TSMC Q4 2025 Earnings Preview: 2,000 Yuan Price Target, Is It a Dream or Reality?

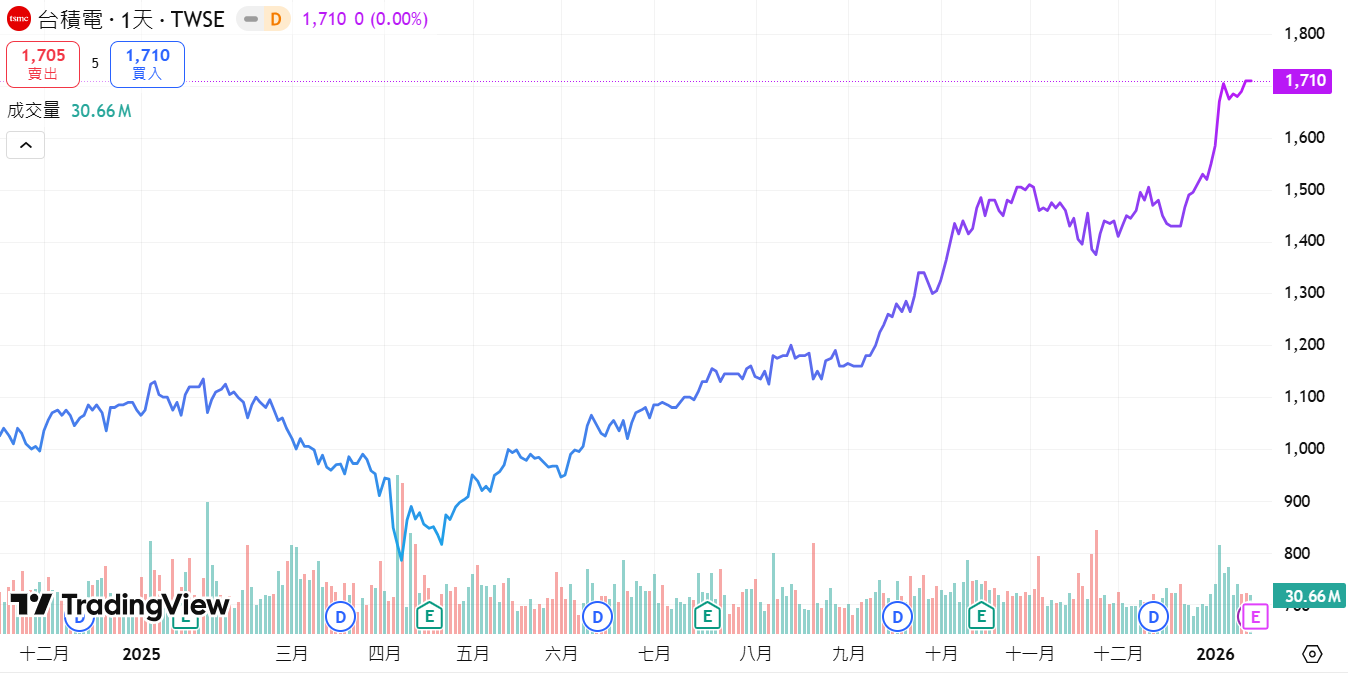

With TSMC's stock price having reached these levels, do earnings still matter? The Q4 2025 earnings report, set for release on January 15, is more than just a summary of profits for many investors watching TSMC; it addresses a practical question: is there still room for the stock to continue climbing?

Source: TradingView

Why is this earnings report particularly important? Because TSMC is undergoing its most significant identity shift in a decade: it is transforming from a company reliant on Apple into one driven by AI. This transition is not just a high-level expectation but a reality already reflected in order books and capacity planning. While Apple remains its largest customer, the growth rate and order scale of AI clients have prompted the market to re-evaluate TSMC's valuation logic. It is no longer a cyclical stock fluctuating with iPhone sales, but a growth stock tethered to global AI infrastructure. This earnings report serves as a litmus test for how far and how long this transformation can last, and whether the stock has a chance to reach the market's target price of NT$2,000 this year.

The market is focusing on three key questions regarding this earnings report:

Question 1: Is CoWoS packaging capacity sufficient to meet the demand from Nvidia and Broadcom?

Many believe TSMC's core competitiveness lies solely in its advanced process nodes, but currently, the real bottleneck for the entire AI supply chain is actually the packaging stage.

Source: TSMC

Simply put, CoWoS (Chip-on-Wafer-on-Substrate) is the key technology for packaging high-performance GPUs and High Bandwidth Memory (HBM) together. In the high-end AI GPU segment, TSMC's CoWoS is virtually the only solution capable of large-scale production and stable delivery. The timely shipment of AI chips from Nvidia and Broadcom now depends less on whether the chips can be fabricated and more on whether TSMC's CoWoS packaging capacity can keep up.

The speed of CoWoS capacity expansion determines the shipment pace of AI chips. TSMC's 2026 monthly CoWoS capacity target has been revised upward from the original market estimate of 100,000 wafers to approximately 127,000 wafers, an increase of over 20%, or about 1.5 million wafers on an annualized basis. Of this, Nvidia alone has booked about 800,000 to 850,000 wafers, taking more than half the capacity, while Broadcom has ordered about 240,000 wafers, primarily for major clients like Meta and Google. It is evident that the scale and pace of TSMC's CoWoS expansion are largely tailored to the demand for this round of AI platform upgrades.

Why has CoWoS suddenly become so sought after? A key change is that the delivery unit for AI chips has evolved from individual chips to entire computing cabinets. For instance, in Nvidia's latest Rubin platform, the flagship Vera Rubin NVL72 is an entire cabinet-scale AI supercomputer, housing 72 Rubin GPUs and 36 Vera CPUs. All these high-compute chips must be paired with high-capacity HBM and then integrated through advanced packaging like CoWoS. Consequently, this new generation of GPUs consumes CoWoS capacity by the cabinet-full, exponentially increasing pressure on TSMC's packaging lines.

Signals from the Taiwanese supply chain further corroborate this. TSMC's own advanced packaging lines have been running at full capacity for some time, forcing it to outsource some CoWoS-related orders to OSATs like ASE and SPIL. Over the past few quarters, these companies have taken turns mentioning advanced packaging expansion and equipment investment during their investor conferences, and their stock prices have already pre-emptively reflected these expectations. Why does capital tend to rush into the packaging segment first? One practical reason is that many CoWoS orders are locked in on an annual or multi-year basis, providing high visibility and clear delivery schedules. In contrast, new process nodes take 12–18 months to transition from design-in to volume shipments for verification and yield ramping. Advanced packaging, once equipment is in place and capacity is live, drives revenue and shipments more quickly and directly, becoming visible within two or three quarters of financial reports.

Therefore, in this area, there are three things to watch in the Q4 earnings report:

First, whether management will once again raise the 2026 monthly CoWoS capacity target or provide a clearer capacity range;

Second, the latest progress on 2026 CoWoS capacity allocation for AI ASIC customers like Broadcom (beyond Nvidia), which determines the strength of the secondary growth engine outside of GPUs;

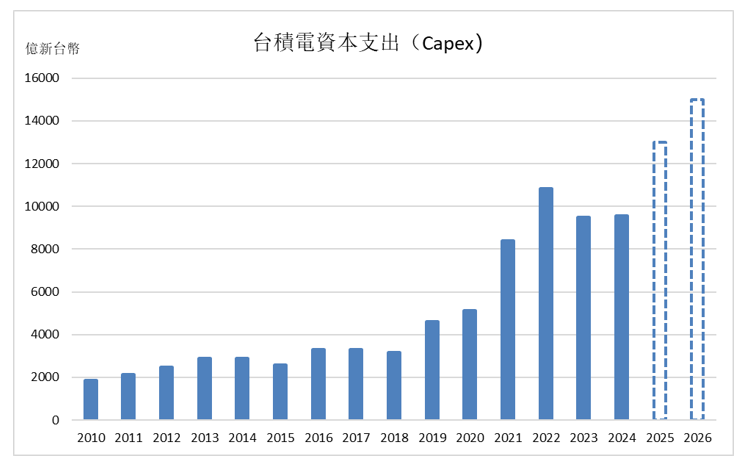

Third, how much of the future capital expenditure is allocated to advanced packaging. If the 2026 Capex plan shows a continued increase in the proportion of investment related to advanced packaging, it would effectively serve as official confirmation that CoWoS and the entire advanced packaging chain will remain TSMC's primary growth focus for the coming years.

Question 2: 2nm mass production has begun, but who secured the first batch?

The market has largely priced in the start of 2nm mass production itself. What truly impacts TSMC's earnings elasticity over the next two to three years are three more detailed questions: How will initial capacity be allocated among key customers like Apple, Nvidia, and Broadcom? Can the 2nm (N2) yield ramp-up speed exceed expectations? Can TSMC leverage this opportunity to further hike prices on advanced nodes?

Regarding production progress, N2 mass production launched as scheduled in Q4 2025, with an initial monthly capacity of approximately 35,000 wafers. The market expects monthly 2nm capacity to reach about 140,000 wafers by the end of 2026, significantly higher than earlier conservative estimates of 100,000 wafers. Performance gains are also impressive; compared to N3E, N2 offers a 10–15% speed increase at the same power, or a 25–30% power reduction at the same speed.

However, no matter how great the capacity is, it depends on who gets it. Apple has reportedly secured over half of the initial 2nm capacity for 2026, primarily for the A20 processor in the iPhone 18 and the next-generation M-series chips for Mac, which are considered the most expensive smartphone and PC processor platforms in history. Nvidia's upcoming Rubin-successor platforms and other AI/HPC chips are also seen as core potential customers for 2nm, while Broadcom, AMD, and others are also lining up for initial capacity.

There is a crucial pricing logic here: the market generally expects 2nm wafer pricing to be about 10–20% higher than 3nm. However, as initial yields are still ramping up, the positive contribution of 2nm to overall gross margins is not expected to be significantly realized until the latter half of 2026.

This explains why institutions are exceptionally sensitive to TSMC's gross margin guidance for Q4 and Q1 2026. Three key signals from this earnings call will directly impact valuation:

First, Yield ramp-up speed. If TSMC reveals that N2 yields have reached over 70%, it means cost absorption efficiency is better than expected, opening up room for gross margin expansion.

Second, Customer structure. If Apple and Nvidia secure most of the initial 2nm capacity, it implies TSMC has immense pricing power at this node, as these two customers are almost entirely dependent on TSMC for high-end products and are far more sensitive to performance and supply stability than to price.

Third, 3nm capacity release. Following the mass production of 2nm, 3nm capacity is expected to tilt more toward customers like Broadcom and AMD, further supporting overall revenue growth.

A risk to note is that initial 2nm capacity is limited. If management's outlook for N2 shipments and revenue contribution in 2026 is significantly lower than the market's current consensus of 10–20%, the market might be disappointed in the short term. However, over a longer cycle, 2nm is still expected to become TSMC's primary profit engine in 2027–2028.

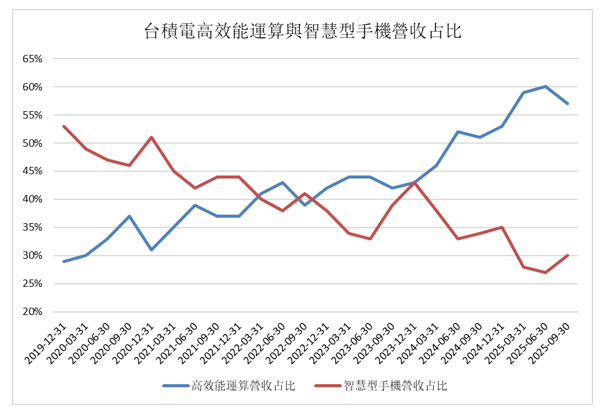

Question 3: Reshuffling the customer base: from Apple dependency to multi-engine AI growth

This may be the most overlooked yet profound point in the earnings report: TSMC is shifting from a reliance on Apple and the smartphone cycle to a greater dependence on AI/HPC infrastructure demand. This is not just a change in the customer list, but a qualitative transformation in revenue structure and business model, pivoting from the consumer electronics cycle to the AI computing infrastructure cycle .

Looking at the numbers, Apple has long been TSMC's largest customer, accounting for just over 20% of revenue. In 2025–2026, Apple will remain the top customer, but its growth is maturing. Bernstein predicts that Nvidia's share of TSMC's revenue will rise rapidly from about 5–10% in 2023 to just over 20% in 2025–2026, potentially matching Apple in scale. The share of AI ASIC and networking chip makers like Broadcom is also rising, forming a multi-core structure of Apple plus an AI client cluster.

Source: TSMC Earnings Report

Taking Nvidia as an example, cumulative orders for AI chips like the H200 in the Chinese market have reportedly exceeded 2 million units, and the company is discussing further capacity expansion with TSMC starting in 2026 to meet delivery requirements. Players like xAI, which announced a new $20 billion funding round in early 2026 primarily for expanding hyperscale data centers and purchasing Nvidia GPUs, are also moving along the same supply chain, increasing TSMC's mid-to-long-term order visibility for advanced nodes and advanced packaging.

More importantly, there is a difference in the nature of demand. Apple's orders are highly seasonal, tied to iPhone/Mac product cycles, with shipment peaks concentrated in the second half of the year. If iPhone sales miss expectations, TSMC quickly feels the pressure. In contrast, orders from customers like Nvidia, Broadcom, and AMD are tied to cloud computing and AI infrastructure investment. These involve year-round ordering, higher unit prices, and a willingness to pay premiums, making the demand more sustainable and predictable.

Therefore, this shift in customer structure will essentially strengthen the market's pricing of TSMC's AI super-cycle across three dimensions, making this earnings report particularly important to watch:

First, Improved revenue predictability. The capital expenditure cycle for AI customers is 3–5 years, unlike the seasonal fluctuations of consumer electronics. If the earnings call reveals a significant increase in the proportion of 2026 long-term contracts and prepaid orders within the total order book, the valuation baseline could be pushed higher.

Second, Structural improvement in gross margin. AI chip customers are less sensitive to price because computing power is competitiveness, and they are willing to share R&D costs. TSMC's Q4 gross margin is expected to be 59–61%. If expectations or guidance are revised upward, the market will interpret this as the further manifestation of pricing power brought by AI clients, with a degree of sustainability.

Third, Rationality premium for capital expenditures. On one hand, the market is concerned that TSMC's cumulative capital expenditure of over $150 billion from 2026 to 2028 might be too aggressive; on the other hand, it is using this earnings report to verify whether this money is a bet on the cycle or backed by long-term AI orders and a diversified customer structure. If the order visibility and customer structure provided by management are sufficient to support the utilization and returns of this massive investment, ultra-high Capex will instead be seen as a deepening moat and capacity becoming a new scarce asset, rather than simple cash-burning expansion.

Data Verification: The Passing Line and Surprise Line for Q4 Earnings

After discussing the logic, it ultimately comes back to the numbers. The market consensus for TSMC's Q4 earnings is roughly as follows:

Market Consensus Expectations | Figures/Range |

Q4 2025 Revenue | NT$1.046 trillion (Reported, +20.45% YoY) |

Q4 2025 Gross Margin | 59–61% |

Q4 2025 Net Income | NT$430–470 billion |

Q4 2025 EPS | NT$17–19 |

Q1 2026 Revenue | NT$980–1,030 billion |

Q1 2026 Gross Margin | 60–63% |

These figures can be viewed as the baseline for this earnings report. What could truly cause a significant stock price reaction are several key points that either beat or miss the consensus:

Q1 Revenue Guidance: If the Q1 guidance continues to fall around 60–63%, it would be roughly in line with expectations; if it is significantly higher than 60%, it would be an upside surprise, leading the market to believe that the AI/HPC business is offsetting the dilution from overseas fabs and new nodes; if it falls below 59%, it would be a miss, typically interpreted as an issue with yield, costs, or pricing pressure.

2026 Capex Guidance: The market is currently looking at the $45 billion to $50 billion range (approximately NT$1.4–1.6 trillion). If the company provides a higher investment plan, it would signify stronger confidence in medium-to-long-term AI/HPC demand and 2nm/advanced packaging expansion. If it stays significantly below this figure, it will be seen as slightly conservative regarding long-term demand.

Source: TSMC Financial Reports

3nm/2nm Capacity and Pricing: If this disclosure mentions that advanced nodes were essentially at full capacity in Q4, and the Q1 guidance shows sustained high utilization for 3nm with 2nm ramping as planned while maintaining significant premium pricing, it would further validate the sustainability of AI/HPC demand and profitability.

Conclusion: With TSMC rising this much, is it still a good time to buy?

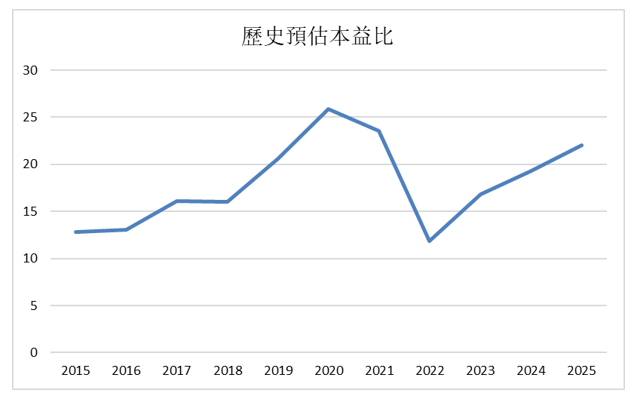

Although TSMC has not yet released this earnings report, the market has already set very high expectations: institutions generally expect its 2026 revenue to maintain a growth rate of 20-25%, mainly driven by the continued ramp-up of 3nm/2nm and data center AI orders. While not as striking as the 30%+ growth seen in 2024–2025, maintaining such a pace after two years of significant growth is remarkable. Based on the current TAIEX price of around 1,700 and market expectations for 2026 EPS of approximately NT$75–80, the forward P/E ratio is roughly 22–24x. For a leading stock positioned at the very center of advanced AI nodes, this is not exactly a bargain, but it isn't expensive either. Many foreign brokerages have set 2026 price targets around NT$2,000, suggesting nearly 20% upside from current levels; even at NT$2,000, the P/E ratio would be between 25–27x, slightly higher than the historical mean but still far from a bubble.

Source: StockAnalysis

Whether the stock price can exceed NT$2,000 ultimately depends on the market's willingness to continue paying for this AI growth curve. Given current fundamentals and valuation levels, the room for TSMC to push toward NT$2,000 still exists, though the timing will need to be confirmed by subsequent performance and the realization of capital expenditures.

Recommended Articles