ConocoPhillips and Trump's Venezuela Play: Is This a Hidden Catalyst or Just More Noise for Investors?

Key Points

ConocoPhillips has experienced a turbulent history in Venezuela.

It may want to see old debts settled before rushing to produce oil there.

It's likely to be awhile before ConocoPhillips returns to Venezuela.

- 10 stocks we like better than ConocoPhillips ›

The bullish case for oil stocks received a significant boost earlier this month when U.S. forces captured the now former Venezuelan President Nicolas Maduro, sparking hope that the petroleum-rich country will eventually be open to Western oil majors.

Count ConocoPhillips (NYSE: COP) among the domestic oil equities in rally mode to start 2026. January isn't over yet, but this stock is higher by more than 8%. How much, if any, of that move is attributable to Venezuela is up for debate.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Regime change is afoot in Venezuela, but that's not a primary catalyst for shares of ConocoPhillips. Image source: Getty Images.

Yes, there's been not-so-gentle cajoling from President Trump toward U.S. oil giants, including ConocoPhillips, to be prepared to invest in the South American country. Maybe they will. Perhaps they won't, but the point is that investors ought to be careful when considering this stock as a Venezuelan play, and that's not an indictment of the company.

ConocoPhillips has Venezuelan scores to settle

Investors who have been actively keeping up with the situation in Venezuela by now likely know that Chevron (NYSE: CVX) is the only domestic oil company operating there, but we're talking about ConocoPhillips here.

Like rival ExxonMobil (NYSE: XOM), Conoco was banished from the country in 2007 when then-President Hugo Chavez nationalized the nation's energy industry. So while access to any member of the Organization of Petroleum Exporting Countries (OPEC) is coveted, history alone could give Conoco pause about rushing back to Venezuela. Then there's the matter of derivatives of that history.

When accounting for interest, Conoco has legal claims against Venezuela totaling $12 billion. Exxon's amount to $20 billion, but that company is hoping to recoup $12 billion, too. At $12 billion apiece, Conoco and Exxon are two of Venezuela's biggest non-sovereign creditors. That's not chump change. In fact, $12 billion is nearly 10% of Conoco's market capitalization as of Jan. 28.

There's speculation that Exxon and Conoco would tie future investment in Venezuela to recouping those debts, but the White House views that as a long-term matter, not something to grapple with in the near term. Said another way, the Trump administration wants U.S. oil companies to invest in Venezuela, but it's not going to play debt collectors to make that happen.

Conoco keeps a low risk profile

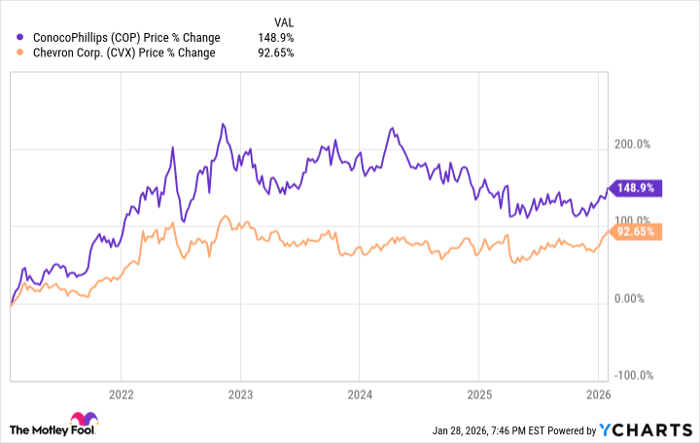

Investors experienced in the oil patch know this segment is ripe with idiosyncratic risk, or issues that are germane to a specific industry. It's difficult, perhaps impossible, to eliminate all idiosyncratic risk in the oil industry, but producers can take steps to minimize broader turbulence. Conoco does that, and not at the expense of shareholders, as the stock outpaced Chevron over the past five years.

COP data by YCharts

For example, Conoco's largest production region is the lower 48 states. Its other significant regional exposures include Alaska, Canada, and Europe. While it does explore and produce in some potentially politically volatile corners of the globe, it's not biting off excessive risk on that front.

That may be a sign that Conoco's Venezuela story will be penned over years, not weeks or months, if it's written at all.

Should you buy stock in ConocoPhillips right now?

Before you buy stock in ConocoPhillips, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ConocoPhillips wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $450,256!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,171,666!*

Now, it’s worth noting Stock Advisor’s total average return is 942% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of February 1, 2026.

Todd Shriber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chevron. The Motley Fool recommends ConocoPhillips. The Motley Fool has a disclosure policy.

Recommended Articles