Oscar Health’s Unexpected Profit Surge

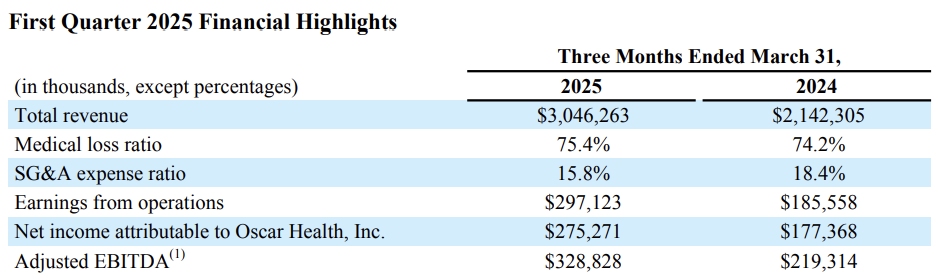

- Revenue grew 42% year-over-year to $3.05 billion in Q1 2025, with net income rising to $275 million.

- SG&A ratio dropped to a record low of 15.8%, supporting a 60% year-over-year increase in operating income to $297 million.

- Membership surged 41% to 2.04 million, driven by ACA individual and small group plans amid the exit from Cigna+Oscar.

- Despite high growth, Oscar trades at over 30x forward earnings—200% above sector median—raising valuation sustainability concerns.

TradingKey - Oscar Health (OSCR) assembled an unlikely reversal with 42% YoY revenue growth to $3.05 billion in Q1 2025 and net income of $275 million, which represents a remarkable $98 million year-over-year improvement. This performance, along with a record low SG&A ratio at 15.8% and rising operating margin (9.8%), is indicative of an insurer rounding the profitability corner.

Nevertheless, valuation measures raise significant questions. A forward P/E multiple above 30 reflects aggressive hopes, significantly above sector medians by nearly 182%. Oscar’s business model is growth-minded, but at what premium are investors paying for future margin expansion?

Source: Oscar Health First Quarter 2025 Financial Results

A closer examination reveals that Oscar’s story is no longer merely that of user growth or cool tech disruption. It now becomes that of execution discipline, leverage of capital, and operating efficiency. Its dual personality, half insurer, half health tech, positions it at the intersection between consumer healthcare and AI-native operational innovation.

In theory, that translates into long-term operating leverage. In practice, it depends on Oscar’s ability to counteract the risks of regulation, member turnover brought on by changes in enrollment policy, and medical service cost inflation. The balance sheet is sound with $4.9 billion in cash and investments. Investor scrutiny is, nevertheless, likely to escalate since valuation multiples stretch while regulatory and competitive overhangs persist.

Health-Tech Flywheel behind the Monetization of Oscar

Oscar Health's model is that of a vertically integrated, tech-enabled health insurer for individual and small group ACA markets with an aspiration to power third-party health plans with its +Oscar tech platform. Its model is centered upon a proprietary full-stack tech platform facilitating digital-first member experiences, care routing enabled by AI, and simplified cost structures. Virtual care, claim integration, and data analytics are more than buzzwords and are ingrained structurally within the model.

Q1 2025 membership grew by 41% YoY to 2.04 million effectuated members, facilitating top-line growth. Most growth came from individual and small group plans, with the previous Cigna+Oscar co-branded plans now effectively discontinued, officially symbolizing movement toward direct platform scale. This focus complements the deployment of capabilities like Virtual Urgent Care live chat, decreasing provider response time by 90% and increasing provider efficiency by 28%. These are the kinds of data points that indicate Oscar’s approach to optimize human capital with software leverage, reminiscent of tech-natsu disruptors.

.jpg)

Source: Oscar Health First Quarter 2025 Financial Results

Here, the protection that Oscar’s $4.9 billion liquidity pool provides, with $1.5 billion stashed out in insurance subsidiary capital and surplus, buys time. Their cash burn has flipped over into cash build, evidenced by record first-quarter operating cash flow of $878 million, up from last year’s $634 million. That gives strategic flexibility, whether for data/AI acquisitions, scaling +Oscar B2B businesses, or member retention investment. The test, though, is that Oscar must scale these tech-enabled efficiencies before margin pressures from high inpatient utilization or risk-adjusted payable resets diminish operating leverage.

Cost Leverage Faces Competitive Headwinds

Oscar’s SG&A ratio shrank from 18.4% to 15.8% during Q1 2025 due to fixed cost leverage, and declining exchange fee rates are such a point of no return. While traditional insurers struggle to shrink administrative overheads without compromising service quality, Oscar’s software-driven stack allows unit cost deflation amidst top-line acceleration. Operating income increased 60% YoY to $297 million, with adjusted EBITDA having hit $329 million, a clear indication of compounding efficiency. These advantages are, however, diluted partially by a 120 bps expansion in medical loss ratio (MLR), now 75.4%, due to what management attributes to a $31 million unfavorable prior year adjustment in risk adjustment payables.

.jpg)

Source: Oscar Health First Quarter 2025 Financial Results

.jpg)

Source: Oscar Health First Quarter 2025 Financial Results

That trade-off between enhancements at the operations level and fluctuation in medical costs remains at the center of Oscar’s investment case. Underwriting risk, proper pricing, and utilization control through digital engagement are theoretically better abilities than legacy insurers. But Oscar’s competition is vertically integrated giants like UnitedHealth (UNH) and Elevance (ELV), which possess deeper care networks, pharmacy benefits scale, and leverage at the legislative level. Oscar’s own differentiator isn’t all tech; it’s whether that tech measurably shifts the cost curve over time.

Looking out, Oscar envisions full-year operating earnings between $225 and $275 million and an increase in adjusted EBITDA by $140 million across that range. SG&A ratios are viewed as stabilizing between 17.6% and 18.1%, with MLR guidance between 80.2% and 81.2%. These ranges represent modest deterioration from the first-quarter standout and are consistent with seasonality and the regulatory headwinds that are muddying margin visibility. The strategic focus should turn toward stabilizing membership with the dissipation of the tailwinds during the special enrollment season, with stabilizing per-member economics intact.

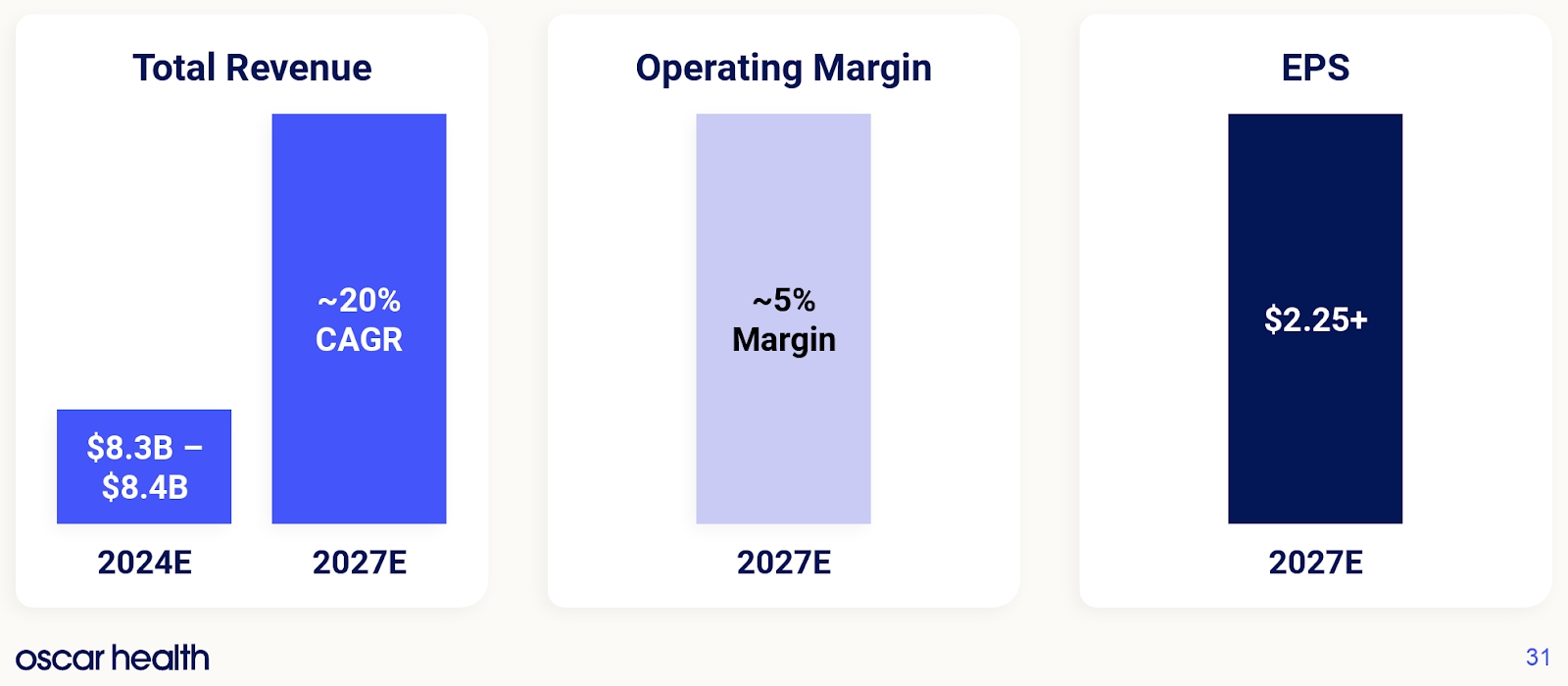

Oscar Health is projecting a compelling financial trajectory heading into 2027. Building on 2024’s revenue base of $8.3–$8.4 billion, the company expects to grow at a ~20% compound annual rate, signaling strong momentum in both market expansion and member growth. By 2027, Oscar aims to achieve an operating margin of approximately 5%, a notable shift toward greater efficiency and scale. Perhaps most striking, EPS are projected to exceed $2.25, underscoring a confident pivot toward consistent profitability. If these targets are met, Oscar will have successfully evolved into a leaner, more mature player in the health insurance space.

Source: Investor Day

Risk Pulse: Regulatory Friction, Margin Volatility, and Competitive Gravity

Oscar’s closest-term risk is policy-based membership swings. Special enrollment phaseout should decrease Q3–Q4 membership from the Q1 high of 2.04 mm to an estimated year-end 1.8 mm. While management believes economics are fine on a per-member basis, fewer members equals lower scale benefits and even a reversal of SG&A leverage. Additionally, the medical loss ratio, already stressed by risk adjustments from the prior year, could escalate should utilization stay at the inpatient level or distributions due to regulation impact risk pools.

Another threat is margin exposure. Even with SG&A improvements, Oscar’s adjusted EBITDA margins are exposed to variations in medical costs that are only partially controlled. In the case that pharmacy savings taper or prevalence among chronic conditions rises, the 9.8% operating margin becomes a ceiling rather than a floor. Additionally, valuation multiples for Oscar imply that it not only has to grow but also grow efficiently and defensibly, which imposes huge execution pressure on its digital platform.

Finally, competitive risk is understated. Despite its tech-native status, Oscar lacks UnitedHealth’s scale, CVS/Aetna’s vertical integration, or the lobbying muscle of Elevance. Such incumbents’ increased investment in utilization control or member interaction with AI/ML could blur Oscar’s differentiation more than we expect. Its +Oscar tech platform, promising as it is, has never yet become a revenue engine equivalent with its core business, limiting diversification optionality.

Conclusion: Execution Is the Key to Valuation Rationale

Oscar Health transformed from a speculative disruption play into a money-making operator with real margin growth and cash-flow leverage. Its Q1 2025 beat reaffirms its execution strategy but escalates investor expectations. The stock now embeds recurring operating improvements and factors in modest regulatory surprises, execution, and growth is the next litmus test. While swapping valuation risk for real earnings potential, the following quarters will reveal whether Oscar becomes a rugged compounder or gives way to margin oscillations and policy friction.

Copyleaks Report: https://app.copyleaks.com/report/au5xbyz23o4iui5u/preview?key=vynwdnrii7xvo4ip&viewMode=one-to-many&contentMode=text&sourcePage=1&suspectPage=1&showAIPhrases=false&alertCode=suspected-ai-text

.png)

Get Started

Recommended Articles