Tesla Just Delivered Very Bad News for Investors

Key Points

Tesla just reported its electric vehicle sales for the fourth quarter of 2025, and they capped off the sharpest annual decline in the company's history.

Tesla is losing market share to more affordable brands, like BYD, in important markets like Europe, and it won't be easy to recover.

Investors are paying a premium for Tesla stock based on its exciting product pipeline, but its sky-high valuation could open the door to steep losses this year.

- These 10 stocks could mint the next wave of millionaires ›

Tesla (NASDAQ: TSLA) stock is trading at a sky-high valuation, as investors place early bets on the future success of product platforms like the Cybercab autonomous robotaxi and the Optimus humanoid robot. These could eventually become the most valuable opportunities in the company's history, but there's a glaring issue in the here and now that investors shouldn't ignore.

Tesla is one of the world's largest manufacturers of electric vehicles (EVs), and this business still represents 75% of its total revenue. Unfortunately, sales plummeted by the largest amount in the company's history during 2025, as rising competition eroded its market share.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

The Cybercab and Optimus are still a few years away from mass commercialization, which means Tesla's financial results will face significant pressure in the short-term if its EV business continues to sputter. Here's why investors might want to avoid this stock for 2026.

Image source: Tesla.

The largest annual sales decline in company history

Tesla was the undisputed leader of the EV industry in 2023, delivering a record 1.79 million cars to customers worldwide for the year. But the competitive landscape shifted rapidly, and the company's EV deliveries sank by 1% in 2024, marking the first annual sales decline since the launch of its flagship Model S in 2011.

The situation worsened in 2025. Last week, Tesla revealed it delivered just 418,227 EVs in the fourth quarter (ended Dec. 31), falling short of Wall Street's consensus forecast of 422,850. It took Tesla's total deliveries to 1.63 million for the year, representing an 8.5% drop compared to 2024. It was the largest annual sales decline in the company's history.

Consumers in some of Tesla's biggest markets, like Europe and China, are choosing lower-cost options as cost-of-living pressures continue to bite. China-based BYD, for example, sells its entry-level Dolphin Surf EV for just $26,900 in Europe -- much cheaper than Tesla's Model 3, which starts at over $40,000 in most countries across the region. The inability to compete saw Tesla's market share shrink from 2.4% to 1.7% in Europe during 2025.

While Tesla's sales figures declined overall last year, BYD boasted a whopping 28% increase worldwide.

The Cybercab and Optimus are a while away

The income from Tesla's EV business fuels the development of its robotaxi and humanoid robot programs, so its current situation could have wide-reaching consequences for the company's future. According to recent guidance from Tesla CEO Elon Musk, the Cybercab won't enter mass production until the end of 2026, and Optimus is even further away from commercialization.

With that said, these products present Tesla with a massive financial opportunity. The Cybercab will run on the company's full self-driving (FSD) software, enabling it to autonomously haul passengers and make small commercial deliveries around the clock. This will create a new revenue stream, which Cathie Wood's Ark Investment Management predicts could be worth $756 billion per year from 2029.

But there is a caveat. Tesla's FSD software isn't approved for unsupervised use anywhere in the U.S. yet, and if this hurdle isn't cleared in the coming months, the Cybercab could be grounded before it even rolls off the production line.

Turning to Optimus, Musk believes humanoid robots will outnumber humans by 2040 because of their versatility. They can be tasked with mundane or even dangerous jobs in offices, factories, and households alike. Musk says Optimus could become Tesla's most successful product ever, with $10 trillion in potential revenue on the table over the long term.

The latest Optimus 3 robot is unlikely to enter mass production until the end of this year at the earliest, but Musk thinks it will scale to 1 million annual units very quickly.

Tesla's valuation opens the door to significant downside

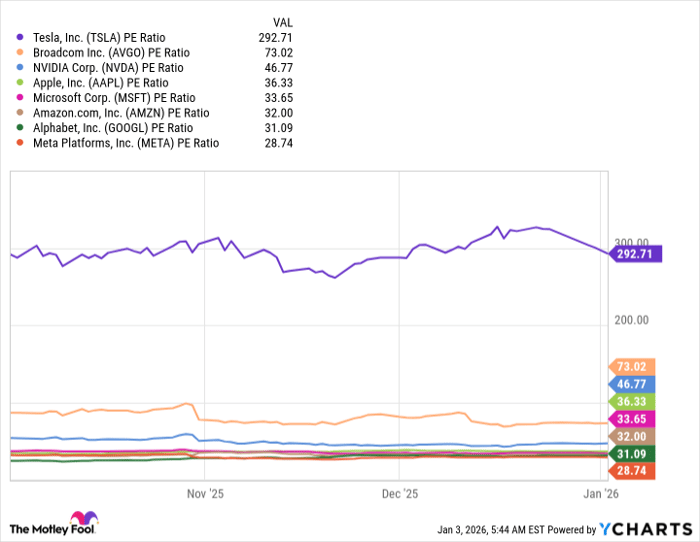

Tesla has generated earnings of $1.44 per share over the last four reported quarters (ended Sept. 30), placing its stock at a sky-high price-to-earnings (P/E) ratio of 292. When we compare Tesla to other tech powerhouses worth $1 trillion or more, its valuation is in a universe of its own. The P/E ratio of the next-most-expensive stock, Broadcom, is a whopping 75% lower:

TSLA PE Ratio data by YCharts. PE Ratio = price-to-earnings ratio.

Tesla is scheduled to report its fourth-quarter operating results on Jan. 28, and in light of the company's weak EV sales for the three-month period, its profits are likely to have suffered a sharp decline. That will probably drag down its trailing-12-month earnings per share, which will make its stock look even more expensive on a P/E basis.

The Cybercab and Optimus are still a long way away from generating meaningful revenue, so they won't be able to fill the void in Tesla's financial results from its declining EV sales. In my opinion, that creates a significant downside risk for Tesla stock this year.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $489,825!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $51,557!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $490,703!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

See the 3 stocks »

*Stock Advisor returns as of January 6, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends BYD Company and Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Recommended Articles