Disney’s Cash Cow Wakes Up: $10B Profit Crown, Streaming Turns the Corner, $7B Buyback Scoop!

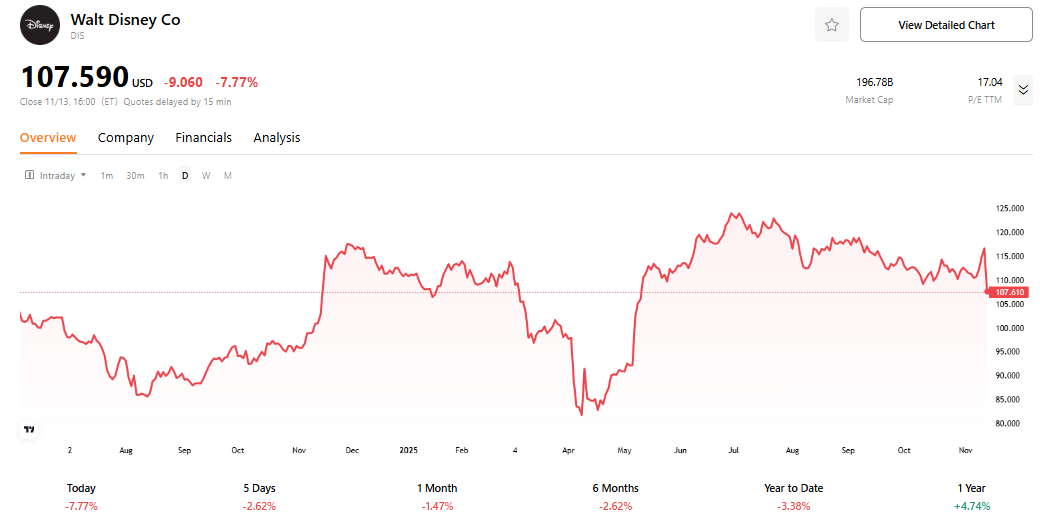

Disney’s stock has been stuck in a consolidating pattern for months, lagging the S&P 500 significantly year-to-date. Trading volume is steady and liquidity remains strong, yet the lack of forceful buying indicates that investors have not yet identified a fresh growth driver or are awaiting a decisive trigger.

2025 Fiscal Q4 Results Overview

The fourth-quarter results were mixed. Amid subdued market sentiment, the stock dropped nearly 10% intraday after the release and closed down almost 8%, erasing all gains since May 9.

- Revenue: Fourth-quarter revenue was essentially flat at $22.5 billion, weighed down by weakness in the Entertainment segment. Full-year revenue rose 3% to $94.4 billion, supported by streaming subscriber growth and the recovery in theme parks.

- EPS: Net income in the fourth quarter surged, aided by a low base in the prior year due to restructuring charges. Adjusted EPS fell 3%, pressured by a 35% decline in Entertainment operating income. For the full year, adjusted EPS increased 19%, reflecting broader profitability gains. The effective tax rate declined from 40.5% to 29.4%, contributing to the earnings improvement.

Segment Performance: Experiences Dominate, Entertainment Struggles, Sports Prepares for Growth

Disney reports across three segments: Entertainment (DTC, linear networks, content sales and licensing), Sports (primarily ESPN), and Experiences (theme parks, cruises, consumer products). Experiences stood out, generating more than half of total segment operating income, while Entertainment faced substantial challenges.

Entertainment Segment

Entertainment represents 45% of total revenue. Fourth-quarter revenue declined 6% and operating income fell 35%. Key components:

- Direct-to-Consumer (DTC: Disney+, Hulu, ESPN+):

DTC, frequently compared to Netflix and a critical component of Disney’s valuation premium, accounts for over 60% of the Entertainment segment. Revenue rose 8%—the only positive note—and operating income climbed from $253 million to $352 million, a 39% increase.

The quality of growth raises questions. Total subscribers reached 196 million, up 12.4 million quarter-over-quarter, but the bulk of the gain came from Hulu (+8.6 million) rather than the core Disney+ brand (+3.8 million). Average revenue per user rose overall, driven by Disney+, while Hulu’s ARPU declined. Much of the reported “strong growth” therefore stems from lower-margin bundled subscribers.

Nevertheless, full-year DTC profitability improved markedly—a landmark in the streaming strategy—thanks to price increases, bundling (Disney+ with Hulu), and content refinements (Marvel, Star Wars).

- Linear Networks:

Operating income dropped $107 million, largely due to the divestiture of Star India (which contributed $84 million in the prior year; $0 this quarter). Domestic advertising revenue weakened amid falling ratings and lower political ad spending, as cord-cutting continues to erode the business.

- Content Sales:

Revenue in this unit fell sharply by approximately $370 million this quarter, with operating income swinging from profit to loss. The decline stems primarily from the inability to replicate last year’s blockbusters such as Inside Out 2 and Deadpool & Wolverine, as the current slate of releases delivered lackluster performance.

Experiences Segment

Experiences reaffirmed its position as Disney’s financial cornerstone. Contributing nearly 40% of total revenue, the segment grew 6% year-over-year and posted a record $1.9 billion in operating profit—1.2 times the combined contribution from Entertainment and Sports. Full-year operating profit reached $10 billion, a new high, supplying reliable cash to support the company’s broader transformation.

- International parks led the way, with operating profit up 25% to $375 million, propelled by Paris Disneyland through higher attendance and per-capita spending.

- Domestic parks delivered a solid 9% increase to $920 million, driven mainly by the cruise business; domestic theme parks appear to be approaching a cyclical ceiling in pricing power and visitor growth.

Sports Segment

Sports is in the midst of heavy investment to shift toward a direct-to-consumer model. Fourth-quarter revenue edged up 2%, but operating profit slipped 2% to $911 million, as management deliberately traded near-term earnings for development of the ESPN DTC application.

The long-term plan is to reposition ESPN from a traditional cable channel into a comprehensive sports aggregation platform. Recent moves—acquiring NFL Network and partnering exclusively with DraftKings for sports betting—strengthen the content and monetization framework. Successful execution should enhance user engagement and open new revenue streams from subscriptions and advertising.

Outlook

Management expressed strong confidence for fiscal 2026, projecting double-digit EPS growth. The guidance rests on three pillars: (1) the full-year benefit of the completed $7.5 billion cost-reduction program; (2) high single-digit operating profit growth from Experiences; and (3) double-digit operating income growth in Entertainment, with DTC sustaining profitability and expanding margins.

Shareholder returns were sharply increased: the fiscal 2026 repurchase target was doubled to $7 billion from $3.5 billion in 2025, and the annual cash dividend was raised 50% to $1.50 per share. These steps underscore confidence in cash generation—operating cash flow rose 30% to $18.1 billion in fiscal 2025, and free cash flow increased 18% to $10.1 billion.

Disney remains in the challenging phase of its business transition. Near-term headwinds—structural decline in linear networks, uncertainty over DTC growth quality, and a carriage dispute with YouTube TV that could affect first-quarter 2026 revenue—will likely constrain the valuation. Over the medium to long term, however, the robust cash flow from Experiences provides a powerful buffer; DTC has passed the profitability inflection point and established a foundation for durable growth; and the aggressive increase in buybacks and dividends signals management’s firm belief in the company’s resilience and earnings potential. Trading at 17x PE—within the historical range—the stock suits patient, long-term investors.

Recommended Articles