NVIDIA Q1 Earnings Preview: China Export Ban Risks vs. Middle East “Stargate” Mega Deal

TradingKey - On Wednesday, May 28, after U.S. markets close, AI chip giant NVIDIA (NVDA.US) will release its Q1 FY2026 earnings report , drawing investor attention to two key factors that could shape the company’s performance: the impact of U.S. export restrictions on China market sales and a major new order from Stargate UAE.

Market consensus expects NVIDIA to report year-over-year revenue growth of 66% to $43.3 billion, a sharp slowdown from the 262% surge in Q1 2024. Earnings per share are projected at $0.88.

Can the Third-Generation Chip Save NVIDIA’s China Market?

The biggest concern for this quarter centers around NVIDIA’s China business, which has been hit hard by export controls.

During ComputeX 2025 in Taipei earlier this month, NVIDIA CEO Jensen Huang revealed that the company’s market share in China has dropped from 95% under the Biden administration to just 50% due to AI chip export bans.

Shortly after Trump lifted some of the prior administration’s chip export rules, the new administration imposed a ban on NVIDIA selling its H20 chips to China, forcing the company to book a $5.5 billion expense related to potential losses.

Huang recently warned that the new restrictions could cost NVIDIA as much as $15 billion in lost sales, and emphasized that the Chinese AI market is expected to grow to $50 billion in the coming years — a huge opportunity if NVIDIA is locked out.

According to Reuters , NVIDIA plans to launch a new AI chip based on the Blackwell architecture targeting the Chinese market, with a significantly lower price than the H20 model. This would mark the third time NVIDIA has introduced a customized chip to comply with U.S. regulations while trying to retain some access to the Chinese market.

Analysts at Bank of America believe that given NVIDIA’s unique position in the global AI deployment cycle and the potential for a sales rebound later this year with new products for China, NVIDIA remains the top pick in the AI space.

Trump’s Middle East Trip Brings NVIDIA a Game-Changing Order

During President Trump’s recent trip to the Middle East, NVIDIA secured a landmark deal with Humain, a Saudi-based AI infrastructure company. Humain placed an order for 18,000 Blackwell GB300 chips, and pledged to gradually scale up to hundreds of thousands of GPUs over the next five years.

Bernstein analysts noted that for investors concerned about the sustainability of AI capital spending, this deal signals the emergence of a new deep-pocketed client willing and able to invest heavily in building regional and global AI hubs.

Is NVIDIA Stock Ready to Take Off Again?

So far, NVIDIA has exceeded EPS estimates for nine consecutive quarters, demonstrating strong earnings power and growth potential.

However, even a beat-and-raise scenario may not guarantee a rally — investors remain cautious about forward guidance and whether the AI narrative can continue to justify high valuations. In the past nine quarters, NVIDIA shares fell three times after reporting earnings — including an 8% drop after the last earnings release.

NVIDIA closed at $135.50 on the day before earnings, up 1% year-to-date in 2025, slightly outperforming the S&P 500’s 0.68% gain.

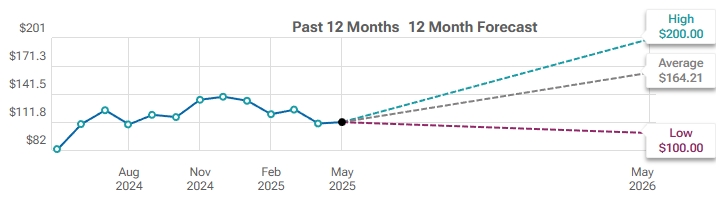

According to data from TipRanks , the average 12-month price target among analysts is $164.21 , implying more than 20% upside potential.

Average Analyst Price Target for NVIDIA, Source: TipRanks

Recommended Articles