Alibaba: Short-Term Noise, Long-Term Structure Unchanged

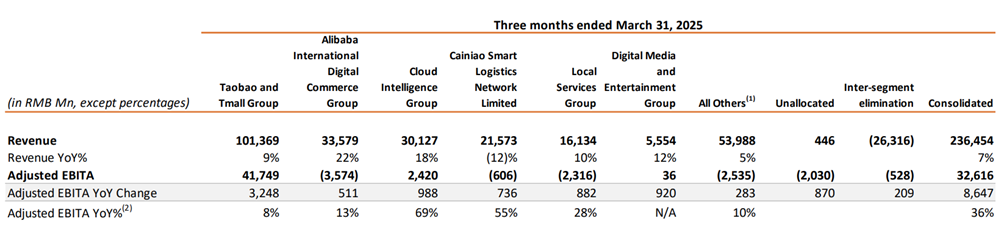

TradingKey - Alibaba’s latest quarterly results (Q4 FY2025) show revenue up 7% year-over-year—decent growth on paper, but a miss versus market expectations. Shares dropped over the following days as reaction settled in.

Source: Alibaba earnings report

At first glance, it may seem like a sign that Alibaba’s growth engine is losing steam. But dig a little deeper, and there’s more to the story. Particularly in e-commerce and AI initiatives, the company is laying the groundwork for what could be solid long-term upside.

E-Commerce Turns a Corner: Take Rate Improves, User Strategy Optimizes

According to National Bureau of Statistics, China’s total retail sales showed signs of recovery in Q1, with online sales of physical goods improving as well—suggesting a steady rebound in consumer activity. Ongoing government subsidies further boosted spending, making e-commerce platforms key beneficiaries. This supported a pickup in both Gross Merchandise Value (GMV) and Customer Management Revenue (CMR).

Historically, there has been a strong—though slightly lagged—correlation between overall retail sales and Alibaba’s CMR, providing near-term macro support for the company’s revenue outlook.

.png)

Source: National Bureau of Statistics and Alibaba earnings report

For Alibaba, the recent recovery in its e-commerce business has been driven by two key strategies: improving its take rate and reshaping its user growth model.

Starting last year, the company gradually raised platform service fees, moving from a 0% base fee to around 0.6%. This fee adjustment has contributed to a more stable income stream for the platform, especially via merchant management services.

However, the added cost has also put pressure on smaller sellers. To strike a balance between revenue and merchant retention, Alibaba rolled out a new AI-powered ad solution called “All-site Promotion.” The idea is simple: shift from charging based on exposure or clicks to a performance-based model that centers on conversions.

This new model is built on a performance-driven pricing model, with a compensation mechanism that guarantees a fixed ROI to merchants at the time they pay for ads. This structure reduces advertising risk at a fundamental level and enhances merchants’ willingness to invest. However, this strategy also means the platform’s recommendation algorithms must be highly accurate—whether its AI capabilities can support such a model at scale remains a key challenge.

To further support merchants, especially smaller ones, Alibaba has launched several AI business tools since 2024, all free of charge. Tools like Business Advisor, Store Assistant Chatbot, and PicCopilot have helped sellers run shops more efficiently. For many, these tools have also offset some of the rising service fees, easing operational costs.

The results are already visible. According to alibaba official news, Taobao and Tmall saw an over 10% year-on-year increase in overall ad conversion rate, along with double-digit growth in ad ROI In 2024. The link between GMV and CMR continues to strengthen.

Meanwhile, with internet traffic in China approaching saturation, Alibaba's user strategy is shifting from “user-first” to “high-value user-first.” In other words, the focus is on building a strong base of high-ARPU (Average Revenue Per User) customers.

This quarter earnings show that 88VIP memberships grew by double digits, crossing the 50-million mark. These users tend to place more orders and spend more per order, making them a key driver of platform revenue through better ad performance and higher commissions. In essence, they’re the “cash engine” of the platform’s self-sustaining growth.

To retain this valuable group, Alibaba offered a 3% stackable discount during the shopping festival, while also enhancing everyday perks like auto-discounts, smoother returns, and dedicated customer service. Despite its “user-first” slogan, the platform’s strategy clearly prioritizes high-value users at the core of its ecosystem.

On the merchant side, Alibaba is also testing new features to improve operational efficiency. For example, sellers can now exclude “high-refund-rate users” from their ad targeting settings—lowering refund costs and boosting ad ROI. It might sound like a minor function, but ultimately, it helps sellers “aim more accurately,” improving platform-wide efficiency.

That said, every initiative aimed at boosting conversions — whether it’s offering free technology tools or stepping up performance ad spend — ultimately translates into higher costs.

Take Taobao and Tmall Group, for example. Under the backdrop of government-backed consumer subsidies, e-commerce revenue rose 12% year-over-year this quarter, but adj. EBITA grew just 8%. The structural reason is clear: rising cost pressure from multiple fronts — platform-wide subsidies, incentives for new products, commission waivers, and off-platform traffic spending — all added up, leading to a disconnect between topline and bottom-line growth.

.png)

Source: Alibaba earnings report

JD.com also benefited from the same subsidy environment, but managed to grow revenue and profit more evenly — underscoring the side effects of Alibaba’s current “growth-through-spending” strategy. More importantly, this approach raises questions around long-term sustainability

Subsidies are a short-term fix to win traffic, not a durable moat. And with user growth reaching a natural ceiling across the sector, spending heavily to gain share may offer near-term results, but the long-term payoff is far less certain.

The goal behind these subsidies is simple: win or defend market share. But this isn’t a strategy you can lean on forever. As user growth across China’s e-commerce sector approaches a ceiling, spending more to stay competitive may work short term, but it’s no guarantee for the long haul.

Alibaba Cloud Sees Stable Foundation as Commercialization Advances

AI and cloud remain the go-to “remote triggers” for market excitement — but Alibaba’s latest earnings show that expectations may have run ahead of reality.

In Q4 FY2025, Alibaba Cloud reported revenue of RMB 30.1 billion, up 18% year-on-year — its fastest growth in three years and ahead of Microsoft Azure’s 16% and Tencent Cloud’s ~10% for the same period.However, the result landed at the lower end of market forecasts (17–20%) and missed more bullish projections of 25–30%, offering limited upside surprise.

.png)

Source: Alibaba earnings report

Profitability disappointed even more. Adjusted EBITA came in at RMB 2.42 billion, with margins slipping 1.9 percentage points quarter-on-quarter to 8% — below both last quarter’s level and market consensus.This sparked concerns about potential margin compression.

Cash flow and capex trends added to the uncertainty. Free cash flow dropped 76% YoY to $374 million, mainly due to stepped-up investments in AI and infrastructure. Still, capex came in at just RMB 24 billion — well below Alibaba’s stated annual target of RMB 120 billion and even behind Tencent’s RMB 27 billion this quarter. These figures have prompted questions: Are AI ambitions being adequately backed with capital? Or is restricted access to high-performance chips becoming a limiting factor?

The issue isn’t that Alibaba’s cloud numbers were poor. The 18% growth still outpaced Microsoft and materially beat Tencent. And while AI monetization remains early-stage, Alibaba is laying the groundwork across model development and compute infrastructure.

Its in-house large model, Qwen, has quickly become one of China’s most active open-source ecosystems. According to CNBC, Qwen has open-sourced over 200 models, led to 100,000 derivative variants, and surpassed 300 million global downloads as of April 2025. API call volumes are growing exponentially.

Its hybrid cloud and industry-specific SaaS products are gaining traction, especially in core verticals like finance and telecom — areas where Alibaba holds strong market share and offers differentiation beyond standard cloud services. Notably, Alibaba’s pricing undercuts AWS by 15–20%, giving it a competitive edge.

Management maintains confidence in further growth. On the earnings call, CEO Eddie Wu noted that cloud adoption continues to expand across industries, and that the migration of AI workflows to the cloud — which in turn drives API usage — will take time. He noted that Q1 results may not fully reflect inference-related demand, suggesting Q2 could provide clearer visibility.

JPMorgan reiterated its “Overweight” rating after the call, stating that Alibaba Cloud’s revenue drivers remain intact and predicting a reacceleration in top-line growth to 22% or higher next quarter.

International E-commerce Growth Slows, But Fundamentals Remain Solid

Alibaba’s international commerce segment remained a key revenue driver, reporting a 22.3% YoY increase. But this trailed market expectations of 26.4% from Reuters, the miss was largely attributed to currency translation losses.

.png)

Source: Alibaba earnings report

The segment remained loss-making, with a net quarterly loss of RMB 3.6 billion — a sequential improvement, though still slightly wider than consensus estimates.

However, the recent U.S. tariff hikes appear to have minimal direct exposure. Platforms like Lazada and Trendyol operate highly localized models across Southeast Asia and the Middle East, with minimal reliance on U.S.-China cross-border trade routes. Moreover, AliExpress has a relatively small GMV footprint in the U.S., insulating it from the brunt of recent tariff hikes.

Interestingly, these very trade restrictions may offer indirect tailwinds. Rising import prices in the U.S. could push cost-sensitive consumers toward alternative platforms — a dynamic some analysts are calling the “tariff refugee” effect. According to sensortower, Alibaba’s shopping apps have seen a steady increase in U.S. downloads Since early 2025, with AliExpress briefly cracking the Top 5 in iOS shopping app rankings — signaling potential upside in cross-border user growth

Near-Term Challenges in Local Services, but Structural Tailwinds for Instant Retail

Alibaba’s local services segment posted a 10.3% year-on-year revenue increase in Q4 FY25, maintaining a top-line performance. However, operating losses widened significantly from the quarterly average of RMB 600 million, suggesting deeper structural cost pressures — beyond seasonal fluctuations.

.png)

Source: Alibaba earnings report

Notably, this spike in losses occurred even before the onset of the latest round of subsidy-driven competition in food delivery. Since Q2, major players including JD.com, Alibaba, and Meituan have launched aggressive promotions,initiating a fresh wave of subsidy-led competition. This trend is likely to weigh on profitability in the near term.

Looking beyond current challenges, however, market fundamentals remain compelling. According to Morgan Stanley, China’s on-demand retail market could reach RMB 2 trillion by 2030, with a CAGR exceeding 20%. Alibaba aims to tap into this trend via its Taobao-branded instant delivery, merging front-end warehousing with existing Tmall logistics and high-frequency traffic. Unlike food delivery firms, which rely heavily on rider networks, this model delivers higher scalability and user stickiness.

.png)

Morgan Stanley highlights that this approach not only captures new demand but also enhances core e-commerce margins, while reducing losses at Ele.me — pointing to strategic synergy beyond short-term cost dents.

Compressed Valuation Signals Bottom-Up Entry Point

According to data from Seeking Alpha, Alibaba currently trades at a GAAP price-to-earnings (P/E) ratio of approximately 16.5x — well below its historical average of 20x or higher.

.png)

Source: SeekingAlpha

The latest earnings report offers tangible support for a “bottoming and recovery” valuation narrative. Core businesses such as e-commerce and cloud computing continue to demonstrate steady growth, while international commerce is gaining traction. Together, these trends reflect an evolving business mix with clearer growth pathways and stronger profit potential.

Alibaba has strengthened shareholder returns and strategic focus through aggressive buybacks, averaging over 10 billion annually in the past two years.With Around 20 billion in remaining authorization, continued repurchases are expected to support market confidence and valuation recovery.

Conclusion

Alibaba’s Q4 FY25 results may not have delivered on all fronts, but they are far from a disappointing read.

The core e-commerce segment remains solidly profitable, with international commerce and Alibaba Cloud now serving as dual growth catalysts. AI-led transformation is also taking shape—especially across advertising, membership monetization, and cloud-based applications.

In the short term, discounts and subsidies are indeed pressuring margins. Yet structurally, Alibaba holds two major long-term advantages: domestic AI innovation and global expansion. As long as these two growth drivers continue to advance, the company’s long-term value remains compelling.

Recommended Articles