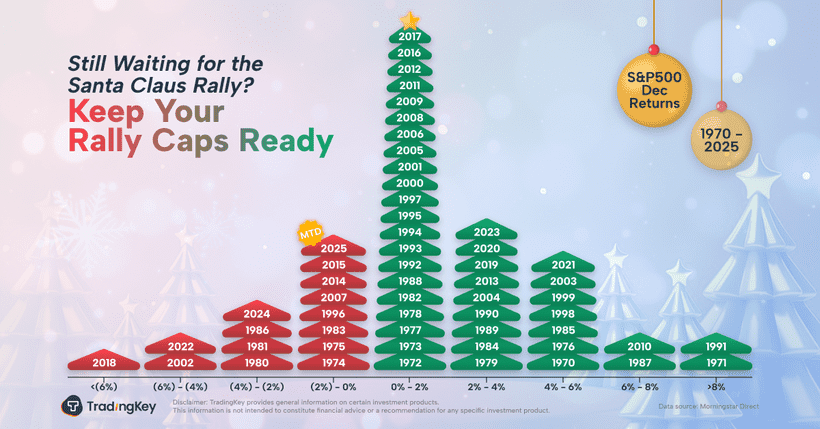

Soft CPI and Valuation Recovery May Set the Stage for a Santa Rally

TradingKey - Few market phrases are generating more attention this quarter than the so-called “Santa Claus Rally.” Defined as the final five trading days of the calendar year plus the first two sessions of the new year, it’s a seasonal stretch known for historically favorable equity returns.

And yet—more than halfway through December—the market remains nonlinear. Trend conviction is missing. Investors are split on whether a Santa rally will even show up this year.

But after yesterday’s cooler-than-expected CPI reading and a more clearly defined Fed policy path, the year-end setup may be shifting toward upside.

Macro Setup Now Supports a Seasonal Push

The Federal Reserve’s tone has turned broadly constructive.

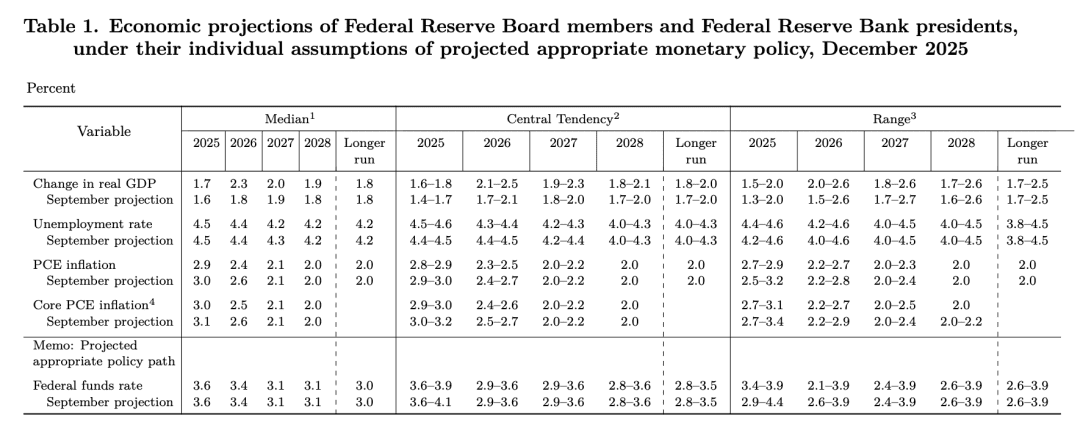

At the December FOMC, the Fed cut rates by 25bps—its third reduction this year and a cumulative 75bps of easing in 2025. The updated dot plot shows a 2026 median policy rate of 3.4%, and this time, official language emphasized the "magnitude and timing" of cuts ahead.

Markets remain divided about the pace—but not about the direction. There is growing consensus that a lower rate regime is now in play. That supports a risk-on backdrop for the final weeks of the year.

The Fed also revised down its inflation forecasts for 2026–2028 and upgraded GDP growth projections, signaling optimism on the macro outlook. While liquidity injections like $40B in short-term Treasury purchases per month aren’t a full-blown QE, they help stabilize curve structure and promote smoother risk dynamics.

In its latest statement, the Fed openly acknowledged a modest rise in unemployment—but still emphasized that “economic activity has been expanding at a moderate pace.” With lower rates, modest bond-buying, and a narrative of “soft landing with cooling inflation,” markets are reading the message clearly: a path toward supporting growth without re-inflating price pressure is underway.

On Thursday, core CPI came in at just 2.6% YoY—the slowest reading since early 2021 and well below consensus. While some quibbled over missing base comparisons in this release, the message was intact: disinflation is accelerating.

José Torres, senior economist at Interactive Brokers, noted: “Whether core inflation lands back in the 2% zone or stays stuck in 3% territory will be psychologically vital.” A return to the 2-handle would sharply boost risk appetite—and potentially open the door for a proper Santa Rally in U.S. equities.

Valuation Reset Already Underway

AI-related overvaluation remains a concern for some. But after several weeks of tactical de-risking, earnings resilience and reduced selloff pressure have helped tech stocks rebound meaningfully.

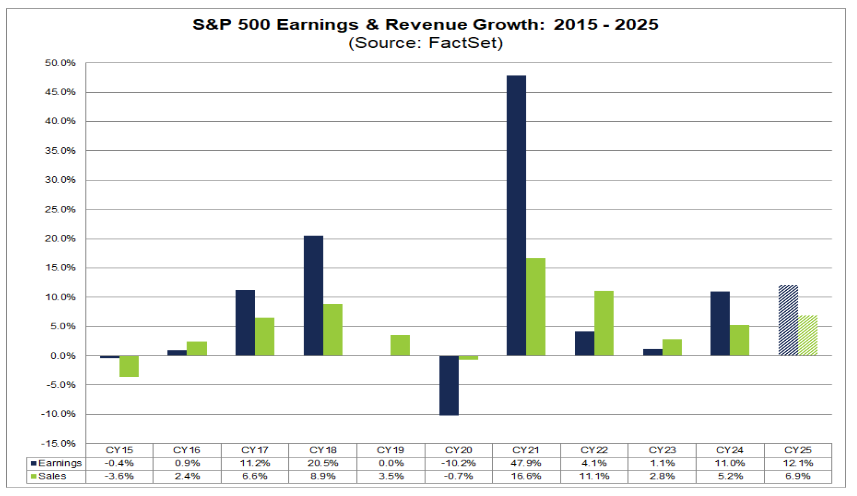

With Q3 earnings nearly complete, FactSet data shows that most S&P 500 firms have seen positive revisions. Consensus now calls for S&P earnings to grow by 12.1% in FY2025—marking a second consecutive year of double-digit profit increases.

Within that, analysts expect the “Magnificent Seven” to deliver 22% earnings growth in 2025. The rest of the index—493 other companies—is expected to grow a still-solid 9%.

Still, “sell the news” reactions remain common. Stocks that had rallied in advance of strong reports often fell sharply—even if fundamental beats occurred. The message: this market isn’t bearish on AI—it’s just correcting unrealistic valuations.

Much of the recent drawdown was a repricing mechanism, pushing stocks back into more reasonable bands.

AI remains the dominant investment theme—but leadership is rotating. Capital has moved beyond early-cycle names like NVIDIA and Google, and is now rotating through AI compute, storage, and application layers.

As near-term selling pressure fades, flows are beginning to turn. Hedge funds have been net buyers of U.S. equities for seven consecutive weeks, building fresh exposure to tech and high-beta sectors. With forced sellers gone, the rebound + recalibration trade has more room to play.

Meanwhile, the AI narrative is still expanding. OpenAI just released ChatGPT-5.2 to compete with Google’s Gemini 3. SpaceX’s plan to go public in 2026 at a $1.5T valuation has reignited the aerospace trade and spilled over into the AI-satellite crossover theme.

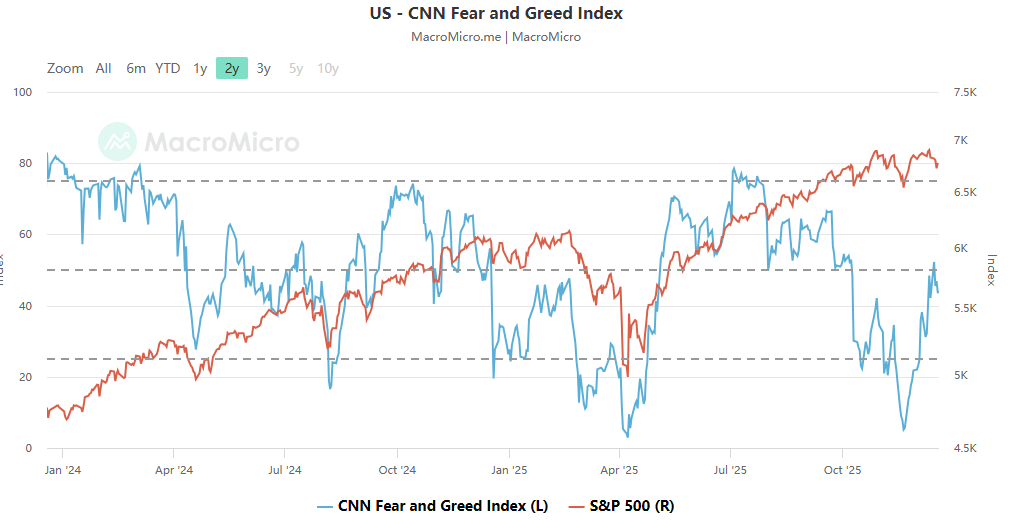

Investor anxiety—once defined by AI drawdowns and Fed uncertainty—is visibly retreating.

In early December, the Fear & Greed Index fell into the “fear zone” with a reading in the low 30s, driven by policy and earnings-related jitters. By mid-December, it had rebounded into the 47–51 range—near “neutral-to-greedy” territory.

That still doesn’t signal euphoria—but it confirms this: systemic panic may pass.

Friday’s Quad Witching May Add Noise

One near-term wrinkle: this Friday is the final quadruple witching event of the year.

With major derivatives expiring across options and futures, institutional books will have to rebalance, hedge, and roll forward. That often triggers sharp volatility spikes—unrelated to fundamentals—and can distort flows in the days around expiration.

This week’s quad witching arrives just ahead of the Santa Rally window, and may cloud sentiment briefly.

A Broader Look

In the short run, AI “bubble fears” mostly represent a valuation adjustment—not a breakdown in conviction.

Policy is easing. AI infrastructure spending continues to scale. And the investing imagination—through ventures like space-based computation—remains uncapped.

It’s not overreach; it’s recalibration.

The S&P 500 still has a path to test the 7,000 level into year-end if momentum holds and macro data cooperates.

And beyond that, year-end rallies tend to carry weight. Markets often use December’s tone to extrapolate into January positioning. Even if the S&P finishes strong, investors know the road ahead may be volatile. Tariffs remain a source of inflation pressure. Trump’s policy unpredictability adds noise. AI exuberance will ebb and flow. The broader message heading into 2026 may volatile upside.

Recommended Articles