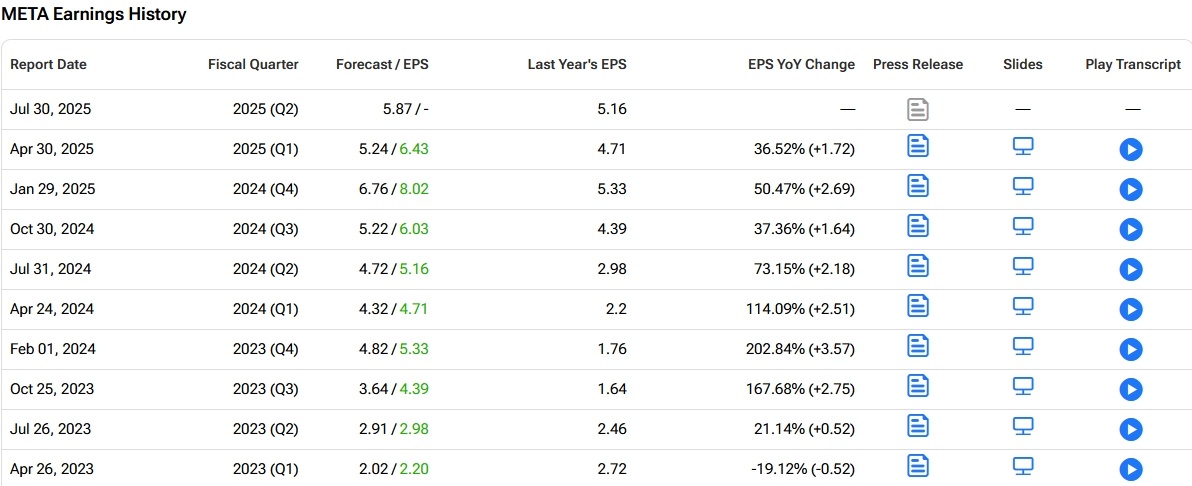

Tipranks data shows that since Q1 2023, Meta has exceeded EPS expectations for nine straight quarters, with eight consecutive quarters of year-over-year EPS growth — a testament to its strong execution and profitability.

Meta Earnings Per Share History, Source: Tipranks

AI-Driven Ads Continue to Deliver

In Q1 2025, advertising revenue accounted for ~98% of total revenue ($42.31 billion) and grew 16% YoY. Analysts expect Q2 ad revenue to maintain double-digit growth, though at the slowest pace in two years.

Bloomberg analysts attribute the sustained strength to AI-driven ad targeting and pricing, which are improving return on ad spend (ROAS) for advertisers.

Deutsche Bank highlighted tools like Advantage+ — Meta’s AI-powered ad automation suite — as a core driver of revenue growth. These tools are enhancing ad performance and increasing advertiser retention.

Deutsche Bank expects Q2 ad revenue to rise 1% from Q1, with acceleration likely in Q3.

TradingKey Analyst Petar Petrov noted that with Alphabet’s recent beat driven by strong ad growth, investors should remain optimistic about Meta’s ability to deliver similar momentum.

All-In on AI — But at What Cost?

While revenue growth remains robust, Wall Street is increasingly focused on costs and profitability.

CEO Mark Zuckerberg has made it clear: Meta is going all-in on AI, aiming to build the world’s most advanced artificial intelligence infrastructure.

Recent moves include:

- $14.3 billion acquisition of a 49% stake in AI startup Scale AI — Meta’s second-largest deal after WhatsApp

- Plans to invest hundreds of billions of dollars in AI infrastructure, including gigawatt-scale data centers. The first such “supercluster”, Project Prometheus, is expected to come online in 2026

- A $100 million war chest to recruit top AI talent from OpenAI, Apple, Google, DeepMind, and GitHub

This aggressive spending has raised concerns about margin sustainability.

Deutsche Bank has revised its expense guidance, now expecting total 2025 expenses to range between $113 billion and $118 billion.

Meta previously forecast $64–72 billion in capital expenditures for 2025. Wells Fargo projects 2026 capex could reach $76.7 billion.

Meta’s Q1 2025 operating margin was 41%, up from 38% in Q1 2024 — but analysts fear this peak may not last.

Jefferies warned that rising AI-related hiring and infrastructure costs will weigh on profitability.

D.A. Davidson noted that while Meta’s AI push is a long-term competitive necessity, it comes with near-term margin trade-offs.

Canaccord forecasts that Meta’s Q2 operating margin could fall below 40%, to around 37.5% — a notable drop from recent highs.

Is Meta Still a Buy?

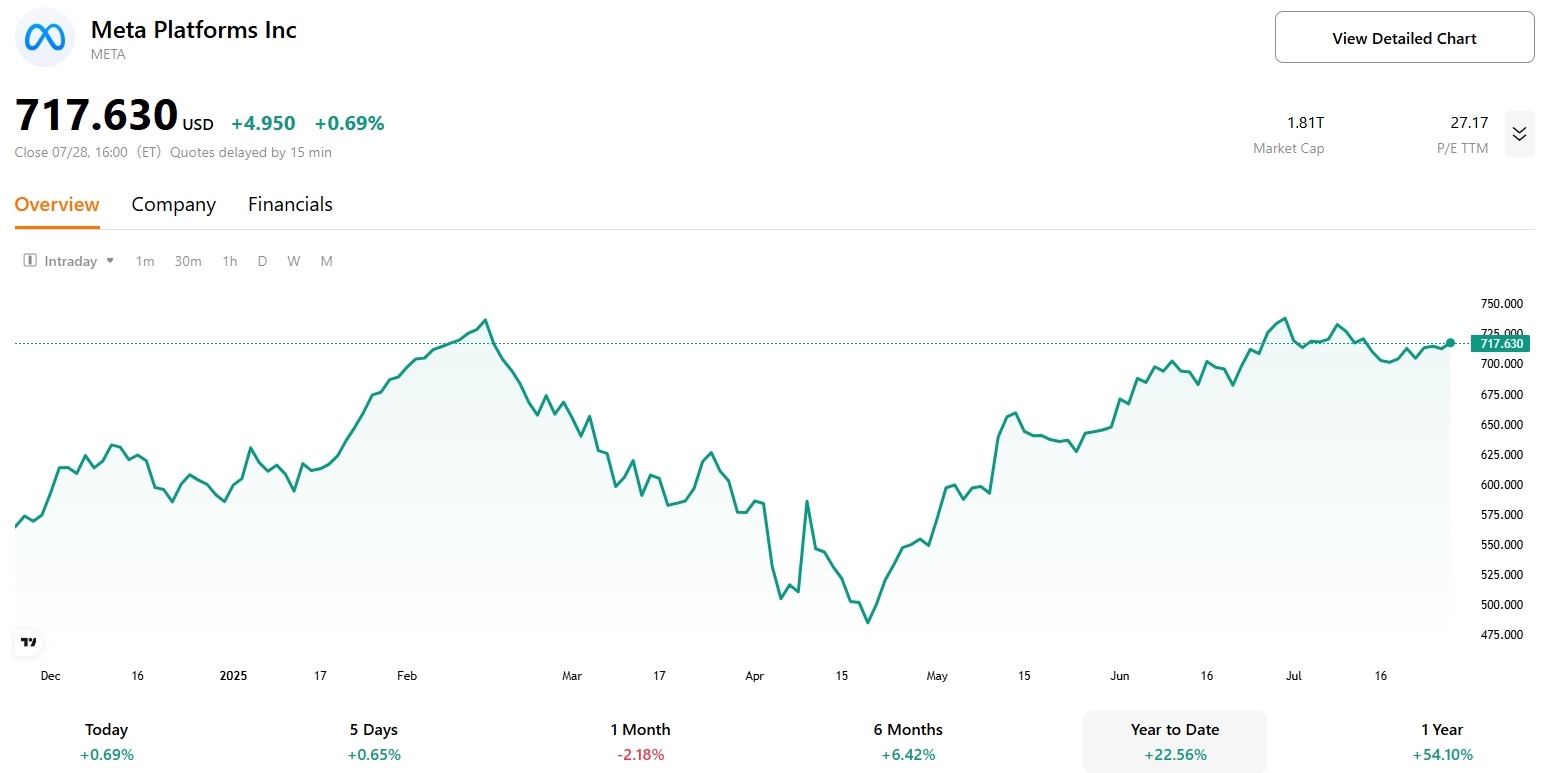

Year-to-date in 2025, Meta’s stock has risen 22.56%, second only to NVIDIA (+31.62%) among the Magnificent 7, and well ahead of the S&P 500 (+8.64%) and Nasdaq (+9.67%).

As of writing, Meta closed at $717.63. According to TradingKey, the average analyst price target is $748.94 — implying about 5% upside.

Meta Stock Performance in 2025, Source: TradingKey

Among 71 analysts covering the stock:

- 23 rate it Strong Buy

- 40 rate it Buy

- Only 8 hold or sell

Analysts Stay Bullish

- Mizuho Securities raised its target from $750 to $800, maintaining a Buy rating

- Goldman Sachs lifted its target from $690 to $775, keeping Buy

- Morgan Stanley increased its target from $650 to $750, also Buy

Morgan Stanley said Meta’s core growth algorithms, powered by advanced GPU-accelerated machine learning, will continue to drive higher user engagement and monetization.

Deutsche Bank added that AI enhancements are leading to improved user activity on Facebook and Instagram — setting the stage for sustained ad volume growth in the years ahead.

Recommended Articles