HPE’s Hidden Pivot: From Infrastructure to Intelligence Amid AI and Margin Turbulence

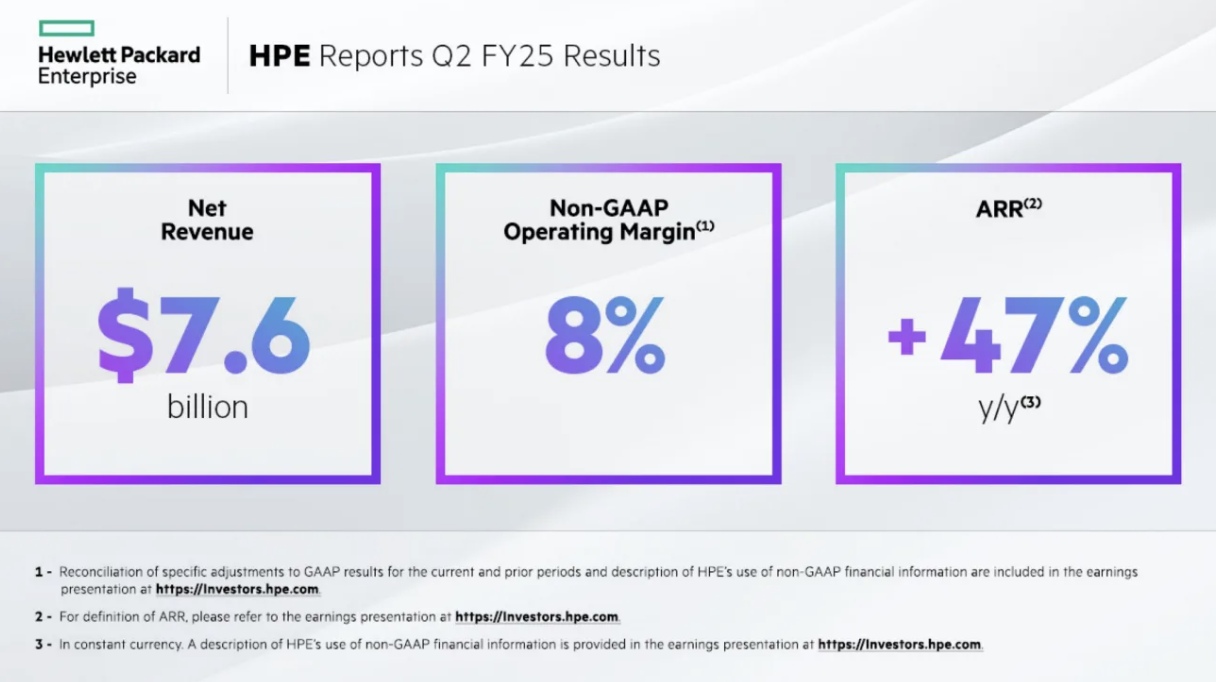

While the market still discounts Hewlett Packard Enterprise (HPE) as a legacy infrastructure vendor, Q2 FY2025 results reveal a mounting misaligned perception. On the face of it, HPE’s 5.9% Server segment margin, a decline from 11.0% YoY, and an anemic non-GAAP operating margin of only 8% could be disappointing. And the headline GAAP EPS of -$0.82, triggered by a $1.4 billion goodwill impairment, further fuels that skepticism.

Source: HPE Condensed Consolidated Statements of Earnings Q2 FY25

But beneath the impairment and segment margin dilution is a quiet transformation: HPE is evolving into an AI-native, software-driven hybrid cloud operator with compounding platform economics. Critically, HPE brought in more than $1 billion in AI systems in Q2, versus $900 million in Q1, and finished the quarter with an AI backlog of $3.2 billion. GreenLake ARR reached 47% YoY growth at $2.2 billion, 75% of which now comes from higher-margin software and services.

Source: HPE

These numbers reflect not only expansion but also a fundamental model transition. Hybrid Cloud sales rose 15% YoY, fueled by triple-digit Alletra MP gains, now integrated more and more into AI pipelines through SDKs such as the X10000 for NVIDIA’s AI suite. Intelligent Edge sales rose 8% YoY, fueled by triple-digit Wi-Fi 7 orders and an expanding AI-linked networking stack.

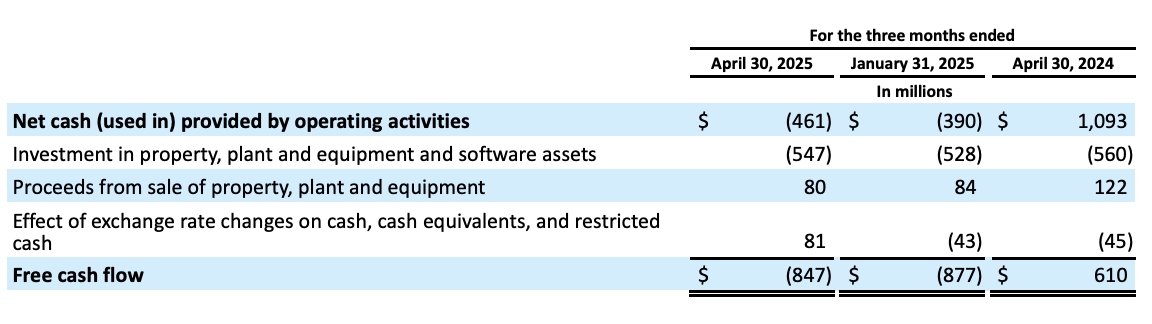

In spite of negative free cash flow of $847 million owing to inventory normalization and AI pre-shipment dynamics, HPE reaffirmed FY25 FCF guidance of $1 billion and guided Q3 sales to the range of $8.2–8.5 billion, suggesting robust AI-related recognition. HPE's own transformation into a standalone company focused on intelligent, modular platforms presents asymmetric optionality while the Juniper acquisition lingers in limbo.

From Compute Commodity to AI-Centric Workloads: The Server Transformation

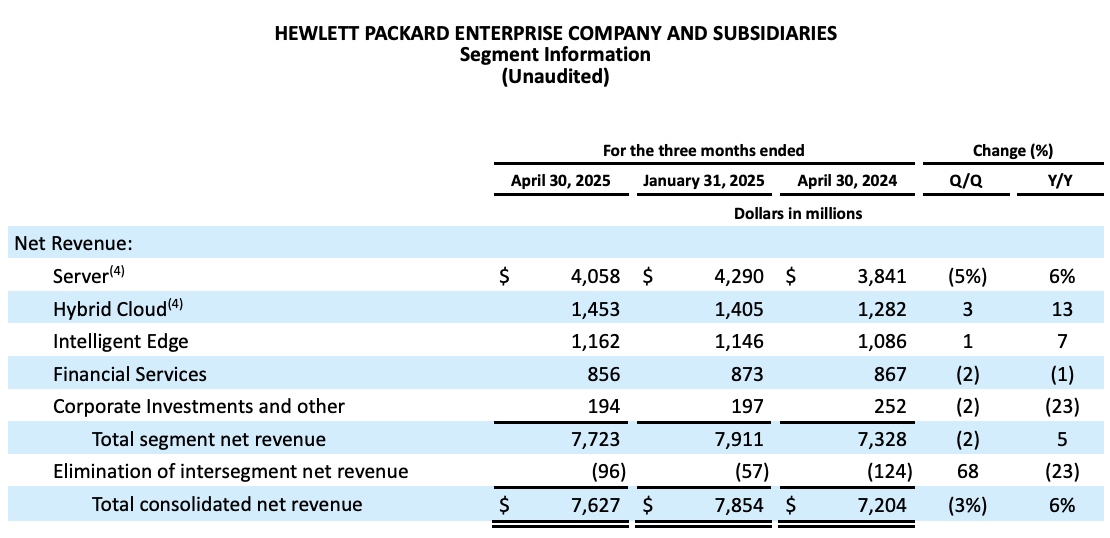

The Server segment has been HPE's revenue driver long-term, but in Q2 FY25, we began to see signs of deeper transformation versus stabilization. Server sales increased 6% YoY to $4.06 billion, but profitability was squeezed hard from 11.0% to 5.9% due to the clearance of backlog and corrective discounting.

Source: HPE Condensed Consolidated Statements of Earnings Q2 FY25

Yet, the internal dynamics are different. AI systems sales were over $1 billion, 10%+ over internal expectations, supported by enhanced readiness of customers and prepayment-linked shipment increases. This volume also covered sequential dips in general-purpose computing.

Most importantly, HPE strengthened deal desk controls and forward-costing analytics that should realign margin achievement to a 10% exit rate in Q4. Inventory levels were cut by $500 million QoQ, indicating a shift from speculative component stocking to demand-driven AI system fulfillment, especially in sovereign compute and Grace Blackwell installations.

HPE's segmental development is underappreciated. Gen12 servers began shipping in Q2 and will scale in H2 with improved AUPs and benefits from standardization. In parallel, Blackwell-related opportunities are experiencing prepayment requirements in advance of inventory purchase, decreasing working capital pull, and mitigating write-down exposure.

This discipline is a stark contrast to hyperscaler competitors sacrificing returns in pursuit of volume. As sovereign AI programs scale and enterprise buyers are ever more focused on “time to value,” HPE's vertically integrated AI servers provide differentiated scale-to-deploy benefits that are just starting to enable monetization leverage.

Hybrid Cloud and Intelligent Edge: Subsystems Becoming Flywheels

HPE's Hybrid Cloud and Intelligent Edge segments are becoming more and more the revenue underpinning of its transition architecture. Combined, the two units contributed ~$2.6 billion of Q2 revenue, an 11% YoY increase, and earned greater segmental operating margins compared to the Server business, demonstrating their flywheel economics.

Source: TipRanks

Hybrid Cloud revenues increased 15% YoY to $1.45 billion, fueled by triple-digit growth in Alletra MP storage and a 300+ sequential increase in new logos. Alletra’s disaggregated, multi-protocol design is now being packaged into NVIDIA AI SDKs, positioning it at the center of inferencing pipelines. While this move towards SaaS-like subscription storage delays some revenues, it increases deferred software revenue and improves profitability materially in the long term. Segment margin increased 440 bps YoY to 5.4% despite increased compensation and marketing expenses.

Meanwhile, Intelligent Edge revenue totaled $1.16 billion, an 8% YoY increase. Particularly, operating margins were at 23.6%, the highest in HPE’s major segments. Orders were fueled by triple-digit expansion in Wi-Fi 7 and campus/data center switching strength. Embedding Aruba’s Central platform in on-prem zero trust deployments is a signal of a shift towards security-focused, AI-controlled network fabrics.

Source: HPE Condensed Consolidated Statements of Earnings Q2 FY25

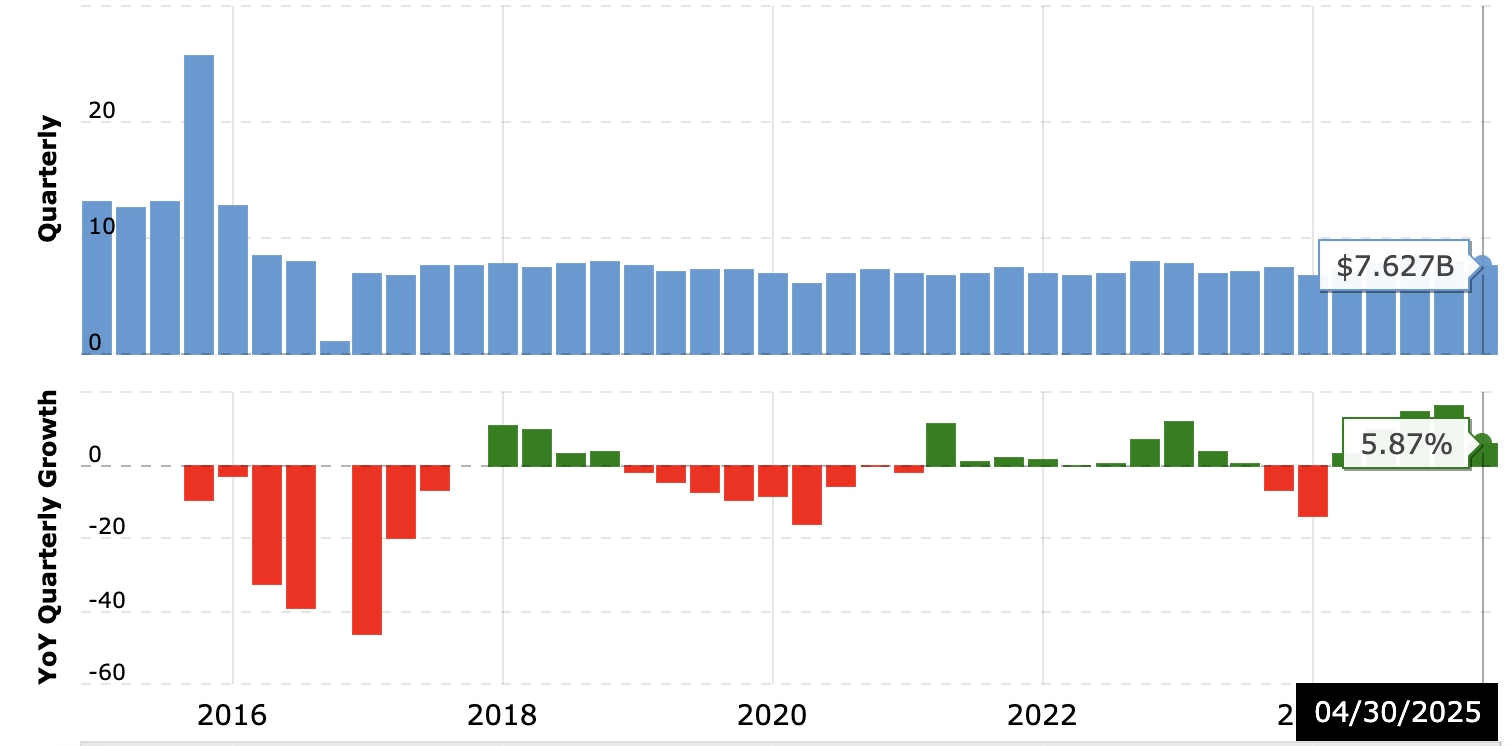

GreenLake is being bundled with those deployments, growing ARR from networking and elevating customer lifetime value. Notably, software and services now account for 75% of HPE's ARR, an increase of 700 bps YoY, underpinned by GreenLake Flex subscriptions. This implies a further reconstitution in revenues towards recurring, higher-margin models with HPE staying in a category that is rapidly becoming ServiceNow or Snowflake-like, but still at an infrastructure-based stage.

Source: MacroTrends

Valuation Reset: Re-Rating Potential and Margin Expansion

HPE's valuation is still based on historical industrial standards instead of forward-looking platform metrics. Shares are priced at ~10x forward non-GAAP EPS ($1.78-$1.90 FY25E) and <1x EV/sales, in spite of 47% YoY ARR expansion and a 75% recurring software/services composition. This discount is still intact due to short-term headwinds, including the $1.4 billion goodwill impairment and negative Q2 GAAP EPS, instead of showing any structural weakness.

However, a number of signs point towards an impending re-rating. First, H2 gross margin is poised to recover, with Q4 expected to be above 30% (vs. 29.4% in Q2), on a mix shift away from legacy compute. Server segment margins will increase from 5.9% to ~10% while Hybrid Cloud is expected to move out of FY25 in the high single digits.

Second, CapEx-weighted AI deployments are switching to revenue ahead of expectations, with Q3 to feature one of the largest GP200 deployments in the world. This will speed cash conversion and mitigate inventory pull, taking FCF to the $1 billion full-year guide.

Third, the Juniper acquisition, while delayed by litigation over regulations, provides an optionality layer. If it goes through, $450 million of synergies can increase operating leverage meaningfully; otherwise, HPE's indication of willingness to consider alternate return of capital and portfolio steps create a path forward in either case, unlocking capital efficiency not reflected in the current price.

Relative to Dell and Lenovo, with their higher proportions of compute or third-party software-based revenues at lower margins, HPE's hybrid combination of AI-native servers, SaaS storage, and zero-trust networking commands a structurally wider margin profile. Today's valuation discrepancy presents asymmetric upside with stabilization in execution and AI backlog monetization.

Risk Considerations: Tariffs, Enforcement, and Capital Allocation

In spite of strategy advances, HPE is confronted with non-negligible dangers. Most significant is the consistency of execution, specifically in the Server segment, where margin volatility jeopardized investor perception. Although corrective maneuvers boosted pricing discipline and alignment of inventories, the benefits will not be realized until Q4, leaving H2 execution vulnerable to possible tardiness in deliveries or client turnover.

Notably, macro and regulatory uncertainties still linger. July 2025 is the deadline of the temporary tariff halt, keeping in place the residual risk of cost re-inflation. HPE experienced $0.02 in Q2 tariff impact and could experience a $0.01–$0.02 drag in H2 based on U.S. trade policy results.

In addition, the Juniper acquisition is still stuck in legal proceedings. A broken transaction could cap near-term networking synergies, while HPE does enjoy good organic growth in Intelligent Edge.

Lastly, cash flow volatility is a worry. Q2 FCF was -$847 million due in part to inventory shifts in anticipation of major AI activations. Positive FCF in Q3–Q4 is anticipated by the management, but any delay in AI conversion or client adoption could send the company beneath its target of $1 billion of FCF on an annualized basis during this year. This would put into jeopardy its credibility on returning capital, particularly with $221 million already repatriated in Q2.

Conclusion: Dilutive Margins Today, Monetization Tomorrow

Hewlett Packard Enterprise is standing at a strategic turning point: from hardware seller to platform of intelligent infrastructure. As historical segment margins suppress profitability on a GAAP-consolidated basis, Q2 results reflect significant traction in AI systems, ARR monetization, and storage integration, signs of an early-stage flywheel picking up speed.

The shift is underappreciated by the market in the short term due to transitory dilution, but normalization of margins, GreenLake expansion, and AI backlog conversion provide real valuation catalysts.

Copyleaks Report: https://app.copyleaks.com/report/mcp3ey3nhog3fdsh/preview?key=rfzcgb2ti8s4plle&viewMode=one-to-many&contentMode=text&sourcePage=1&suspectPage=1&showAIPhrases=false&alertCode=suspected-ai-text

Recommended Articles