This Tech Giant Is Buying Back Stock Hand Over Fist. Insiders Are Buying, Too. Should You Follow?

Key Points

This household software name has fallen to an all-time low valuation.

Management just executed a massive accelerated share repurchase, and insiders are buying.

Fears over AI disruption may be overblown, though we won't know for sure for years.

- 10 stocks we like better than Salesforce ›

The enterprise software sector has fallen off a cliff to start the year, with the largest software exchange-traded fund, the iShares Expanded Tech-Software Sector ETF (NYSEMKT: IGV), down nearly 25% year to date.

Yet while the software sector has crashed, evidence that AI might disrupt these companies' business models hasn't shown up in their financials -- at least not yet.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

One major software player has seen its valuation fall to levels not seen in its history, and management is taking advantage, implementing a massive accelerated share repurchase, with insiders also buying shares on the open market.

Are these signs of confidence reason to follow and scoop up shares yourself?

Salesforce's stock swoon

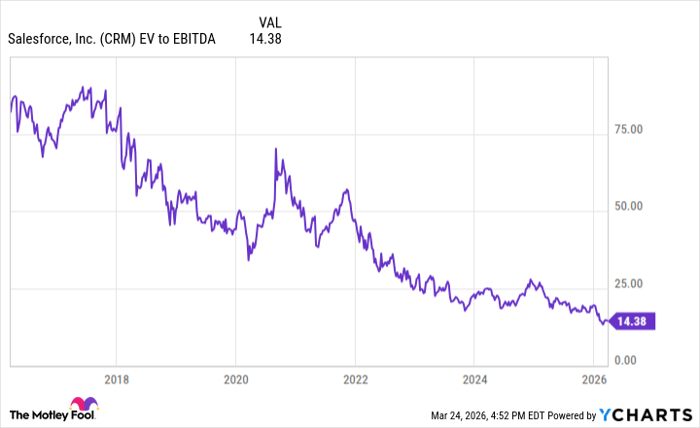

Salesforce (NYSE: CRM) software has long been a mainstay of enterprise IT departments. But amid this year's software "SaaS-pocalypse," its valuation has fallen to an all-time low.

CRM EV to EBITDA data by YCharts

Salesforce's growth has slowed a bit from what it used to be, but that's really just due to the law of large numbers. Last quarter, the numbers were still quite solid, with revenue up 12.1% and earnings per share up 18.3%.

The declining share price even amid rising earnings raises questions about the long-term effect of AI on Salesforce's business. Will AI agents be able to do the work for which Salesforce currently charges clients? Will AI enable small companies to build a lower-cost customer relationship management software competitor? Or on the flip side, will Salesforce be able to harness AI to its advantage?

Salesforce buys with both hands, as do insiders

Clearly, Salesforce CEO Marc Benioff thinks it will be the latter and is putting his money where his mouth is, so to speak.

Salesforce had already been ramping up share repurchases over the past few years. Over the past three fiscal years, Salesforce repurchased $7.6 billion, $7.8 billion, and $12.6 billion of stock, respectively. Then, as the share price fell this year, Salesforce took things up a notch, authorizing a $50 billion repurchase program. In mid-March, Salesforce raised $25 billion in debt and put it to work in an accelerated share repurchase program, spending about $20 billion of that all at once, with the remaining $5 billion to be executed through the remainder of the year.

That is a very significant number of shares Salesforce just repurchased. As of the release of its annual report on Feb. 25, Salesforce had 923 million shares outstanding. The mid-March accelerated repurchase retired another 103 million shares, immediately lowering Salesforce's share count by 11.1%.

Assuming Salesforce's current share count is around 810 million shares and declining, its current market capitalization is around $148 billion. Last year, Salesforce generated $14.4 billion of free cash flow, and it expects to grow that figure by 10% in fiscal 2027. That means Salesforce's stock is only trading at around 9.5 times this year's free cash flow guidance.

Other insiders are also expressing optimism. Directors David Blair Kirk and Laura Alber each purchased about $500,000 worth of shares on the open market on March 18 and 19, respectively.

Image source: Getty Images.

Risks to the story, and how Salesforce is reacting

There are of course some valid concerns behind Salesforce's bargain-basement valuation. The rapid improvements in agentic AI over the past six months or so have raised fears that model providers, such as Anthropic and OpenAI, may pose a threat to current software leaders.

For its part, Salesforce is partnering with model providers. Specifically, Salesforce announced a close partnership with Anthropic in October 2025.

After integrating with Anthropic and closing the acquisition of Informatica in November, Salesforce's Agentforce 360 platform, its new unified agentic AI platform based in Slack, grew 37% last quarter, bolstering overall results. While it's true that other parts of Salesforce's empire may be slowing, the fact that its agentic offering is growing that rapidly is promising.

Another point of interest is that Salesforce just began disclosing something called the agentic work unit (AWU). This metric measures the output of work that AI agents execute for Salesforce's customers. Predictably, as agentic technology has improved, these AWUs have been taking off, growing 57% sequentially in the fourth quarter.

While a partner like Anthropic charges Salesforce on a per-token basis, Salesforce can monitor how efficiently those customers are using those tokens. If Salesforce's internal data and sales professionals can help customers use tokens more effectively in a proprietary way, that could be a recipe for generating value.

But investors shouldn't expect a quick turnaround

Clearly, the fear overhanging software stocks is real, and there doesn't seem to be anything that will change the narrative in the near term. If anything, the release of more powerful AI models may only add to the concern. Thus, it may take several quarterly earnings reports or updates to convince skeptics that the AI fears are overblown.

Meanwhile, Salesforce will now carry some $30 billion of net debt, up from about $5 billion at the end of January. While that debt load amounts to less than two times this year's likely free cash flow, which is a very reasonable leverage ratio, it also adds a bit of risk should anything go awry.

As such, Salesforce is certainly a name to watch during this period of rapid AI disruption. If signs emerge that its platform will be one of the AI survivors or beneficiaries, it could be one of the best buys in the market.

Should you buy stock in Salesforce right now?

Before you buy stock in Salesforce, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Salesforce wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $490,325!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,074,070!*

Now, it’s worth noting Stock Advisor’s total average return is 900% — a market-crushing outperformance compared to 184% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of March 26, 2026.

Billy Duberstein and/or his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Salesforce. The Motley Fool has a disclosure policy.

Recommended Articles