Bubble Burst? MSTR: A Liquidity Crisis More Brutal Than Bitcoin’s Crash

Bitcoin Correction Amid Global Liquidity Ebbing

In December 2025, the crypto asset market underwent a heart-stopping stress test. After touching an all-time high of $126,000, Bitcoin sharply corrected, plunging to the $80,000 range. This represented a maximum draw-down of over 35%, marking the most severe deep cleansing of the current bull cycle.

The core catalyst was an unexpected tightening of global liquidity at the end of November. The U.S. government shutdown crisis led the Treasury General Account (TGA) to act as a giant sponge, absorbing trillions of dollars in bank reserves. This, coupled with an abrupt halt in stablecoin issuance, instantly dried up the market's once-ample funding. Simultaneously, soaring Japanese government bond yields triggered a wave of unwinding in the Yen carry trade, while tightened regulatory signals from China prompted the final tranche of panic selling by profit-takers. Beyond these macro factors, a deeper technical cause lay in the excessive long leverage that had reached a cyclical extreme, resulting in an extremely thin order book. This made the market susceptible to any minor disturbance, which was enough to trigger a chain reaction of waterfall liquidations, accelerating the price collapse.

MSTR: The Leveraged Amplifier in the Liquidity Crisis

As a stock highly correlated with Bitcoin, MSTR's share price mirrored Bitcoin’s trajectory but with significantly amplified losses. Besides the decline in the underlying asset (Bitcoin) price, MSTR was also hit by targeted institutional selling pressure. MSCI announced its plan to remove companies heavily invested in digital assets from its index system, an adjustment expected to lead to a passive fund outflow ranging from $2.8 billion to $11.6 billion. Furthermore, a potential year-end drop in its Nasdaq 100 ranking, combined with bearish reports from major Wall Street banks like JPMorgan, further fueled short-selling interest.

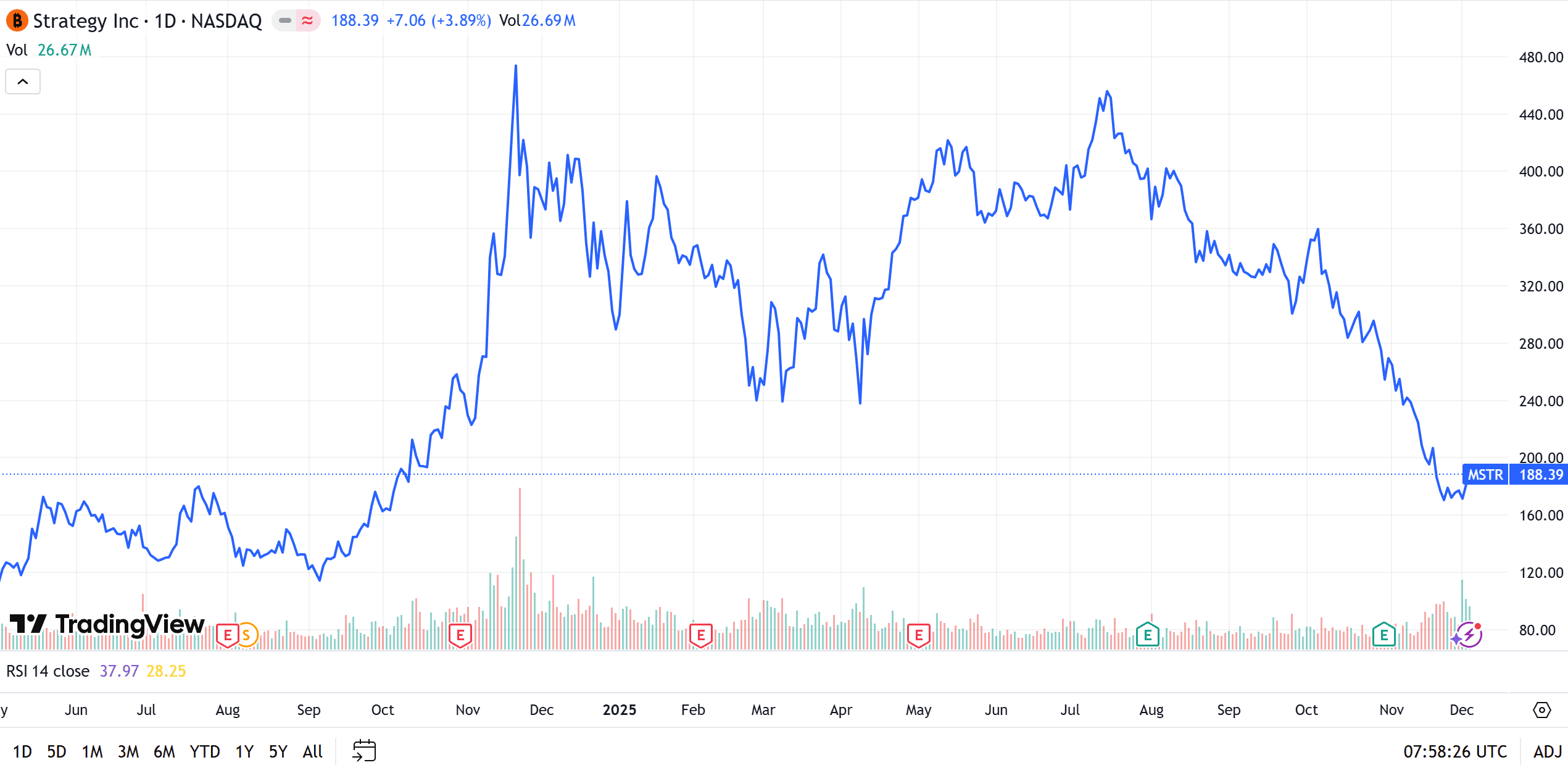

Under the perfect storm of multiple negative factors, MSTR's stock price experienced a drastic adjustment in early December, falling more than 60% from its July peak of $457. Its market capitalization evaporated by over 40% in November alone. On December 1st, the stock briefly hit a new annual low of $155.61, and its market cap shrunk from a peak of a hundred billion to approximately $52 billion, a collapse far more brutal than that of Bitcoin itself.

Decoding MSTR: From Software Company to Premium Machine

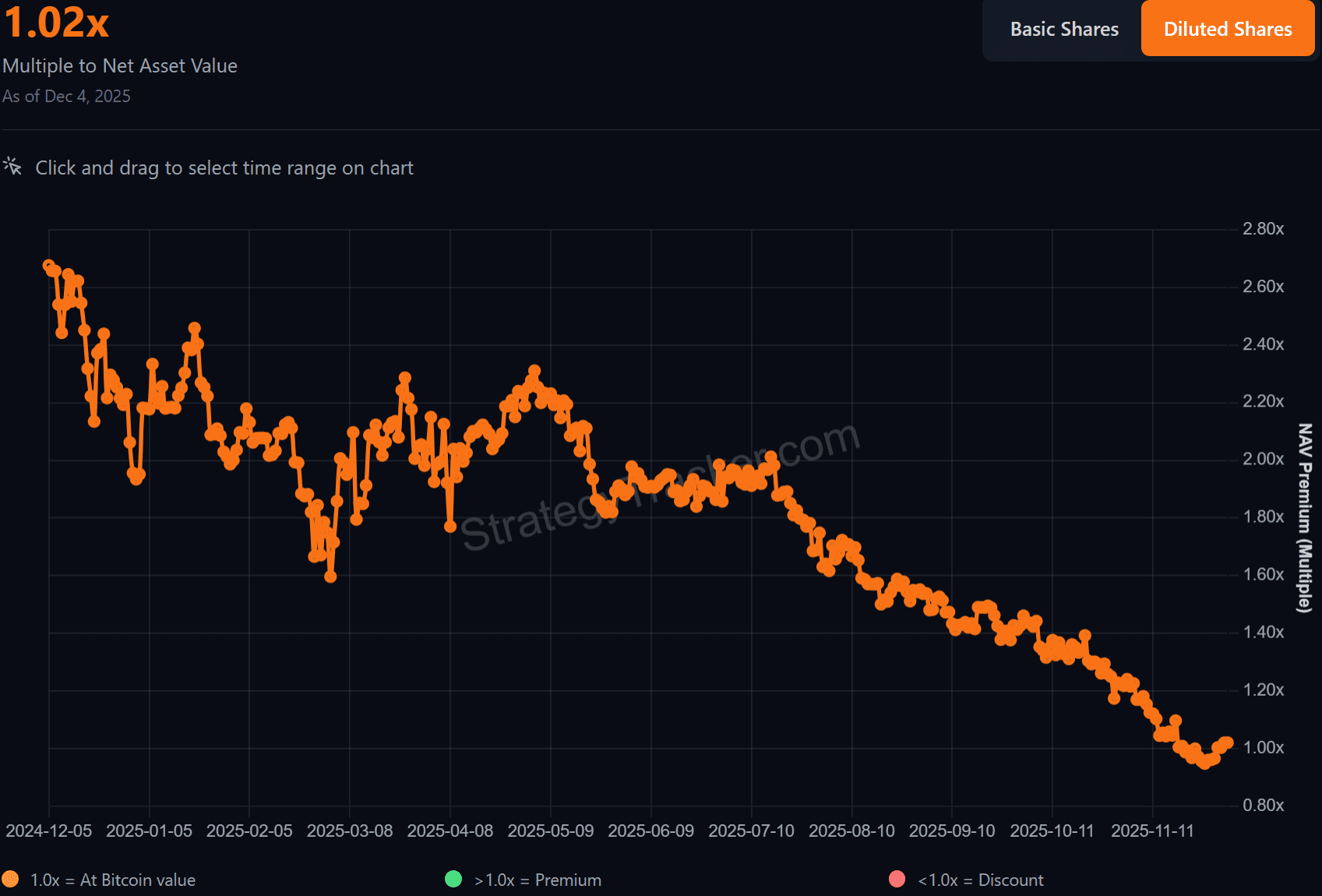

To understand the exaggerated volatility of MSTR, one must start with its unique operating mechanism: the mNAV (Market Value to Net Asset Value ratio). MSTR is no longer a traditional software company; it is a sophisticated machine that uses financial instruments to amplify Bitcoin's movements. Its core business logic revolves around the "Premium." Buying MSTR is essentially buying leveraged Bitcoin.

This underlying logic can be explained by the "Wine Cellar Theory": Suppose MSTR is a wine cellar, and Bitcoin is the Moutai stored inside. If the market price of Moutai is $100, and the transfer price of the cellar is also $100, the mNAV is 1. However, in a state of market frenzy, investors who cannot buy the wine directly due to regulatory restrictions, or who believe the cellar keeper (Saylor) can conjure up more wine in the future, are willing to pay $200 to acquire the cellar. At this point, the mNAV becomes 2; the extra factor of one represents the premium. The higher the mNAV, the crazier the emotional value the market assigns.

The Saylor Flywheel: A Premium-Driven Positive Feedback Loop

During the bull market cycle, Michael Saylor engineered a near-perfect "Flywheel Strategy." When the mNAV is high (i.e., the premium is substantial), the company aggressively issues new stock. Because the stock price is high, the company can raise significant cash with a minimal number of shares, and immediately use this cash to purchase Bitcoin. The magic is that despite the increase in share capital, the growth rate of the acquired Bitcoin, due to the high premium, far outpaces the rate of share dilution. This results in an increase in "Bitcoin per Share." This increase in per-share value further ignites market sentiment, driving up the mNAV premium and allowing the company to issue more shares at an even higher price. The higher the mNAV, the faster the flywheel spins, and the more Bitcoin is accumulated—a model that proved infallibly successful in an upward trend.

Flywheel Failure and the Davis Double Kill

However, the sole prerequisite for this flywheel to operate is the market's willingness to pay a premium; that is, mNAV must be significantly greater than 1. Once mNAV retreats to 1 or falls below it, the flywheel instantly fails, and investors face the brutal "Davis Double Kill." Taking the recent market as an example: when MSTR's stock price was $456, the mNAV was as high as 2, meaning half the share price was Bitcoin value, and the other half was pure emotional premium. When the Bitcoin price dropped from $120,000 to $92,000 (a 23% decline), market panic caused the premium to crash from 2x to 1.2x (a 40% premium decline). The combination of both led to MSTR's stock price being halved to approximately $181, a drop of up to 60%. This is the MSTR holder's nightmare: essentially, it was not the Bitcoin collapse that destroyed the stock price, but the bursting of the premium bubble that delivered the devastating blow.

Tail Risk: The Death Spiral Triggered by Convertible Arbitrage

More perilous than flywheel failure is the "Death Spiral" lurking in the capital structure, primarily stemming from MSTR’s heavy reliance on "Convertible Note" financing and the underlying hedge fund arbitrage mechanisms.

MSTR issues large amounts of convertible senior notes to purchase Bitcoin. The purchasers of these notes are often arbitrage institutions seeking risk-free returns. To hedge the equity risk embedded in the convertible notes, these institutions establish significant short positions in MSTR stock in the secondary market simultaneously with buying the bonds. This creates a dangerous negative feedback loop: when the stock price falls, institutions increase shorting pressure to maintain the hedge ratio or capitalize on profitable short trades. The deeper the stock price falls, the weaker MSTR's ability becomes to raise debt capital or buy more Bitcoin by issuing stock at a favorable price. If forced to issue shares at a low price, it would severely dilute existing shareholder equity, further driving down the stock price. This short-selling mechanism, intrinsic to the financing structure, forms a massive selling vortex during a down cycle, meaning the stock price could sink deeply even if the company does not sell any Bitcoin.

Macro Anchors: Bitcoin's Long-Term Narrative Unchanged

Despite the short-term heavy losses, Bitcoin's core logic as "digital gold" and a hedge against fiat currency devaluation remains intact. From a macro perspective, Bitcoin is at a critical juncture of "Massive Handover," where the primary buyer base has completely shifted from retail investors to traditional financial behemoths. The floodgates of U.S. wealth management channels are opening—this is the "Holy Grail" of crypto asset institutionalization. With Morgan Stanley, Citi, and Bank of America successively opening crypto asset allocation to their vast client base, and Vanguard allowing trading in crypto ETFs, trillions of dollars of long-term capital are entering the market. This capital has extremely high stickiness, fundamentally different from the "chase the pump, sell the dump" behavior of retail traders. Furthermore, with the Trump administration explicitly proposing to include Bitcoin in 401k plans, and the potential future entry of sovereign wealth funds, Bitcoin is completing its leap from an alternative asset to a core reserve asset. Once this process is complete, the current volatility may only be a minor blip on the long-term chart.

MSTR Balance Sheet Defense: A Survival Philosophy of Buying Time

The biggest misconception about MSTR is the crude application of the individual investor's "margin call/liquidation logic" to the corporate balance sheet. Investors worry that if the Bitcoin price drops below MSTR's cost basis (currently around $74,000), the company will face mandatory liquidation. However, MSTR is not using exchange-based contract leverage; the vast majority of its Bitcoin holdings are not pledged as collateral.

MSTR's primary form of liability is "unsecured convertible senior notes." This means that regardless of how sharply the Bitcoin price fluctuates, even theoretically falling to extremely low levels, as long as the company does not default on its debt, creditors have no right to demand mandatory takeover or liquidation of the company's Bitcoin assets. This debt feature dictates that MSTR faces "solvency risk" rather than "price fluctuation risk." Dropping below the cost basis only leads to unrealized losses on the accounting statement, and will not directly trigger a liquidity crisis.

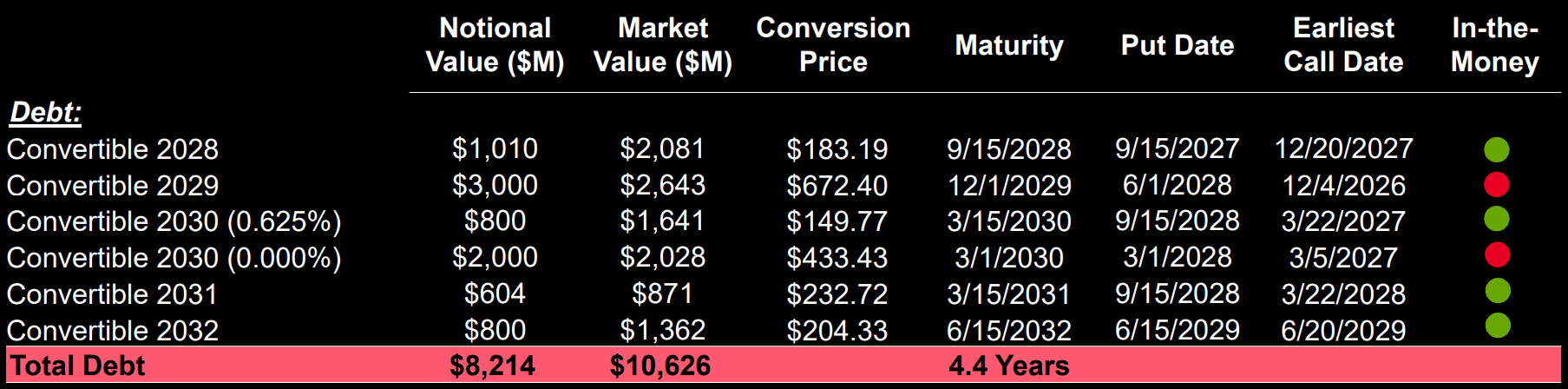

Building the Time Barrier: A Debt Ladder for Cycle Navigation

MSTR has constructed an extremely long safety window through sophisticated debt duration management—the core of its "buying time" strategy. Based on the latest debt structure analysis, the company has tiered the maturity dates of its debt. The first large-scale principal repayment is not due until September 2028, with subsequent debts extending to 2029, 2030, and even 2032. This means the company has completely shielded itself from principal repayment pressure for nearly three years. Even if Bitcoin enters a prolonged bear market or a period of sideways consolidation, MSTR is not forced to sell assets at a low price. This long-cycle debt arrangement grants the company immense strategic patience, allowing it to ignore short-to-medium-term book losses and calmly await the next Bitcoin halving cycle or a turn in macro liquidity. As long as time is on MSTR's side, short-term price volatility is merely noise.

Cash Flow Moat: Prepaid Interest and the ATM Mechanism

To ensure that it does not experience technical default during the long debt tenure, MSTR has established a dual insurance mechanism. The first is a bedrock of cash reserves. The company did not use every penny raised to buy Bitcoin, reserving approximately $1.44 billion in cash and cash equivalents. This fund is specifically allocated to cover debt interest and preferred stock dividends for approximately 21 months or more. This strategy is essentially a "prepayment" of future cash flow needs, completely cutting off the transmission chain where a drop in the coin price leads to the depletion of operating cash flow.

Secondly, MSTR possesses a powerful "ATM (At-The-Market)" equity financing capability. Even with a falling stock price, as long as a premium exists, the company can still raise fiat currency by issuing shares to the secondary market. This ability to convert highly valued equity into immediate cash flow allows MSTR to continuously replenish its interest reserves, secure creditor returns, and thereby prevent debt default.

Evolution of the Capital Structure: From Volatility Arbitrage to Fixed-Income Cornerstone

In the evolution of its defense system, MSTR is demonstrating an advanced form of mature capital operation. Early on, MSTR primarily relied on convertible notes, which were prone to attracting hedge fund short-selling arbitrage. Now, the company is strategically transitioning to a more stable capital structure. By introducing instruments like "Perpetual Preferred Stock" aimed at institutional investors, MSTR is reducing its reliance on a single financing channel. These new instruments have no definitive maturity date and only require fixed dividend payments. This not only opens up the massive pension and insurance fund markets but, more importantly, de-risks the repayment pressure from "principal repayment" down to "interest payment." A more robust capital structure allows the company to maintain access to financing channels even when the Bitcoin price is under pressure, and even use income generated from Bitcoin lending to further smooth financial stress, truly achieving a coexistence of high volatility on the asset side and ultra-stability on the liability side.

Conclusion

In summary, MSTR’s current crash is more of a valuation model premium reversion than an existential crisis. Its survival logic is not determined by the short-term fluctuations of Bitcoin but by its ability to sustain the growth of "Bitcoin per share content." By locking in long-dated debt until 2028, using reserves to lock in cash flow, and employing perpetual capital to secure financing channels, MSTR has constructed a high-resilience balance sheet structure. As long as Bitcoin does not go completely to zero, and as long as Saylor can use the time difference to weather the cycle, book losses are merely a number game. Of course, investors must still be wary of the liquidity shock from the MSCI index removal, key person risk, and extreme macroeconomic black swan events, but as for the business model itself, the machine continues to operate according to its established logic.

Recommended Articles