US Stocks Close: Dow Hits Another Record High, Nasdaq Rises 1.12%; Market Expects Samsung Electronics to Post Strong Q2 Earnings, SK Hynix Starts US Listing Process, Chip and Memory Stocks Lead Gains.

TradingKey - Market expectations that Samsung Electronics will soon post a positive profit alert in its preliminary Q2 earnings report, coupled with SK Hynix officially launching its roadshow for a US listing, have fueled high market trading sentiment. The three major US stock indexes rose across the board, with the Dow Jones Industrial Average continuing to hit record highs, the Nasdaq Composite Index strengthening, and chip stocks and memory stocks leading the gains.

As of the close, the Dow Jones Industrial Average rose 0.29% to 53,055.91 points; the Nasdaq Composite Index rose 1.12% to 26,121.16 points; and the S&P 500 Index rose 0.72% to 7,537.43 points.

Performance of Tech Stocks

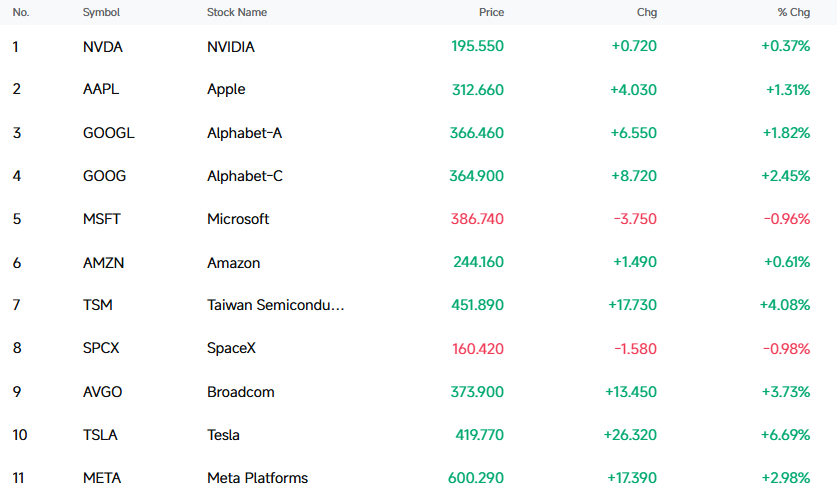

Tesla (TSLA) rose 6.69% to close at $419.77.

Tesla's autonomous ride-hailing footprint has officially expanded into the southeastern United States. Recently, Tesla officially announced on the social media platform X that its Robotaxi autonomous ride-hailing service has now expanded to a small area in western Miami. This marks the first time its driverless ride-hailing service has entered Florida, making it the third state covered after Texas and California.

Among mega-cap tech stocks, Tesla (TSLA) rose 6.69%, Broadcom (AVGO) rose 3.73%, Meta Platforms (META) rose 2.98%, Alphabet (GOOGL) rose 1.82%, Apple (AAPL) rose 1.31%, Amazon (AMZN) rose 0.61%, and Nvidia (NVDA) rose 0.37%; on the downside, SpaceX (SPCX) fell 0.98% and Microsoft (MSFT) fell 0.96%.

[Source: FutuBull]

The Philadelphia Semiconductor Index rose 2.17% to 12,900.14 points. Among its 30 constituents, 22 rose and 8 fell. Advanced Micro Devices (AMD) rose 6.61%, Qualcomm (QCOM) rose 5.80%, TSMC (TSM) rose 4.08%, Broadcom (AVGO) rose 3.73%, and Texas Instruments (TXN) rose 3.56%.

Memory stocks led the gains, with Western Digital (WDC) up 7.14%, Seagate Technology (STX) up 5.86%, and Micron Technology (MU) up 0.96%. A Morgan Stanley report pointed out that the current HDD market faces a severe supply-demand imbalance: on the demand side, driven by AI workloads, the annual growth rate is as high as 40% to 50%, with hyperscale cloud service providers storing about 80% of their data on HDDs; on the supply side, the annual growth rate is only 30% to 35%, leading to a supply deficit of 10% to 15% of demand by 2026, while ODM manufacturers hold only 1 to 2 weeks of inventory.

Popular US-listed Chinese stocks mostly gained, with BOSS Zhipin (BZ) up 5.15%, Nio (NIO) up 4.70%, Bilibili (BILI) up 4.43%, XPeng (XPEV) up 3.71%, and GDS Holdings (GDS) up 3.59%.

Corporate News

Broadcom Extends Custom ASIC Chip Contract with Apple to 2031

Broadcom and Apple have signed a new multi-year partnership agreement, extending their chip supply cooperation to 2031. According to a regulatory filing disclosed by Broadcom on Monday, the two parties have reached a new agreement on custom ASIC chip products, under which Broadcom will develop and supply a range of custom silicon products for multiple generations of Apple products. The long-term cooperation between the two companies has an established foundation. In 2023, they announced a multi-billion dollar agreement for Broadcom to develop and produce 5G radio frequency components for Apple. Prior to this, Broadcom was already a major supplier of wireless connectivity chips, such as Wi-Fi and Bluetooth, for Apple.

Microsoft Plans to Cut 4,800 Jobs to Reduce Costs and Improve Efficiency

Microsoft plans to lay off 4,800 employees, representing 2.1% of its total workforce, with its gaming business serving as the core area of contraction. The Xbox division will see a cumulative layoff rate of 20% by fiscal year 2027, to be implemented gradually in batches, making it the hardest-hit area of this adjustment. In addition to the layoffs, Microsoft is simultaneously launching a review of its gaming assets, with four studios exiting its system: Compulsion Games and Double Fine, acquired in earlier years, will return to independent operations; Ninja Theory and Undead Labs will change hands; and France's Arkane Studios is also advancing an evaluation of strategic options.

Anthropic Enters into a 20-Year Data Center Partnership with TeraWulf

Anthropic has entered into a 20-year data center partnership agreement with TeraWulf, under which the latter's computing power campus in Kentucky, USA, will provide infrastructure support for the former. The data center has a supported power capacity of approximately 400 megawatts, with the first phase expected to connect to the grid and supply power in the second half of 2027. According to estimates, this cooperation is projected to generate over $19 billion in revenue in its initial phase.

Nvidia Denies Kyber Delay Rumors: Product Roadmap Remains Unaffected

An Nvidia spokesperson responded that the company's product roadmap remains unaffected. Previously, research firm SemiAnalysis claimed that Nvidia's next-generation AI computing architecture, Kyber, had hit research and development setbacks, and its release date could be delayed by 12 months to 2028. The architecture was originally scheduled for the next-generation Rubin Ultra GPU. Jordan Klein, an analyst at Mizuho Securities, stated that similar rumors of delays in Nvidia's new products have appeared in the market multiple times, and such news is more like "clickbait noise." Limited by the impact of the rumors, Nvidia's stock price still rose about 1.2% during Monday's trading. Kyber is regarded as a major upgrade to Nvidia's data center architecture, and will feature a brand-new vertical rack design to increase computing density and reduce network latency, while also expected to drive demand in the data center co-packaged optics (CPO) industry chain.

Industry & Macro News

Morgan Stanley Recommends Betting on Fading Fed Rate Hike Expectations

Morgan Stanley interest rate strategists suggest that as expectations for Federal Reserve interest rate hikes weaken, investors should bet on shorter-dated US Treasury yields falling relative to longer-dated ones. This would result in a steepening of the US Treasury yield curve, meaning an widening of the spread between shorter and longer maturities. Specifically, on July 2, Morgan Stanley recommended betting on a widening of the spread between 7-year and 30-year US Treasuries.

The core logic of this trade is that the market is still overpricing Fed rate hikes, while the bank expects no rate hikes this year and a rate cut in March next year. The strategy is based on the San Francisco Fed's proxy federal funds rate being 100 bps higher than the actual rate, representing an excessive equivalent rate hike. Under the base case, this spread represents a realizable risk premium.

Saudi Arabia Slashes Official Selling Prices of Crude Oil to Asia

Following the US-Iran ceasefire, global crude oil supply has recovered rapidly, and the market structure has abruptly shifted from tight to loose. Saudi Arabia has slashed its official selling prices for crude oil, with its flagship light crude for the Asian market shifting directly from premium to discount pricing. This marks the first discounted sale since the 2020 price war, with the price cut far exceeding market expectations.

The core driver of this pricing shift is the concentrated release on the supply side. After the Strait of Hormuz resumed navigation, previously stranded Gulf crude oil flooded into the market. Coupled with the full recovery of oil-producing countries' export capacities, global market supply quickly saturated. To protect its core market share in Asia, Saudi Arabia chose to respond proactively with deep price cuts, and even rarely opened spot sales channels to clear backlogged inventory in the Persian Gulf.

Fed Governor Waller: More Forward Guidance Is Not Always Better, Can Be Dispensed With Entirely If Necessary

Federal Reserve Governor Waller stated that monetary policymaking cannot mechanically apply historical experience, but must judge policy effects based on the "initial conditions" of the current economy. In addition, he said that although forward guidance can influence the market in advance and accelerate policy transmission, if it is too rigid or faces multiple potential economic scenarios, it may instead constrain decision-making and delay policy adjustments. Therefore, it should remain sufficiently flexible and, if necessary, should not even be used.

USD/JPY Approaches 40-Year High Once Again

Following its bottoming out and rebound last Friday, USD/JPY is currently trading near 162.28, up 0.59%, once again approaching the 40-year high of 162.83. The yen remains under deep pressure, and the risk of intervention by Japanese authorities in the FX market continues to rise. Market analysis suggests that this round of yen weakness stems primarily from macro factors such as USD strength, the US-Japan interest rate differential, and lagged Japanese monetary policy. At the same time, an easily overlooked factor is also playing out: Japanese equities and the yen are showing a classic inverse relationship. Combined with the analysis of mainstream institutions, the yen's weakness is highly likely to persist in the medium to long term, which also indicates that capital continues to favor Japanese tech stocks.

US June ISM Services PMI Registers 54, Expanding for the 24th Consecutive Month

Economic activity in the services sector continued to expand in June. The Services PMI registered 54, remaining in expansionary territory for the 24th consecutive month, though below the market expectation of 54.3. Anthony Nieves, Chair of the ISM Services Business Survey Committee, stated: The June Services PMI registered 54, down 0.5 from May's 54.5. The Business Activity Index remains in expansionary territory, decreasing 2.3 to 55.4 from May's 57.7. The Prices Index fell to 67.7 in June, down 3.6 from May's 71.3, dropping below 70 for the first time since February. The index has been above 60 for 19 consecutive months, with a 12-month average of 68.

Recommended Articles