Can Anything Save Sweetgreen Stock Now?

Key Points

Sweetgreen's sales per locations have dropped, and automation hasn't delivered profits.

The company has a lot of cash to buy the necessary time to turn things around.

- 10 stocks we like better than Sweetgreen ›

Make no mistake about it: Salad restaurant chain Sweetgreen (NYSE: SG) is a business very much in need of saving.

Sweetgreen went public in 2021 with so much excitement -- shares soared 76% during its first of trading, closing in on a price per share of $50. But those early days would prove to be the peak. Sweetgreen stock has plunged more than 80% in 2025 and is now down 90% from its all-time high.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

Sweetgreen doesn't have a problem with selling food. The company has average unit volumes (AUV) of $2.8 million -- that's the sales revenue each location generates annually, on average. Clearly, there's plenty of consumer demand for salad.

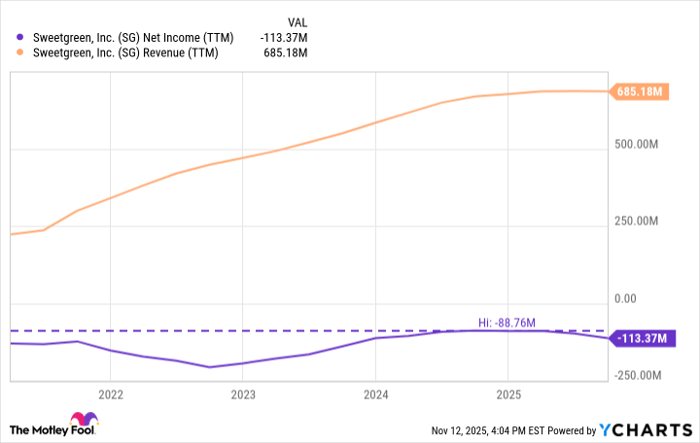

The company, however, does have a problem profiting. On a trailing-12-month basis, the best it's done as a publicly traded company is delivering a net loss of $89 million. In short, it hasn't even been close to turning the corner on the bottom line.

SG Net Income (TTM) data by YCharts

To finally become profitable, Sweetgreen has two options: grow sales or lower expenses. Higher sales volume can lead to operating leverage. But the company is starting to lose ground here. Management expects same-store sales to fall roughly 8% year over year here in 2025.

When it comes to lowering expenses, Sweetgreen expects automation to be the key. The company invested in robotics to make its food preparation more efficient and precise. It calls it its Infinite Kitchen vision. But after two years, it hasn't delivered meaningful profit improvements for the business as a whole. And in the third quarter of 2025, management announced that it was selling this part of the business, casting doubt on everything.

Needless to say, with sales slumping and profits lacking, Sweetgreen is a business that needs saving. But can anything save Sweetgreen now?

The Sweetgreen turnaround has one thing going for it

Sweetgreen has what might be the most important thing for a rescue operation to work: time.

Sweetgreen has time to turn things around because it has money. The business is still debt-free, and it had $130 million in cash at the end of Q3. Furthermore, it's selling its automation unit Spyce, giving it an equity position in the acquiring company Wonder as well as around $100 million in cash. This will bring its cash position up to over $200 million, providing significant runway.

In short, Sweetgreen's management has time to thoughtfully implement changes, and it has some resources to invest where it needs to.

Sweetgreen stock from here

The only thing that can truly save Sweetgreen stock is profitability. The stock has dropped to a cheap price-to-sales (P/S) valuation of less than 1. This bargain valuation is basically telling us that investors don't believe it will ever turn the corner.

If the business can eventually produce profits, investors will change their tune, and the stock will respond accordingly. But it may take time to get there.

Here's why: Sweetgreen's management said that two-thirds of its restaurants had operational issues last quarter. It's addressing problems and now only 40% have operational issues. But that's still a high percentage of underperforming restaurants. It would be a bad idea to rapidly scale while issues are ongoing.

A big part of the investment thesis for Sweetgreen has been its growth from opening new restaurants. But management is now slowing way down here while fixing operations. For perspective, it expects to only open up to 20 new locations in 2026, which would be a single-digit growth rate. This may be slower than what investors want, but it's probably the right move for Sweetgreen at this time.

Therefore, step one for saving Sweetgreen is improving operations at the majority of its restaurants. Once this is accomplished, management would return to scaling the business while lowering costs through automation -- it sold its kitchen automation business, but retains the rights to use the technology. Automation "remains central" to management's plan.

Sweetgreen can likely open new locations without many problems. Scaling at already open locations won't necessarily be easy, but it's also possible. But I think that investors should view automation with a dose of skepticism, because every expense for operating its restaurants have increased for Sweetgreen in 2025 in spite of automation.

Admittedly, not all locations have the Infinite Kitchen. But management says that restaurant profitability has only improved by about 800 basis points altogether at locations with its automation technology. Considering it has a negative 21% profit margin, that's still not enough to drive the profitability it needs once rolled out across the entire system.

Is there any hope?

In conclusion, Sweetgreen stock isn't without hope. But I think that investors need to realize that the company has a long uphill climb before it gets to where it needs to be. I would personally watch on the sidelines for meaningful progress before believing the turnaround story.

Should you invest $1,000 in Sweetgreen right now?

Before you buy stock in Sweetgreen, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sweetgreen wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $599,784!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,165,716!*

Now, it’s worth noting Stock Advisor’s total average return is 1,035% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of November 10, 2025

Jon Quast has no position in any of the stocks mentioned. The Motley Fool recommends Sweetgreen. The Motley Fool has a disclosure policy.

Recommended Articles